Artificial intelligence is no longer a side tool in real estate. It is weaving itself directly into property searches, listing creation, marketing strategies, and even back-end MLS infrastructure. As the industry leans deeper into AI-powered systems, the central question becomes who is responsible for protecting the accuracy, safety and legal compliance of real estate data?

MLSs across the country are stepping into that role. After years of commission lawsuits and rising regulatory pressure, industry leaders are choosing a license-not-lawsuit model to protect consumers as AI becomes more powerful and more widely used.

The Push for Guardrails and Clear Disclosures

California is leading the charge with new disclosure rules for AI-adjusted listing photos. If an agent digitally edits landscaping, brightens interiors or removes unwanted objects, the state now expects side-by-side comparisons of the original and enhanced images.

Brokerages like eXp are revising internal policies to emphasize ethical enhancement rather than misleading presentation. AI has not created new risks… it has simply amplified old ones at incredible speed.

Quick Insight

MLSs have always banned edits that alter a material fact. AI did not change that rule… it just made violating it easier than ever. This is why formal, modernized guardrails matter.

AI Does Not Create Risk, It Scales It

MLS leaders cite simple examples. A gas meter digitally removed. A staircase reduced from four steps to three. These types of edits existed long before AI, but modern tools allow anyone to perform them instantly.

That speed is why MLSs like Doorify are updating their licensing agreements to reflect the modern real estate landscape. The goal is not to slow innovation but to define what is prohibited so safe, creative AI use can flourish.

Modernizing MLS Policies for an AI Era

Legacy frameworks like IDX and VOW were designed during the early days of internet real estate. They never anticipated brokerages feeding MLS data into AI engines, CRMs or automated analytics tools.

This raises the new and unavoidable question: What counts as authorized MLS data use in 2026?

MLSs are now rewriting agreements with clearer definitions and stronger privacy safeguards while still allowing brokers to innovate responsibly.

Who Should Control and Enforce AI Data Rules?

While national trade groups provide guidance, many MLS executives argue that state real estate commissions are best suited to oversee AI use. They already manage tens of thousands of licensees and enforce consumer protections.

Modern MLS platforms now resemble secure data networks rather than simple listing databases. With showing schedules, client data and financial details flowing through AI-enabled systems, regulation must evolve to match the stakes.

The Privacy Flashpoint Ahead

Consumer advocates warn of a major risk: agents and clients accidentally feeding sensitive documents into public AI platforms. Contracts, reports and financial materials were never meant to be handled without strict data controls.

And if AI mishandles or misinterprets that information, the liability becomes complex. Who is responsible for the mistake?

MLS leaders hope to address these issues proactively, avoiding another wave of litigation while still encouraging innovation.

Considering a Career in Real Estate?

Understanding AI rules and data compliance is now a core skill for modern real estate professionals. Cameron Academy trains future agents and brokers across all 50 states with licensing programs that prepare you for both technology and regulation.

If you are pursuing your Florida real estate license or expanding into mortgage, insurance, medical or finance licensing, Cameron Academy keeps you ahead of industry evolution.

Explore the Original Reporting

For deeper insights and the complete source article, visit Real Estate News:

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

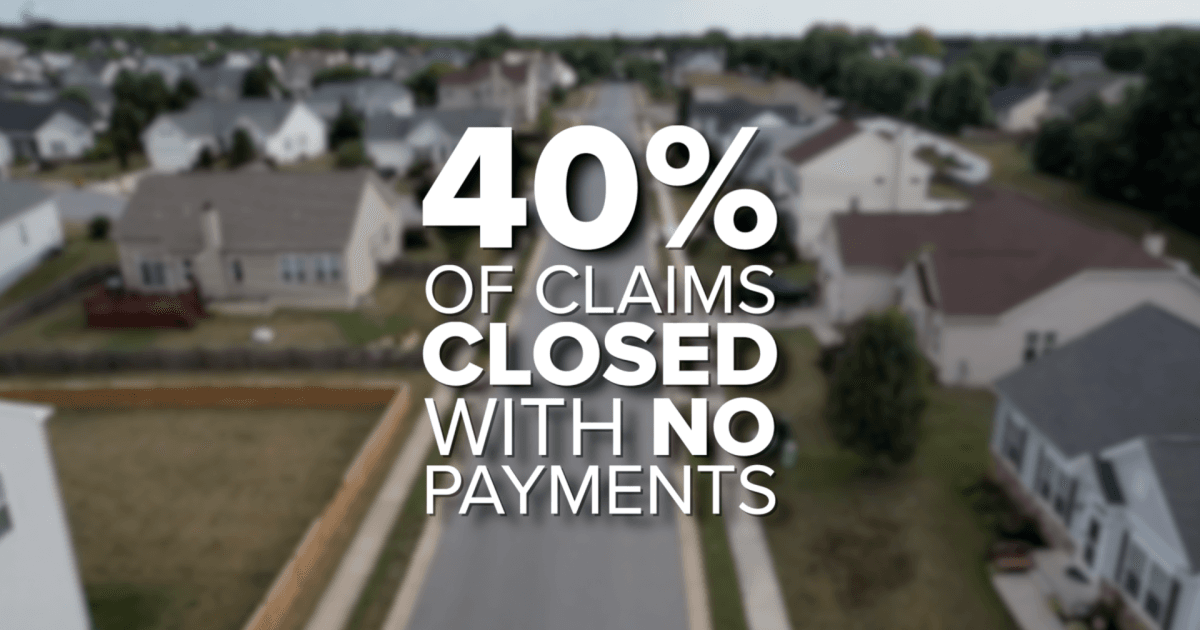

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}