Flood Disclosures Take Center Stage as Massachusetts Faces a Wetter Future

For 35 years, Denise Kress has woken up to the natural beauty of Belle Isle Marsh just beyond her Winthrop backyard. But the marsh, once a peaceful view, has increasingly become an unpredictable force of nature — one capable of swallowing cars, flooding basements, and turning daily life into a never‑ending battle with water.

Kress has endured totaled vehicles, ruined heating systems, and even hotel stays after her basement froze over in 2018. Yet, she remains — comforted by the same marsh that challenges her. Still, she wonders what will happen the day she eventually sells her home.

“I would want the next owner to know,” she says. “People have a right to know.”

A Push for Flood Transparency

As climate conditions worsen, Massachusetts Gov. Maura Healey is pushing a proposal that could reshape property transactions statewide: mandatory flood disclosures. With Massachusetts being one of only 14 states — and just three on the coast — with no disclosure requirements, the goal is simple: ensure buyers understand the risks before signing on the dotted line.

The proposal is part of Healey’s nearly $3 billion environmental bond bill aimed at updating dams, stormwater systems, and coastal defenses. But for real estate professionals, the disclosure requirement is the real game‑changer.

Why Flood Disclosures Matter

Flood histories directly affect insurance rates, property values, and long‑term financial stability. Without disclosures, buyers may unknowingly take on high‑risk properties. Transparency protects consumers while creating a fairer marketplace.

A Divided Real Estate Landscape

Support for the proposal comes from the business community, insurance experts, and municipalities. But one major player remains hesitant: the real estate industry.

The Massachusetts Association of Realtors argues that the rule disrupts the traditional “buyer beware” structure, shifting more responsibility onto sellers. Others believe the focus should be on increasing housing availability before adding major regulatory changes.

Still, economists — including Redfin’s chief economist — say disclosures create a more stable and trustworthy housing market.

Real Lives, Real Consequences

The debate isn’t theoretical. Former Salem homeowner Carole McCauley faced the issue firsthand after a 2011 storm flooded her basement with three feet of water, destroying her sump pumps, water heater, and car. When selling her home later, she did not disclose the flood history.

“I felt like a real jerk,” she admits — an all‑too‑common dilemma when laws don’t require transparency.

A Costly Lesson in a Changing Climate

McCauley says the experience reshaped her understanding of climate change, finances, and personal responsibility. “This isn’t just about science,” she says. “It’s about people’s retirement, their savings… their lives.”

The Road Ahead

Healey’s proposal now enters the legislative arena next year, raising major questions about transparency, safety, and the future of homeownership in a rapidly changing climate.

As one flood expert describes it, avoiding flood disclosure is like playing “a perverse game of musical chairs.” Eventually, someone gets stuck with a home that floods too often to sustain.

What This Means for Real Estate Professionals

Mandatory flood disclosures could reshape Massachusetts’ real estate environment. For anyone pursuing or maintaining their real estate license, understanding these shifts is essential.

At Cameron Academy, we emphasize ethical representation, consumer protection, and staying ahead of industry‑wide changes. For new and seasoned professionals alike, knowledge of flood disclosure laws helps build trust and elevate your practice.

To explore the original reporting behind this story, visit Commonwealth Beacon:

commonwealthbeacon.org

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

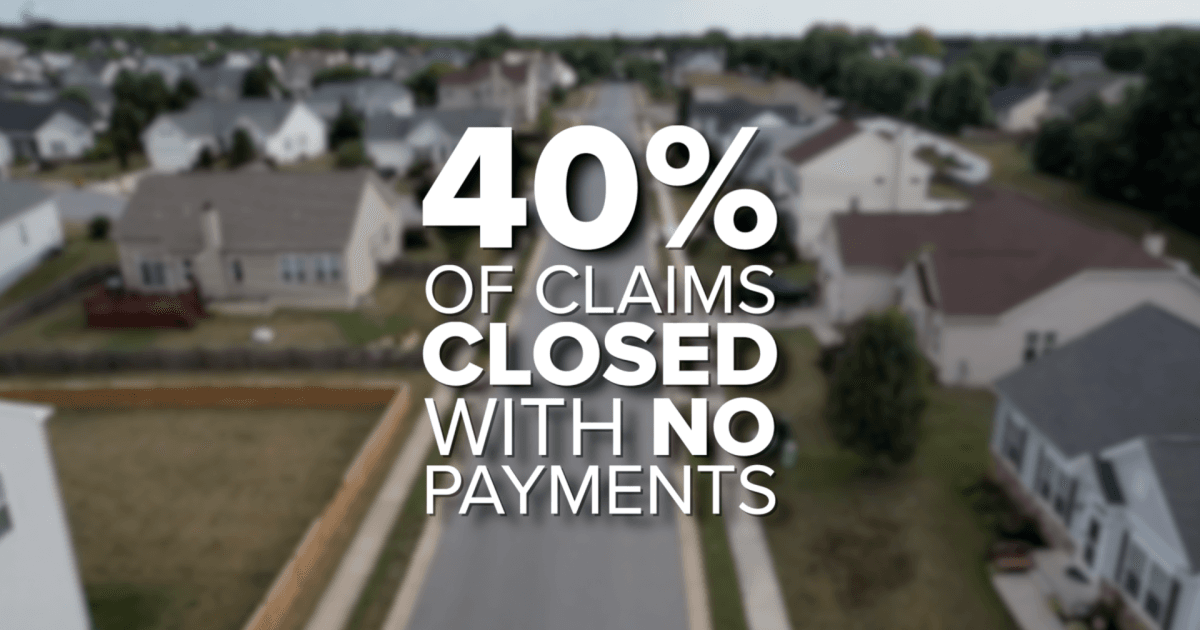

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}