AI Is Reshaping Mortgage Underwriting in 2026 — And Professionals Are Taking Notice

If you’ve been watching the mortgage industry evolve over the past few years, buckle up — 2026 is shaping up to be the year artificial intelligence finally steps into the underwriting spotlight. A new National Mortgage News survey reveals that 57% of mortgage professionals believe AI-powered underwriting will deliver the most transformative change across the industry this year.

And it’s not just hype. With breakthroughs in large language models and workflow automation, AI is now capable of tackling the “messy real world” of lending decisions — the odd file structures, inconsistent documentation, and human bottlenecks that have slowed innovation for decades.

Why Underwriting Is the Perfect AI Use Case

Theo Ellis, CEO of fintech platform Friday Harbor, highlights why underwriting is primed for transformation: it’s rule-heavy, data-packed, and historically vulnerable to bias. According to Ellis, the reason it has taken decades for AI to break through is simple — “the real world’s really messy.” But today’s AI systems finally process that complexity with consistency and speed.

Loan officers are already benefiting from early AI-powered file reading and workflow orchestration. John Brumund, senior vice president at Quontic Bank’s mortgage division, notes that loans passing through AI before reaching underwriting consistently produce more efficient outcomes.

The Ripple Effect: Credit, Verification, and Preapprovals

The survey shows widespread expectations for AI’s influence far beyond underwriting:

51% anticipate improved credit scoring and deeper analysis

49% expect real-time employment and income verification to accelerate significantly

Loan officers gain the power to build stronger, more accurate preapprovals earlier

This early clarity isn’t just good for borrowers — it’s a win for listing agents seeking reliable, confidence-boosting preapproval letters. As Ellis noted, “Underwriters can now focus on true risk management decisions,” thanks to AI offloading the administrative weight.

Policy Winds and Regulatory Influence

Policy direction is also fueling the rise of AI. With the second Trump administration signaling a looser federal mortgage regulatory environment, 41% of respondents expect overall policy softening. Another 37% say the current climate has encouraged increased AI use specifically in underwriting.

But states aren’t relaxing as quickly. Lenders remain cautious — data privacy and consumer protection still dominate conversations. Brumund emphasizes that mishandling data within AI systems is simply “not acceptable today.”

Resistance, Operational Overhaul, and the Path Forward

Despite momentum, large-scale adoption faces friction. Flyhomes CEO Tushar Garg cautions that redesigning underwriting processes carries real operational risk — and in the mortgage world, “things do not happen quickly or cleanly.”

Still, something powerful is happening: grassroots pressure from within the industry itself. Loan officers and processing teams are watching peers succeed and pushing leadership for the same AI tools. Faster cycle times, clearer paths to clear-to-close, and huge efficiency wins are too significant to ignore.

And when lenders see competitors scaling these benefits beyond small pilots, the rush toward AI becomes inevitable.

What This Means for Mortgage and Real Estate Professionals

For professionals in mortgage, real estate, and adjacent fields, AI’s rise in underwriting is more than a tech milestone — it’s a career-defining shift. Understanding how AI tools work, how they affect borrower experience, and how they influence regulatory expectations will be essential for the next generation of rising industry leaders.

That’s why institutions like Cameron Academy continue to develop forward-thinking education tailored to real estate, mortgage, insurance, finance, and other professional pathways. Staying ahead of AI-driven transformation is becoming a must-have advantage for long-term success.

To explore the original reporting and dive deeper, visit National Mortgage News at their full article here, written by Technology Reporter Spencer Lee.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

The title insurance industry is entering 2026 with a renewed focus on technology, operational efficiency, and stronger agent support after years of volatility. Leaders from major underwriters report rising transaction activity, improved affordability, and a surge in automation and fraud‑prevention tools—signs that smarter systems and better training will define the next wave of growth.

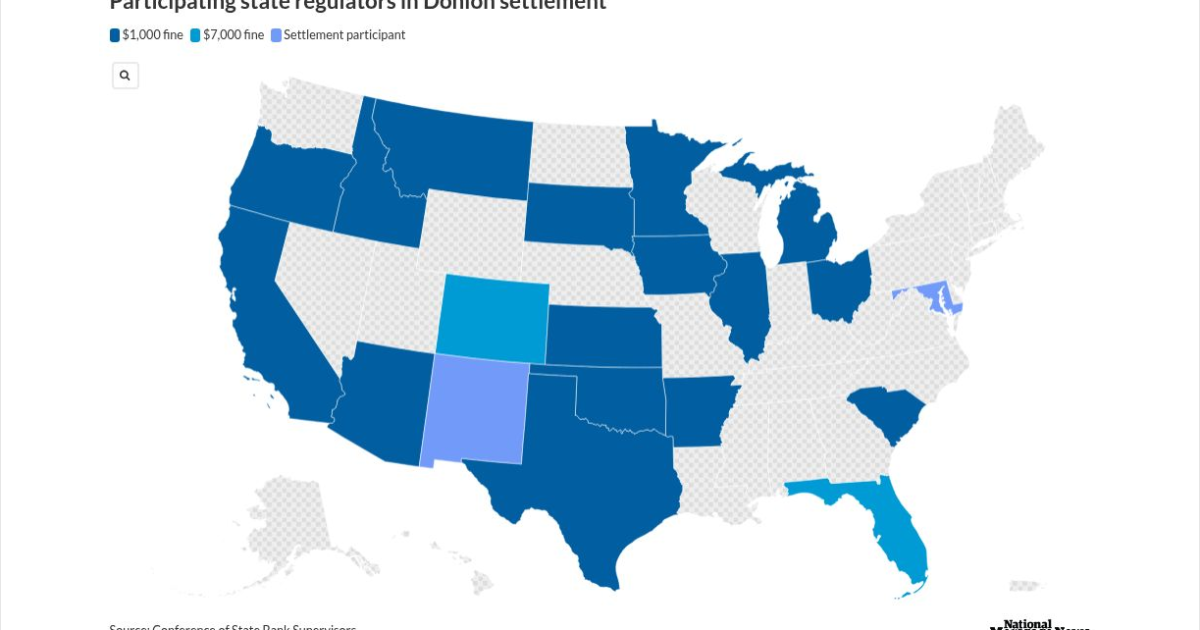

A multistate crackdown has sent shockwaves through the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, accepted a sweeping settlement that bans him from working as a mortgage loan originator in 21 states—19 of them permanently. Regulators say Donlon had another individual complete his mandatory licensing and continuing‑education courses, a violation that triggered a coordinated investigation and a $31,000 penalty. The case underscores regulators’ growing intolerance for education fraud and serves as a sharp reminder to industry professionals: cutting corners on licensing can end careers.

Florida’s once‑booming housing market is cooling fast as rising insurance premiums, increasing foreclosures, and expanding flood zones push buyers to back out of deals and force sellers to cut prices. With insurance now adding thousands to annual housing costs, professionals across real estate, mortgage, and insurance are navigating a dramatically shifting landscape that’s redefining affordability in the Sunshine State.

Florida begins 2026 with a wave of more than 250 new laws now in effect, impacting healthcare, insurance, real estate, and consumer protections statewide. From free breast cancer screenings for state employees to tighter pet insurance regulations, mandatory healthcare refund rules, enhanced animal‑cruelty penalties, and new condo‑management requirements, these updates carry major implications for professionals navigating Florida’s evolving regulatory landscape.

Florida’s barrier islands may offer postcard-perfect beaches and soaring real estate demand, but they’re also some of the most fragile and costly places to build in the United States. With 765,000 residents living on land that shifts, sinks, and takes the brunt of every major hurricane, the financial and insurance risks are accelerating fast. From billion‑dollar beach rebuilds to towers settling into the sand, today’s coastal development challenges are reshaping conversations around property values, disclosure, and long‑term resilience. For real estate professionals, understanding these risks isn’t just smart — it’s becoming essential.

A Cedar City development is turning heads with its fresh approach to affordability. The team behind Temple View Commons is delivering luxury‑inspired twin homes at prices below the local median by using a small, hands‑on staff and cutting traditional costs like realtor commissions. In a tight Utah housing market where inventory is scarce and prices remain high, their strategy offers a realistic path to homeownership without sacrificing high‑end finishes.

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}