Florida Ends Insurance Assessment Early, Saving Homeowners Millions

Florida homeowners just scored a rare financial win — and it’s a big one. The emergency insurance assessment added after a wave of insurer bankruptcies has been paid off two full years ahead of schedule. This fast payoff translates into more than $650 million in savings statewide, bringing long‑awaited relief to residents who have endured years of climbing premiums.

The assessment, around $30 annually for most homeowners, was originally created after Hurricane Ian triggered the collapse of 10 insurance companies, including United Property and Casualty. When those companies failed, the financial pressure fell directly on residents. Many policyholders had no idea they were paying the fee — until now, when it’s about to vanish.

Tap to reflect: Did you know you were paying this assessment each year?

What This Means for Florida Homeowners

Insurance Information Institute spokesperson Mark Friedlander emphasized how unusual this positive news is. The strengthening of Florida’s insurance market allowed the debt to be retired early, unlocking more than half a billion dollars in savings over the next two years.

Residents like Alexa Stevenson of Fort Myers say the timing is perfect. “In this economy, it’s tough — and to know we’re going to save a little bit is nice,” she shared.

Even incoming homebuyers, including new retirees like Doreen Eldred, view this as a much‑needed shift. Still, she warns that one major storm could change everything again. For aspiring real estate agents, mortgage professionals, and insurance specialists, these shifts are critical to understand in today’s Florida market.

Why This Matters to Real Estate Professionals

Insurance expenses are now one of the biggest deal‑makers or deal‑breakers for buyers. Whether you’re guiding clients or navigating your own policy, the end of this assessment helps restore a sense of stability across Florida’s real estate and lending landscape.

At Cameron Academy, we see firsthand how insurance trends shape the careers of real estate and insurance students. A more balanced market means more confident buyers — and more opportunities for professionals ready to step into the field.

Insight: If you’re considering a Florida real estate or insurance career, moments like this highlight why staying educated and licensed matters.

Source Spotlight

This developing story was originally reported by Gulf Coast News. Explore their full coverage and stay informed about Florida’s shifting insurance and housing markets:

Read the full report on Gulf Coast News.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

The title insurance industry is entering 2026 with a renewed focus on technology, operational efficiency, and stronger agent support after years of volatility. Leaders from major underwriters report rising transaction activity, improved affordability, and a surge in automation and fraud‑prevention tools—signs that smarter systems and better training will define the next wave of growth.

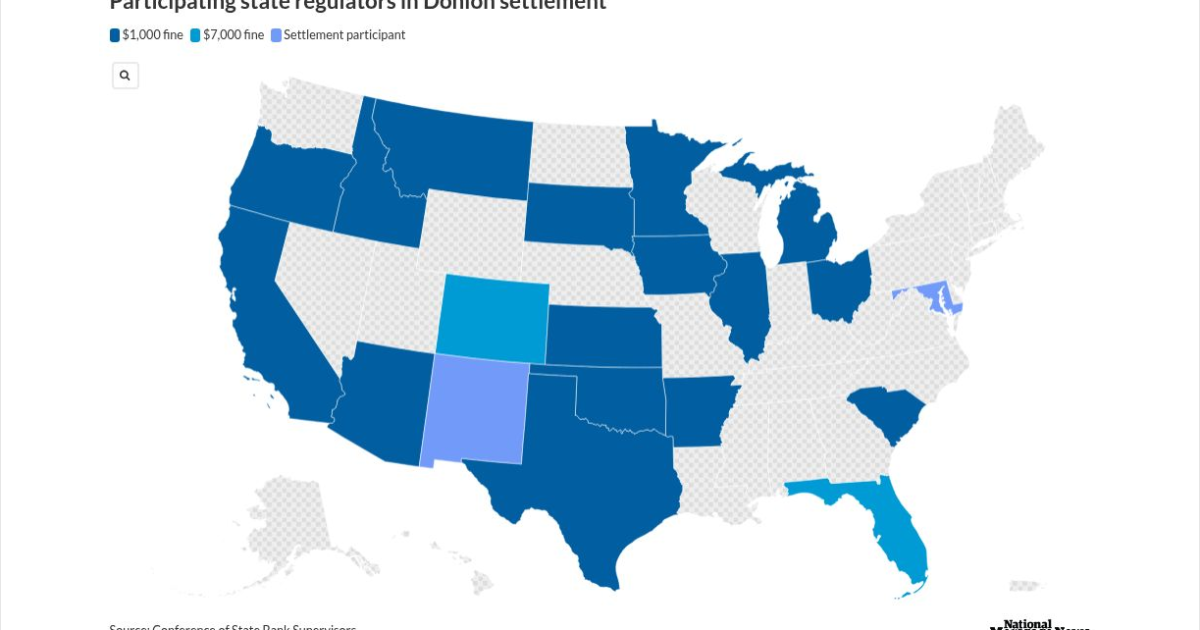

A multistate crackdown has sent shockwaves through the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, accepted a sweeping settlement that bans him from working as a mortgage loan originator in 21 states—19 of them permanently. Regulators say Donlon had another individual complete his mandatory licensing and continuing‑education courses, a violation that triggered a coordinated investigation and a $31,000 penalty. The case underscores regulators’ growing intolerance for education fraud and serves as a sharp reminder to industry professionals: cutting corners on licensing can end careers.

Florida’s once‑booming housing market is cooling fast as rising insurance premiums, increasing foreclosures, and expanding flood zones push buyers to back out of deals and force sellers to cut prices. With insurance now adding thousands to annual housing costs, professionals across real estate, mortgage, and insurance are navigating a dramatically shifting landscape that’s redefining affordability in the Sunshine State.

Florida begins 2026 with a wave of more than 250 new laws now in effect, impacting healthcare, insurance, real estate, and consumer protections statewide. From free breast cancer screenings for state employees to tighter pet insurance regulations, mandatory healthcare refund rules, enhanced animal‑cruelty penalties, and new condo‑management requirements, these updates carry major implications for professionals navigating Florida’s evolving regulatory landscape.

Florida’s barrier islands may offer postcard-perfect beaches and soaring real estate demand, but they’re also some of the most fragile and costly places to build in the United States. With 765,000 residents living on land that shifts, sinks, and takes the brunt of every major hurricane, the financial and insurance risks are accelerating fast. From billion‑dollar beach rebuilds to towers settling into the sand, today’s coastal development challenges are reshaping conversations around property values, disclosure, and long‑term resilience. For real estate professionals, understanding these risks isn’t just smart — it’s becoming essential.

A Cedar City development is turning heads with its fresh approach to affordability. The team behind Temple View Commons is delivering luxury‑inspired twin homes at prices below the local median by using a small, hands‑on staff and cutting traditional costs like realtor commissions. In a tight Utah housing market where inventory is scarce and prices remain high, their strategy offers a realistic path to homeownership without sacrificing high‑end finishes.

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}