Central Bank Digital Currencies: Bridging Innovation and Stability

In a world increasingly dominated by digital innovation, the emergence of central bank digital currencies (CBDCs) marks a pivotal evolution in the financial sector. Unlike traditional money, CBDCs offer a digital alternative that is both backed and issued by national central banks, combining the benefits of digital transactions with the stability of government-backed currency. Understanding the depth and breadth of CBDCs is crucial for financial experts navigating the future of finance.

The Evolution of Money and Introduction of CBDCs

Money has seen significant transformations over the centuries, evolving from barter systems to banknotes and now to digital banking. CBDCs represent the next step, aiming to modernize financial services to be more resilient and inclusive. Central banks like the European Central Bank and the Federal Reserve are exploring CBDCs to stay at the forefront of technological innovation while safeguarding monetary sovereignty.

Technological Underpinnings

CBDCs are digital currencies issued by central banks that hold legal tender status, bridging the gap between digital and physical economies. While some countries opt for blockchain technology to leverage decentralization, transparency, and security, others prefer a centralized approach to maintain tighter control. Key technological considerations for CBDCs include:

Scalability: Ensuring the system can handle large volumes of transactions.

Security: Implementing robust defenses against cyber threats and fraud.

Interoperability: Facilitating seamless integration with existing financial technologies.

Privacy: Balancing transparency with individual rights to privacy.

Worldwide Implementation Efforts

Different nations have taken unique approaches to deploying CBDCs, reflecting their diverse economic contexts and objectives:

Sweden’s E-krona: Developed in response to dwindling cash usage, aiming to secure public access to trusted money in a digital format.

China’s Digital Yuan: Part of a broader initiative to increase China’s influence in the global financial system.

Eastern Caribbean’s DCash: Implemented to improve financial accessibility and resilience in a region prone to natural disasters.

Advantages of CBDCs

CBDCs offer numerous advantages, including:

Efficiency: Streamlining payments and settlements, enhancing economic activity and reducing transaction costs.

Financial Inclusion: Providing a gateway for financial services to populations typically outside the banking system.

Reduced Operational Costs: Digital formats decrease costs related to printing, distributing, and securing physical currency.

Monetary Sovereignty: Helping countries assert control over their monetary systems.

Stability: Offering a secure alternative to private digital currencies and volatile cryptocurrencies.

Economic and Market Implications

The implementation of CBDCs could significantly impact monetary policy and financial stability. By providing central banks with a new tool for conducting monetary policy, CBDCs could enhance control over the money supply and interest rates. They may also influence the banking system by providing individuals with direct access to the central bank’s resources, potentially reducing transaction costs and increasing speed.

CBDCs carry significant implications for the global financial marketplace, including:

Banking Sector Dynamics: With the potential to hold funds directly with the central bank, consumers might choose CBDCs over traditional bank deposits.

International Trade: Facilitating easier and cheaper cross-border transactions, potentially reshaping economic engagement.

Innovation and Competition: Spurring innovation within the private sector, pushing financial institutions to enhance their service offerings.

Despite the potential benefits, CBDCs raise significant issues, particularly regarding privacy and data security. Ensuring a CBDC system is secure against cyberattacks while maintaining user privacy is a complex challenge.

Regulatory and Policy Frameworks

The successful rollout of CBDCs will require comprehensive regulatory frameworks to address potential risks and ensure smooth operation. These frameworks need to tackle issues related to cybersecurity, privacy, legal tender status, and international cooperation.

As digital currencies become more integrated into the global financial system, they may offer a more inclusive and efficient financial framework but will require careful implementation to balance innovation with stability. CBDCs present a profound opportunity to enhance financial transactions, promoting greater efficiency, inclusivity, and stability. However, their successful integration demands careful consideration of technological choices, impact assessments on existing financial structures, and robust regulatory measures.

The information provided here is not investment, tax, or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida’s property insurance system is once again spiraling as new “market-friendly” reforms fail to stabilize rising premiums, insurer failures, and mounting homeowner frustration. Despite aggressive efforts to shift policyholders from Citizens to private carriers, many of the new insurers stepping in are tied to past insolvencies, questionable ratings, and political influence. For real estate, mortgage, and insurance professionals, these systemic cracks are reshaping closings, valuations, and risk across the state—making it essential to stay ahead of ongoing regulatory and market shifts.

Commercial real estate is heading into a turning‑point year in 2026, driven by economic uncertainty, AI‑powered transformation, shifting demographics and rising portfolio risk. Insights from The Counselors of Real Estate highlight the top issues shaping the year ahead—from fiscal pressures and capital constraints to housing shortages, global volatility and the future of data‑driven decision‑making. For real estate, mortgage, insurance and finance professionals, these trends offer a clear roadmap for staying competitive and preparing for the next wave of industry change.

AI-powered tools, fraud protection systems, and smarter MLS integrations are sweeping through the real estate industry as major organizations adopt new technologies. From RealReports hitting its 50th partnership to BeachesMLS unveiling instant AI home visualizations and Doorify boosting security, professionals are seeing rapid advancements that promise sharper insights, safer transactions, and more efficient rental workflows. This evolving tech landscape underscores the importance of staying educated and adaptable — especially for agents preparing for a competitive, AI-enhanced 2025 market.

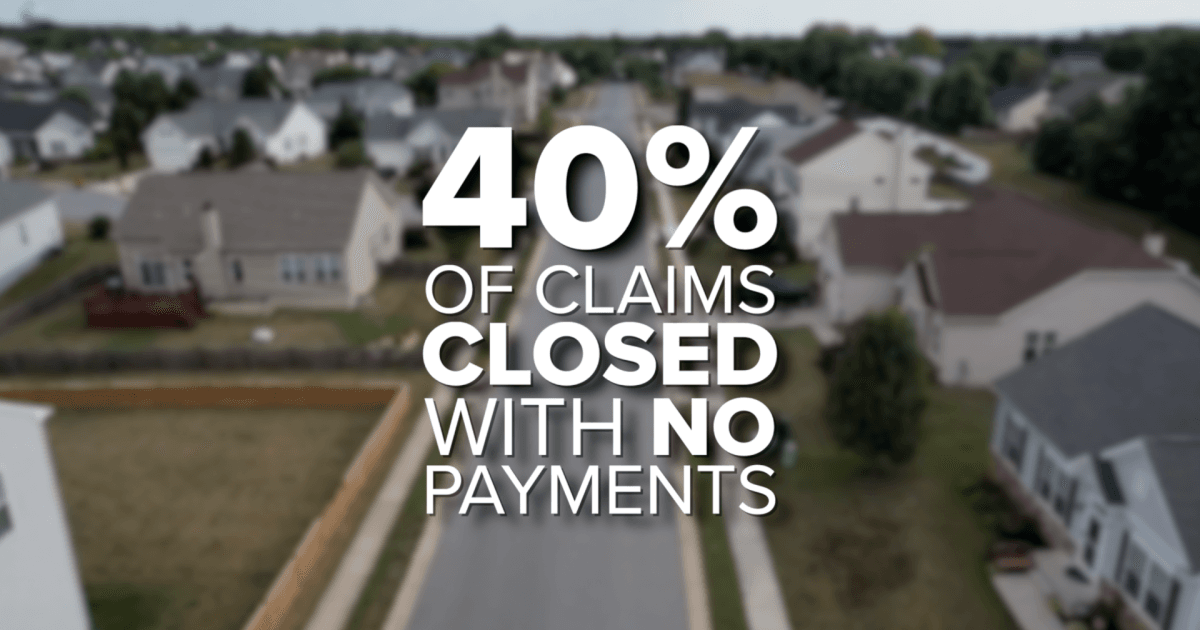

Florida homeowners are being hit with the highest insurance premiums in the nation, averaging $5,838 per year—nearly double the U.S. average. As costs skyrocket, many residents are reporting denied claims, non‑renewals, and impossible financial choices. New investigations reveal that more than 40 percent of claims in Florida close with no payment, while lawmakers push for transparency, fair pricing, and meaningful reform to stabilize a market that’s rapidly becoming unsustainable.

Vend Park, a Boston-based proptech company, has raised $17.5 million in Series A funding to reinvent parking as a high-performing commercial real estate asset. By replacing outdated operator–vendor systems with a unified AI-driven platform, Vend Park is helping major property owners boost NOI by up to 30%, slash operating costs, and modernize the tenant experience. As the company expands from three to fifteen cities and partners with giants like Nuveen and Jamestown, its technology highlights a major shift: real estate professionals must now understand AI, automation, and digital infrastructure to stay competitive.

Keller Williams Realty Atlanta Partners has formed an exclusive partnership with Southeast Mortgage, Georgia’s largest non‑bank mortgage lender. The collaboration promises faster, tech‑enhanced transactions for both agents and homebuyers, combining real estate expertise with streamlined mortgage services. This move reflects a growing trend toward integrated real‑estate ecosystems designed to reduce delays, boost transparency, and modernize the homebuying experience.

The information provided here is not investment, tax, or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

The information provided here is not investment, tax, or financial advice. You should consult with a licensed professional for advice concerning your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}