Conforming Mortgage Credit Availability Hits Record Low: What It Means for Today’s Borrowers

As 2026 unfolds, fresh data from the Mortgage Bankers Association (MBA) reveals something unexpected in the lending world: conforming mortgage credit availability has officially dropped to its lowest point since the index debuted in 2011. For today’s buyers and mortgage professionals, this shift is more than a headline—it’s a signal worth paying extremely close attention to.

Overall mortgage credit availability dipped by 2.6% in December, according to the MBA’s latest Mortgage Credit Availability Index (MCAI). This decline not only reverses two consecutive months of improvement but also pushes the MCAI down to 104.7—its lowest reading in three months.

Source Insight: Reporting for this development was originally published by Scotsman Guide, a trusted authority for mortgage and finance professionals nationwide.

A Tightening Market in a Time of Change

While mortgage credit availability still sits above year‑end 2024 levels, the December reading reveals a different narrative—one marked by lenders reducing program offerings and increasing documentation demands across many loan categories.

“Mortgage credit availability increased on an annual basis in December due to increased loan program offerings and industry capacity compared to the end of 2024,” said Joel Kan, MBA vice president and deputy chief economist. “However, on a monthly basis, credit supply declined to its lowest level in three months, with tightening in both conventional and government loan offerings.”

Kan noted that diminishing adjustable‑rate mortgage options, fewer cash‑out programs, and heightened documentation standards played major roles in this shift—changes that undeniably impact both buyers and mortgage pros working through today’s evolving lending landscape.

Historic Low for Conforming Loans

The Conforming MCAI saw the sharpest contraction, falling 3.8% and hitting its lowest point since tracking began more than a decade ago. The broader Conventional MCAI also dropped 3.6%, with jumbo lending moving in parallel.

Government‑backed programs weren’t immune either: FHA, VA, and USDA availability collectively declined by 1.4%.

For buyers, this tightening translates to fewer loan choices and stricter qualification hurdles. For real estate, lending, mortgage, and finance professionals, it highlights the need for staying educated, adaptable, and well‑versed in changing underwriting guidelines.

Why This Matters for Real Estate and Mortgage Professionals

When credit tightens, opportunities shift—not vanish. Professionals who stay ahead of lending trends and understand evolving credit landscapes are the ones who continue to thrive, even when market conditions tighten.

That’s where education becomes a powerful advantage. Whether you’re renewing a license, adding a new credential, or expanding into fields like real estate, mortgage origination, insurance, or finance, staying trained is essential.

Cameron Academy proudly supports professionals nationwide with flexible, career‑aligned licensing and continuing education—helping you stay sharp, informed, and ready for whatever comes next.

Looking Ahead

The December dip may be a temporary adjustment—or the start of a broader tightening cycle for 2026. Regardless, professionals who stay informed and anticipate these movements will maintain a competitive edge in serving their clients.

As the MBA continues tracking key lending shifts, one thing is clear: this year’s mortgage story is only just beginning, and those who stay educated will be best positioned to navigate it.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

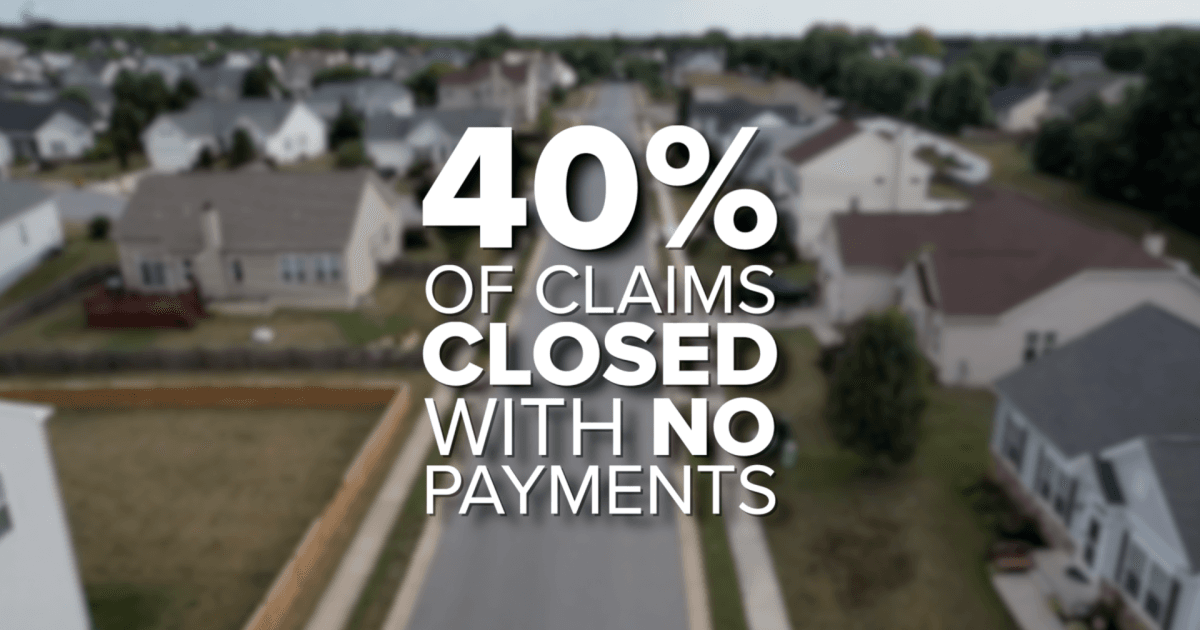

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}