Florida’s Citizens Insurance Proposes Rare Rate Cuts for 2026 — Here’s What It Means for You

In a surprise move that could reshape Florida’s property insurance landscape, Citizens Property Insurance Corp. is recommending lower rates for many of its policyholders in 2026. For millions of Florida homeowners who’ve watched premiums rise year after year, this news marks a meaningful—and overdue—shift in the state’s insurance narrative.

You can read the original full report at Miami Times Online here: Miami Times Online.

A First in Over a Decade

The Citizens Board of Governors approved the recommended reductions last Wednesday. If the state’s Office of Insurance Regulation approves, it would be the first time since 2015 that policyholders see premiums decrease instead of climb.

Statewide personal-line policies would drop an average of 2.6%. According to Citizens’ official rate kit, three out of five policyholders could see savings as high as 11.5% — roughly $359 annually.

See the County-by-County Breakdown

Citizens has released a full county‑by‑county projection outlining which areas will see decreases and which may still face increases. Explore the full report here: View PDF.

Why Are Rates Going Down?

Citizens officials credit major insurance‑market reforms enacted throughout the decade. These changes, championed by Gov. Ron DeSantis and the Florida Legislature, targeted fraudulent claims and excessive litigation — two long‑standing contributors to market instability.

“Critical reforms… have done what they were supposed to do: provide rate relief to policyholders and stability to the Florida market,” said Citizens CEO Tim Cerio.

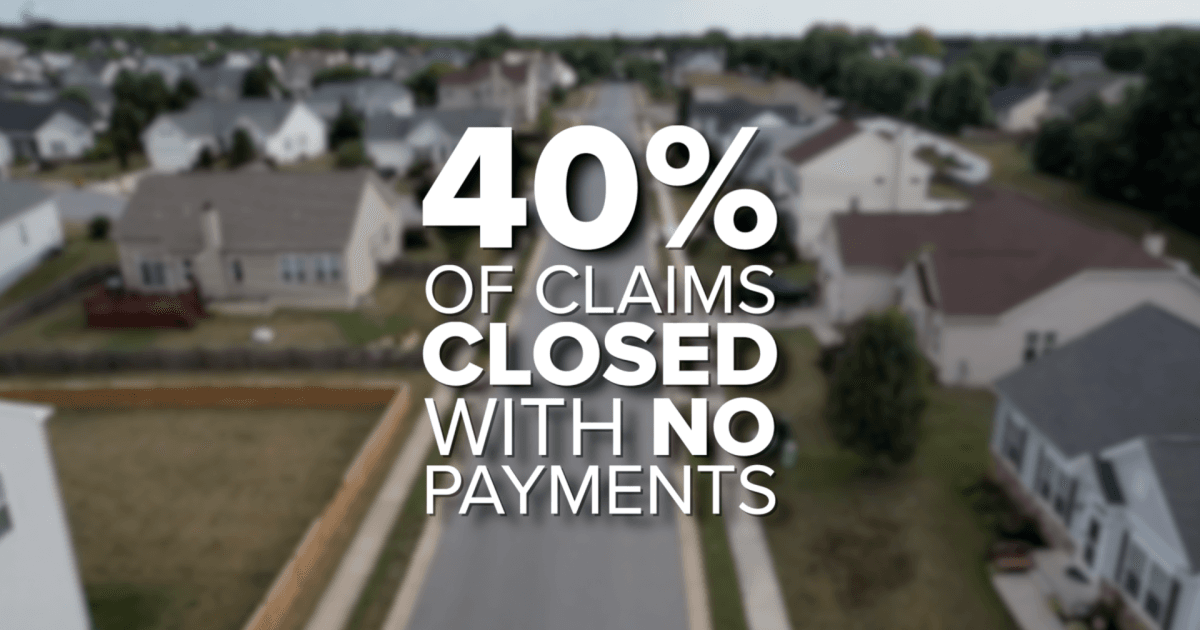

Signs of stabilization already show promise. Since these reforms took effect, 17 new insurers have entered the Florida market. Citizens itself has shrunk dramatically — from a record 1.42 million policies in 2023 to just 385,000 this year. More than half a million policies have returned to private insurers.

The Catch: Not Everyone Will See a Decrease

Reductions won’t be universal. Some counties may still experience increases due to risk exposure, claim frequency, or regional vulnerabilities.

This uneven impact highlights Florida’s continuing challenge: balancing affordability with the realities of a storm‑prone, high‑risk property market.

What Happens Next?

The proposed rate cuts will now be reviewed by the Florida Office of Insurance Regulation, which will hold public hearings before issuing a final ruling. If approved, the new rates would take effect June 1, 2026.

Why This Matters for Real Estate and Insurance Professionals

Lower premiums could reignite Florida’s real estate market — particularly in coastal and high‑risk zones where high insurance rates have discouraged buyers. For real estate agents, insurance professionals, and mortgage specialists, understanding these shifts is essential for guiding clients through 2025 and beyond.

For those entering the industry or expanding their credentials, Cameron Academy continues to support Florida’s growing workforce with licensing programs in real estate, insurance, mortgage, and more — ensuring professionals stay prepared as the market evolves.

Final Takeaway

The proposed 2026 Citizens rate cuts signal cautious optimism for Florida’s property market. After years of volatility, the landscape finally shows signs of stabilizing — and for many Floridians, meaningful relief could be just months away.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}