AI Is Reshaping Mortgage Underwriting in 2026 — And Professionals Are Taking Notice

If you’ve been watching the mortgage industry evolve over the past few years, buckle up — 2026 is shaping up to be the year artificial intelligence finally steps into the underwriting spotlight. A new National Mortgage News survey reveals that 57% of mortgage professionals believe AI-powered underwriting will deliver the most transformative change across the industry this year.

And it’s not just hype. With breakthroughs in large language models and workflow automation, AI is now capable of tackling the “messy real world” of lending decisions — the odd file structures, inconsistent documentation, and human bottlenecks that have slowed innovation for decades.

Why Underwriting Is the Perfect AI Use Case

Theo Ellis, CEO of fintech platform Friday Harbor, highlights why underwriting is primed for transformation: it’s rule-heavy, data-packed, and historically vulnerable to bias. According to Ellis, the reason it has taken decades for AI to break through is simple — “the real world’s really messy.” But today’s AI systems finally process that complexity with consistency and speed.

Loan officers are already benefiting from early AI-powered file reading and workflow orchestration. John Brumund, senior vice president at Quontic Bank’s mortgage division, notes that loans passing through AI before reaching underwriting consistently produce more efficient outcomes.

The Ripple Effect: Credit, Verification, and Preapprovals

The survey shows widespread expectations for AI’s influence far beyond underwriting:

51% anticipate improved credit scoring and deeper analysis

49% expect real-time employment and income verification to accelerate significantly

Loan officers gain the power to build stronger, more accurate preapprovals earlier

This early clarity isn’t just good for borrowers — it’s a win for listing agents seeking reliable, confidence-boosting preapproval letters. As Ellis noted, “Underwriters can now focus on true risk management decisions,” thanks to AI offloading the administrative weight.

Policy Winds and Regulatory Influence

Policy direction is also fueling the rise of AI. With the second Trump administration signaling a looser federal mortgage regulatory environment, 41% of respondents expect overall policy softening. Another 37% say the current climate has encouraged increased AI use specifically in underwriting.

But states aren’t relaxing as quickly. Lenders remain cautious — data privacy and consumer protection still dominate conversations. Brumund emphasizes that mishandling data within AI systems is simply “not acceptable today.”

Resistance, Operational Overhaul, and the Path Forward

Despite momentum, large-scale adoption faces friction. Flyhomes CEO Tushar Garg cautions that redesigning underwriting processes carries real operational risk — and in the mortgage world, “things do not happen quickly or cleanly.”

Still, something powerful is happening: grassroots pressure from within the industry itself. Loan officers and processing teams are watching peers succeed and pushing leadership for the same AI tools. Faster cycle times, clearer paths to clear-to-close, and huge efficiency wins are too significant to ignore.

And when lenders see competitors scaling these benefits beyond small pilots, the rush toward AI becomes inevitable.

What This Means for Mortgage and Real Estate Professionals

For professionals in mortgage, real estate, and adjacent fields, AI’s rise in underwriting is more than a tech milestone — it’s a career-defining shift. Understanding how AI tools work, how they affect borrower experience, and how they influence regulatory expectations will be essential for the next generation of rising industry leaders.

That’s why institutions like Cameron Academy continue to develop forward-thinking education tailored to real estate, mortgage, insurance, finance, and other professional pathways. Staying ahead of AI-driven transformation is becoming a must-have advantage for long-term success.

To explore the original reporting and dive deeper, visit National Mortgage News at their full article here, written by Technology Reporter Spencer Lee.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

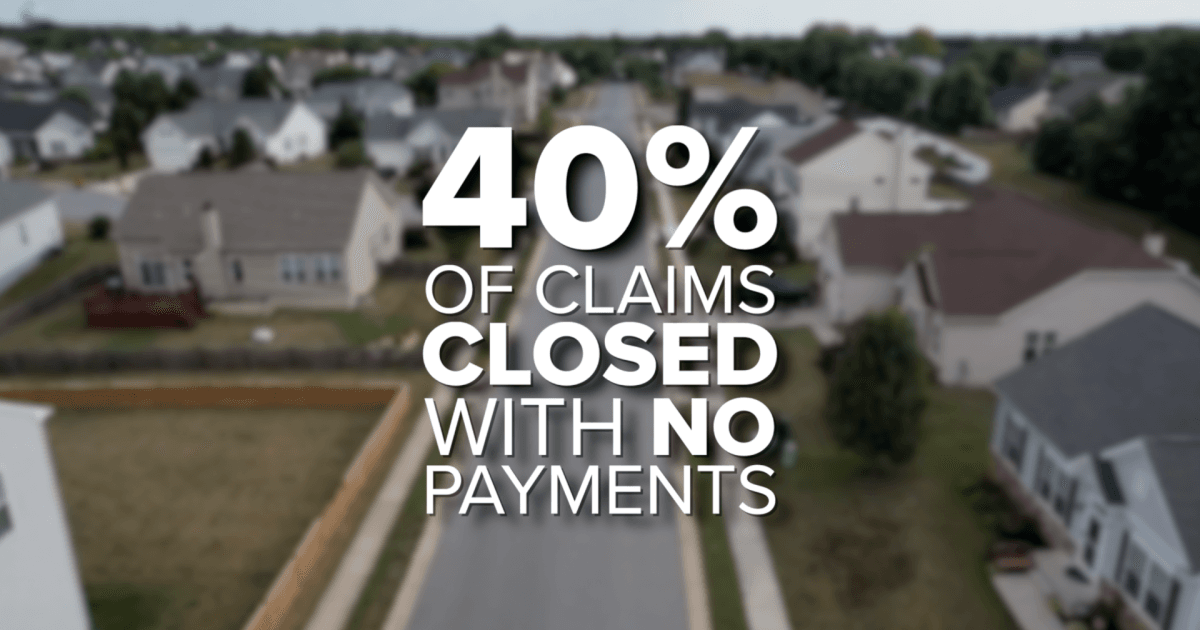

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}