In a bold move to address the pervasive student debt crisis, the Biden-Harris administration has rolled out a series of ambitious regulatory proposals. These initiatives, lauded by the Center for American Progress, are designed to rectify longstanding inequities within the student loan system and extend relief to borrowers most in need.

Following the Supreme Court’s June 2023 decision to overturn the initial student debt cancellation plan, President Joe Biden swiftly introduced a comprehensive “plan B.” This new approach seeks to establish clear guidelines on eligibility and debt cancellation limits, potentially impacting around 27.6 million borrowers. To date, the administration has delivered $168 billion in relief, with the new measures projected to cost an additional $147 billion over the next decade.

A central focus of the plan is to address inequitable interest accumulation. Proposed policies aim to benefit an estimated 23 million borrowers by capping interest growth. Furthermore, specific borrowers, particularly those who have been repaying loans for over two decades, may see their debts fully forgiven.

The relief will be automatic for eligible individuals, effectively bypassing the bureaucratic hurdles that previously impeded access. Importantly, these policies target those most burdened by student debts, including low-income groups, borrowers of color, and individuals who attended institutions now held accountable for failing to meet federal standards. The proposed regulations ensure that the benefits extend to these more vulnerable demographics, countering criticisms that the relief favors the affluent.

Moreover, the new initiatives aim to address systemic racial disparities in educational debt. Black borrowers, who typically incur higher debt levels and face longer repayment challenges than their white counterparts, stand to gain significantly from these proposals. Provisions such as the interest waiver are set to benefit a substantial portion of Black and Latino borrowers, with the intent to mitigate the racial wealth gap exacerbated by student loans.

These actions are part of the administration’s broader focus on accountability, underscoring the need for rigorous institutional oversight. The proposed regulations also include waivers for borrowers from unscrupulous or failed educational programs, aiming to protect future students from similar predicaments.

As deliberations continue, the Department of Education is fine-tuning these policies to ensure they align with broader financial equity objectives. While the current administration’s tenure may influence the timeline for enactment, future administrations have the potential to advance these reforms, fostering a more equitable and supportive educational financing system across the nation.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

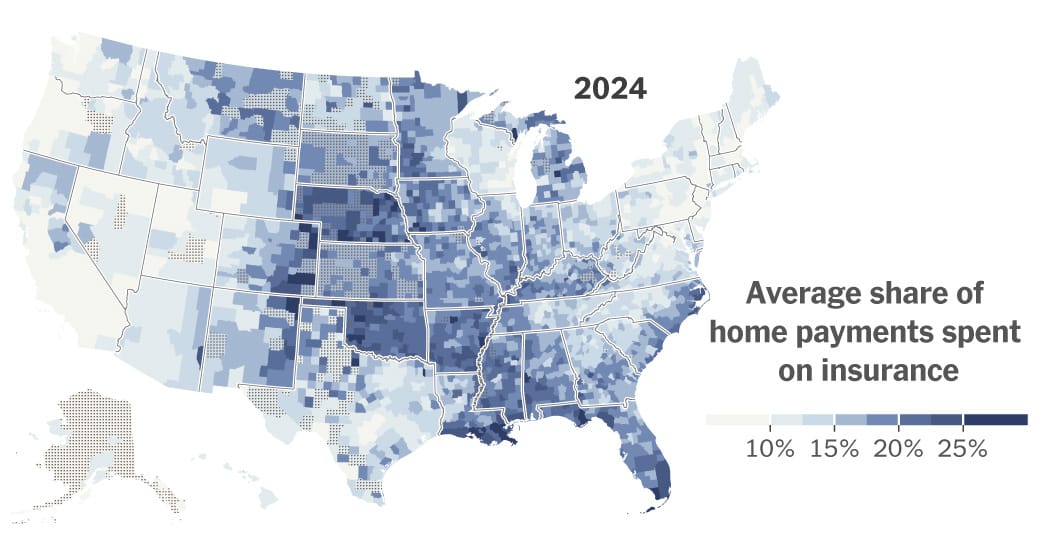

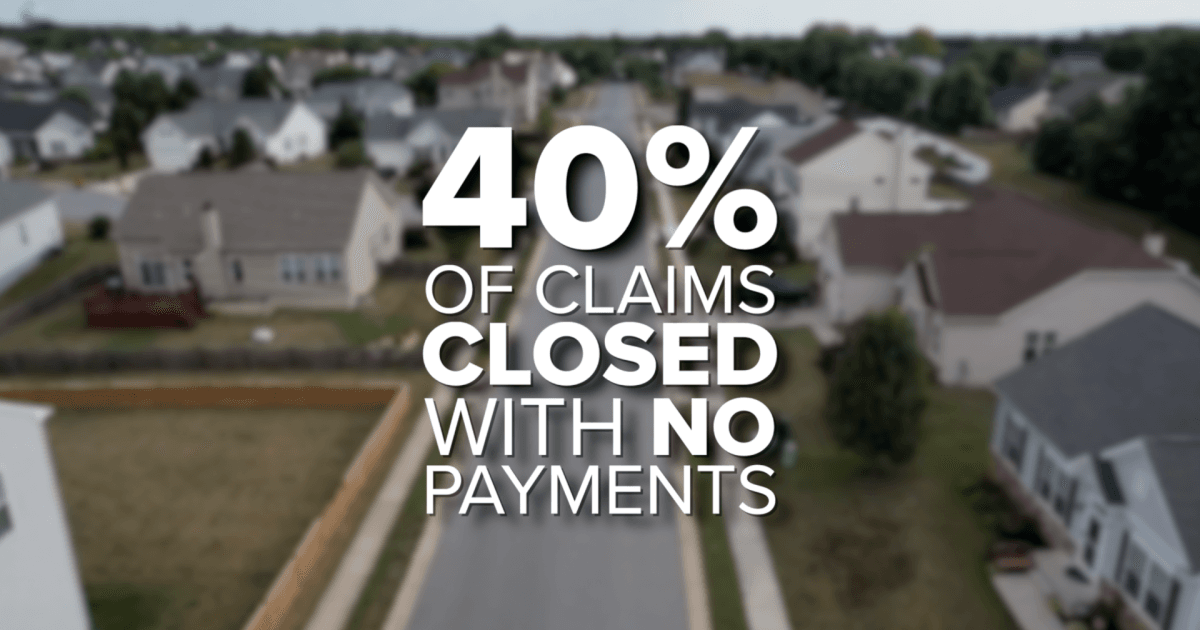

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}