Brookline’s Hidden Flood Risks: What New Maps Reveal and What They Miss

Brookline’s flood risk has long been a topic of curiosity for homeowners, investors, and local professionals. But this year, the release of FEMA’s updated flood maps sparked an important conversation: Is Brookline’s flood risk far higher than what the new maps show?

In June, FEMA introduced updated maps for Norfolk County. Brookline’s new map identifies 97 high‑risk parcels—properties with a 1% or greater annual flood chance requiring flood insurance. These parcels sit mostly around Leverett Pond and the Muddy River. Helpful as these tools are, local experts say they don’t tell the whole story.

Source: Brookline News — “Brookline’s flood risk may be higher than FEMA’s new map shows”

Read the original report

“There is a false sense of safety that many people assume if their property is not officially designated in a FEMA floodplain,” said Maria Rose, Brookline’s environmental engineer and floodplain administrator. “Flooding can happen anywhere.”

The Muddy River: Designed for Protection, Tested by Nature

Much of Brookline’s flood resilience traces back to Frederick Law Olmsted’s Emerald Necklace design—parklands surrounding waterways to buffer homes from flooding. Landscape historian Arleyn Levee emphasized that these green spaces weren’t just aesthetic; they were strategic environmental mitigation.

The town saw this system tested in the 1990s. In the floods of October 1996, more than 12 inches of rainfall overwhelmed the Muddy River system. Sediment, neglect, and obstructed waterways worsened the problem. Roads, stations, and buildings experienced significant damage.

In response, the Muddy River Restoration Project began—ultimately becoming a $92 million, decades-long effort completed largely by 2023. The improvements included dredging, invasive species removal, and daylighting buried river segments—restoring both ecological function and flood capacity.

Flooding Beyond the Riverbanks

While riverine flooding is the basis for FEMA’s models, it’s only part of the problem. Brookline experiences frequent pluvial flooding—flooding caused when stormwater overwhelms soil absorption and drainage systems.

Transportation corridors, MBTA stations, and roads bordering floodplains are vulnerable during significant rain events. Residents voiced major concerns about access, travel disruption, and emergency response times during Brookline’s Climate Action and Resiliency Plan (CARP) development.

Beacon Street: The Flooding That FEMA Doesn’t Capture

Beacon Street is one of Brookline’s most flood‑prone corridors, yet FEMA’s map labels the area low‑risk. Another model reveals a different truth.

Explore the Interactive Map: First Street Flood Factor offers a richer look at flood risks, including rainfall, tides, surges, and climate‑driven changes.

When First Street’s factors are considered, the number of Brookline properties at risk over the next 30 years jumps to over 1,300—nearly a quarter of the town.

Flood modeler Daniel Rees notes that flood maps are only “one view” of a broad, uncertain future. Being “just inside” or “just outside” a FEMA zone can mean drastically different risk levels.

Other tools, such as the USGS Coastal Change Hazards Portal, Massachusetts CZM Hurricane Surge map, and NOAA’s Sea Level Rise Viewer, provide additional lenses for evaluating risk.

Climate Change and Urbanization: A Growing Threat

Brookline officials warn that changing climate patterns are intensifying storms and reshaping flood risk. More frequent downpours combined with hard urban surfaces reduce natural water absorption, amplifying flooding potential.

“The amount of water that is now coming down in a storm is unbelievable,” Levee said, expressing doubt about whether traditional flood control designs can handle modern extremes.

Rees raised concerns familiar to many real estate and insurance professionals: Could areas like Brookline see future impacts on property values—or even insurability?

How Soon Until Brookline’s Next Big Flood?

While storms causing nuisance flooding are expected, flash floods—like those in 1996—pose serious risk even in places labeled “low‑risk.” Nationwide, over 40% of flood insurance claims come from properties outside FEMA high‑risk zones.

This reality puts communities like Brookline on alert. Climate‑fueled storms have caused catastrophic flooding in cities across the U.S. in recent years. Local officials worry that a similarly intense event could overwhelm culverts, road systems, and restored waterways.

For now, flood control measures stand ready—but their true test may be closer than residents expect.

Professionals Take Note:

Flood literacy is becoming essential for real estate agents, adjusters, insurers, and urban planners. At Cameron Academy, we train professionals nationwide to recognize environmental factors that influence property value, insurance needs, and long‑term risk.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A growing share of American homeowners now carry mortgage rates above 5%—a dramatic shift that’s reshaping refinancing, inventory, and buyer behavior nationwide. With more than 30% of borrowers locked into rates over 5% and 20% above 6%, the market is split between owners holding on to low pandemic‑era loans and new buyers taking on higher‑rate mortgages. Federal efforts to push rates down could unlock millions of refinancing opportunities, while buyers see only modest monthly savings. For real estate professionals, understanding these rate dynamics is crucial as they increasingly drive inventory levels, affordability, and market activity.

New Moody’s data shows commercial real estate deal volume slipped 20% in December, marking a second monthly decline. Yet the full year tells a different story: 2025 ended with a 17% gain, signaling a quiet but resilient recovery. The biggest surprise came from the office sector, which posted a 21% jump in activity as return‑to‑office trends and AI‑driven job growth boosted demand. Multifamily, retail, and alternative assets like data centers also saw strong momentum, giving real estate professionals a market full of fresh opportunities heading into 2026.

Florida drivers and industry professionals are heading into 2026 with good news: auto insurance rates are dropping across the state as the market shows strong signs of stabilization. USAA leads the latest wave with a 7% average rate decrease expected in May 2026, saving members more than $125 million annually. They join several major insurers — including State Farm, Progressive, AAA, Allstate, and Florida Farm Bureau — all approving significant reductions. Officials credit recent legislative reforms, especially tort reform, for the improved loss ratios and renewed insurer confidence. With both auto and home insurance markets strengthening, Florida’s real estate, mortgage, and insurance professionals can expect more consumer confidence, smoother transactions, and expanding career opportunities.

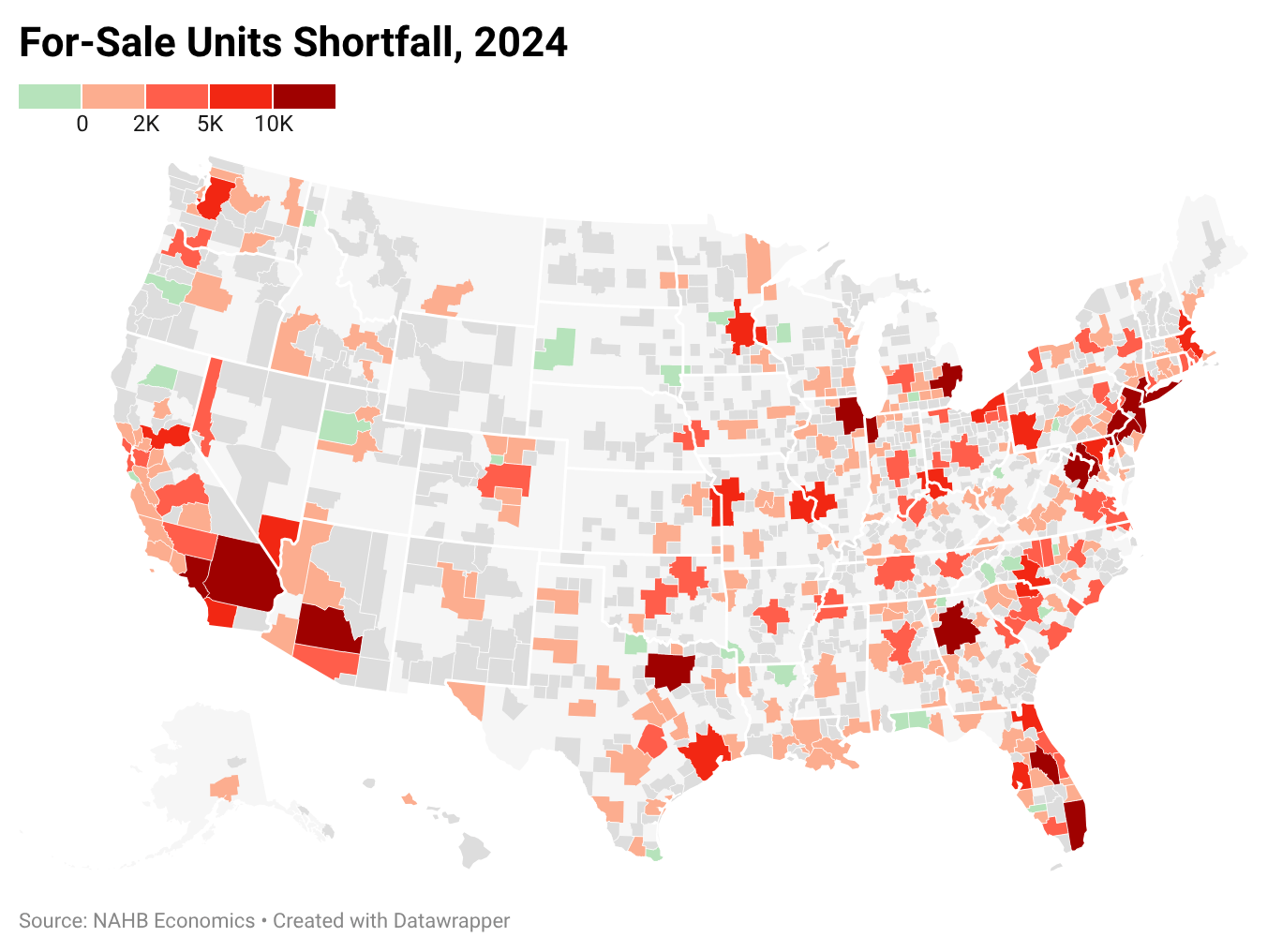

New data from Eye On Housing and the NAHB shows the U.S. remains short more than 1.2 million housing units, keeping pressure on both rents and home prices. Record‑low vacancy rates, slow single‑family construction, and restrictive zoning continue to fuel intense competition in 2024. Major metros like Chicago, New York, and Atlanta face some of the deepest deficits, and the true nationwide shortfall may be even higher when accounting for overcrowding and aging homes. For real estate professionals, the ongoing shortage means sustained demand, tighter inventory, and major opportunities for those who understand the evolving market.

Top real estate coach Jason Pantana says the divide between agents today isn’t about who has “tried” AI — it’s about who is immersed in it. In a new HousingWire interview, he explains why AI isn’t a gimmick but a full business system that amplifies output, improves authenticity, and reshapes how clients search for agents. From prompt mastery to AI‑driven visibility on Google, Pantana reveals how agents who commit even 15 minutes a day to learning AI are already outperforming those who hesitate.

Dallas–Fort Worth’s commercial real estate market closed 2025 with a split personality. Industrial dominated with massive new deliveries and soaring leasing demand, retail held steady with some of the market’s strongest fundamentals in years, and office continued to falter under remote‑work pressures. High vacancies, weak absorption, and rising demand for top‑tier space show the sector’s ongoing reset. Meanwhile, industrial and retail strength position the Metroplex for another powerhouse year heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}