Exploring Innovative Strategies for Managing Student Loan Payments

In a landscape where student loan debt is a growing concern, borrowers are exploring creative methods to manage their financial obligations. According to EducationData.org’s 2023 report, the average federal student loan borrower owes $37,574, while private borrowers face an even steeper average of $54,921. With these daunting figures, many are considering unconventional methods to ease their financial burden.

Contact Your Lender

For those with private loans, reaching out to your lender can reveal whether credit card payments are an option. While not all lenders offer this flexibility, some do, providing a possible avenue for managing payments more conveniently.

Utilize Third-Party Payment Platforms

Federal student loan borrowers might consider third-party platforms like PaySimply and Plastiq. These services enable payments via credit card by converting them into wire transfers or cash equivalents, although fees ranging from 2.5% to 3% can offset any potential rewards benefits.

Consider a Balance Transfer

For those nearing the end of their loan term, transferring the balance to a 0% APR balance transfer credit card could be a viable option. This method can provide an interest-free period of up to 21 months, though it comes with a transfer fee of 2% to 3%.

Creative Budgeting

A strategic approach involves reallocating expenses. For example, paying for groceries with a credit card can free up cash for student loan payments, achieving the same financial effect without direct loan charges.

Cash Advances

While not ideal due to high APR rates and immediate interest accrual, cash advances can be a last-resort option. Borrowers should weigh the costs carefully before proceeding.

Explore Deferment and Forbearance

Federal loan holders should explore deferment and forbearance options, which offer payment relief without credit damage. Private lenders may also provide hardship plans, though these vary by institution.

While these strategies can provide temporary relief, borrowers must remain vigilant about the potential pitfalls, such as high interest rates and the risk of accumulating more debt. The original article by Erica Sandberg on CardRates.com emphasizes the importance of informed financial decisions and responsible credit management.

CSS for Styling

“`css

h3 {

color: #b40101;

margin-bottom: 20px;

}

h4 {

color: #b40101;

margin-top: 30px;

margin-bottom: 10px;

}

p {

margin-bottom: 15px;

}

b {

color: #b40101;

}

a {

color: #b40101;

text-decoration: none;

}

a:hover {

text-decoration: underline;

}

img {

margin: 20px 0;

max-width: 100%;

height: auto;

}

“`

This approach ensures that borrowers are equipped with the knowledge to navigate their financial landscape effectively, prioritizing both short-term relief and long-term financial health.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A growing share of American homeowners now carry mortgage rates above 5%—a dramatic shift that’s reshaping refinancing, inventory, and buyer behavior nationwide. With more than 30% of borrowers locked into rates over 5% and 20% above 6%, the market is split between owners holding on to low pandemic‑era loans and new buyers taking on higher‑rate mortgages. Federal efforts to push rates down could unlock millions of refinancing opportunities, while buyers see only modest monthly savings. For real estate professionals, understanding these rate dynamics is crucial as they increasingly drive inventory levels, affordability, and market activity.

New Moody’s data shows commercial real estate deal volume slipped 20% in December, marking a second monthly decline. Yet the full year tells a different story: 2025 ended with a 17% gain, signaling a quiet but resilient recovery. The biggest surprise came from the office sector, which posted a 21% jump in activity as return‑to‑office trends and AI‑driven job growth boosted demand. Multifamily, retail, and alternative assets like data centers also saw strong momentum, giving real estate professionals a market full of fresh opportunities heading into 2026.

Florida drivers and industry professionals are heading into 2026 with good news: auto insurance rates are dropping across the state as the market shows strong signs of stabilization. USAA leads the latest wave with a 7% average rate decrease expected in May 2026, saving members more than $125 million annually. They join several major insurers — including State Farm, Progressive, AAA, Allstate, and Florida Farm Bureau — all approving significant reductions. Officials credit recent legislative reforms, especially tort reform, for the improved loss ratios and renewed insurer confidence. With both auto and home insurance markets strengthening, Florida’s real estate, mortgage, and insurance professionals can expect more consumer confidence, smoother transactions, and expanding career opportunities.

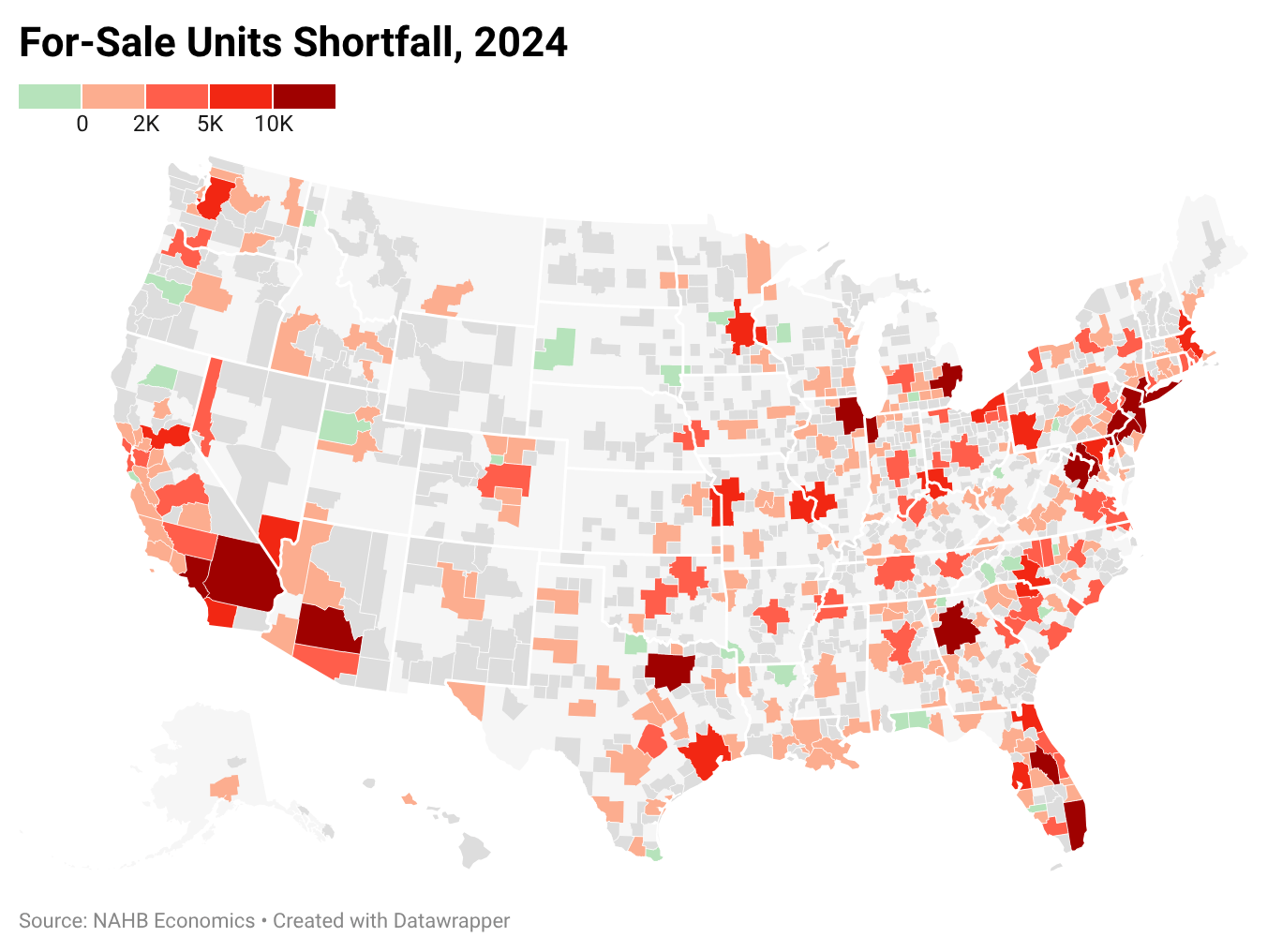

New data from Eye On Housing and the NAHB shows the U.S. remains short more than 1.2 million housing units, keeping pressure on both rents and home prices. Record‑low vacancy rates, slow single‑family construction, and restrictive zoning continue to fuel intense competition in 2024. Major metros like Chicago, New York, and Atlanta face some of the deepest deficits, and the true nationwide shortfall may be even higher when accounting for overcrowding and aging homes. For real estate professionals, the ongoing shortage means sustained demand, tighter inventory, and major opportunities for those who understand the evolving market.

Top real estate coach Jason Pantana says the divide between agents today isn’t about who has “tried” AI — it’s about who is immersed in it. In a new HousingWire interview, he explains why AI isn’t a gimmick but a full business system that amplifies output, improves authenticity, and reshapes how clients search for agents. From prompt mastery to AI‑driven visibility on Google, Pantana reveals how agents who commit even 15 minutes a day to learning AI are already outperforming those who hesitate.

Dallas–Fort Worth’s commercial real estate market closed 2025 with a split personality. Industrial dominated with massive new deliveries and soaring leasing demand, retail held steady with some of the market’s strongest fundamentals in years, and office continued to falter under remote‑work pressures. High vacancies, weak absorption, and rising demand for top‑tier space show the sector’s ongoing reset. Meanwhile, industrial and retail strength position the Metroplex for another powerhouse year heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}