In a bold move to address the pervasive student debt crisis, the Biden-Harris administration has rolled out a series of ambitious regulatory proposals. These initiatives, lauded by the Center for American Progress, are designed to rectify longstanding inequities within the student loan system and extend relief to borrowers most in need.

Following the Supreme Court’s June 2023 decision to overturn the initial student debt cancellation plan, President Joe Biden swiftly introduced a comprehensive “plan B.” This new approach seeks to establish clear guidelines on eligibility and debt cancellation limits, potentially impacting around 27.6 million borrowers. To date, the administration has delivered $168 billion in relief, with the new measures projected to cost an additional $147 billion over the next decade.

A central focus of the plan is to address inequitable interest accumulation. Proposed policies aim to benefit an estimated 23 million borrowers by capping interest growth. Furthermore, specific borrowers, particularly those who have been repaying loans for over two decades, may see their debts fully forgiven.

The relief will be automatic for eligible individuals, effectively bypassing the bureaucratic hurdles that previously impeded access. Importantly, these policies target those most burdened by student debts, including low-income groups, borrowers of color, and individuals who attended institutions now held accountable for failing to meet federal standards. The proposed regulations ensure that the benefits extend to these more vulnerable demographics, countering criticisms that the relief favors the affluent.

Moreover, the new initiatives aim to address systemic racial disparities in educational debt. Black borrowers, who typically incur higher debt levels and face longer repayment challenges than their white counterparts, stand to gain significantly from these proposals. Provisions such as the interest waiver are set to benefit a substantial portion of Black and Latino borrowers, with the intent to mitigate the racial wealth gap exacerbated by student loans.

These actions are part of the administration’s broader focus on accountability, underscoring the need for rigorous institutional oversight. The proposed regulations also include waivers for borrowers from unscrupulous or failed educational programs, aiming to protect future students from similar predicaments.

As deliberations continue, the Department of Education is fine-tuning these policies to ensure they align with broader financial equity objectives. While the current administration’s tenure may influence the timeline for enactment, future administrations have the potential to advance these reforms, fostering a more equitable and supportive educational financing system across the nation.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Skyrocketing insurance premiums and soaring rebuilding costs are transforming communities across Southwest Florida, especially in the wake of Hurricane Ian. As longtime residents struggle to keep up with rising financial pressure, wealthier newcomers and stricter building standards are reshaping the identity of places like Fort Myers Beach. With insurance rates now driving home sales, triggering potential foreclosures, and squeezing both owners and renters, Florida’s middle-class families face a growing question: can they afford to stay in the state they love?

Florida’s insurance industry is stabilizing fast, with nearly 1.6 million policies shifting from Citizens to private insurers and litigation dropping sharply. Regulators report stronger market confidence, decreasing premiums, and renewed competition—signaling one of the healthiest periods the state has seen in years.

A Leon County judge has ordered the restart of arbitration for Citizens Property Insurance claims, directly conflicting with a previous ruling that halted the process as potentially unconstitutional. With more than 400 cases now back in motion, real estate, insurance, and mortgage professionals can expect renewed activity in claim disputes and fresh uncertainty as Florida courts clash over the legality of Citizens’ arbitration system.

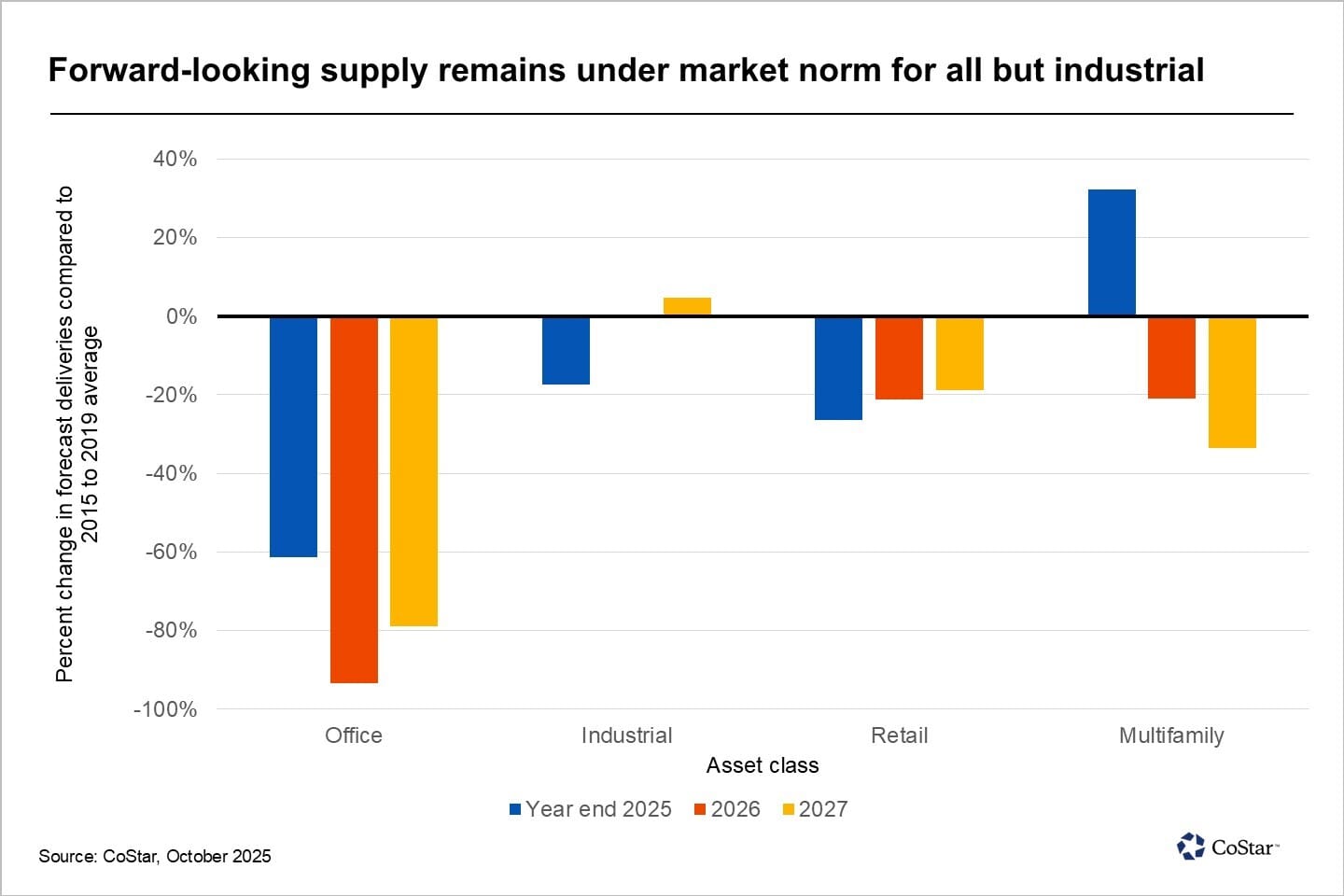

The DFW market is transitioning into a new construction phase marked by a slowdown in office development, a more selective approach to industrial projects, and an evolving housing landscape shaped by affordability and population growth. Developers are recalibrating their priorities, and for real estate professionals, understanding these shifts offers a critical edge in navigating—and capitalizing on—the next phase of the metroplex’s growth.

A new federal lawsuit claims Zillow pushed homebuyers toward Zillow Home Loans by rewarding affiliated agents with valuable leads — all without proper disclosure. The suit alleges undisclosed incentives, referral quotas, and potential RESPA violations, raising major concerns about steering, fiduciary duties, and Zillow’s expanding mortgage ambitions.

The mortgage industry is evolving fast, and the lenders who come out on top will be those who innovate without uprooting what already works. By building on strong technology foundations, streamlining workflows and adopting smart automation, lenders can reduce costs, improve customer experience and stay resilient in any market cycle. This article breaks down why innovation matters now, how a stable tech ecosystem protects lenders in volatile conditions and why small, strategic steps can drive long-term transformation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}