Florida’s 3.35% Home Insurance Non‑Renewal Rate: Why Hundreds of Thousands Lost Coverage

Florida’s insurance market has always had a flair for the dramatic, but last year’s numbers took things to a new level. A 3.35% non-renewal rate may sound small, yet in a state with millions of homeowners, it translates to hundreds of thousands suddenly losing their insurance coverage. It’s the kind of statistic that makes any Floridian pause mid‑coffee sip.

For real estate agents, mortgage professionals, insurance licensees, and homeowners, this shift is more than a headline—it’s a reshaping of Florida’s risk profile. And understanding these changes is becoming essential for anyone working around property. If you’re in the industry and need to stay ahead, continuing education through Cameron Academy can help keep your expertise sharp.

When Storm Damage Becomes a Breaking Point

Florida’s storms are practically characters in our yearly storyline—dramatic, recurring, and often costly. Over recent years, however, the financial aftermath has escalated. NAIC data reveals that Florida leads the nation in non-renewals, with insurers stepping back after repeated storm‑related claims.

Insurers aren’t acting on emotion. When storms become more frequent and more destructive, payouts skyrocket. Eventually, companies tighten underwriting standards or withdraw entirely from high‑risk zones. The irony is hard to miss: the same storms that make insurance essential also make it harder to keep.

The Rising Cost of Rebuilding

The weather isn’t the only culprit. Rising construction expenses—driven by labor shortages, material costs, and lingering supply chain issues—mean each claim costs insurers more than it would have just a few years ago.

As construction costs continue climbing, insurers adjust their risk models, premiums shift upward, and coverage criteria tighten. Homeowners feel the effects long before they ever see the spreadsheets causing it all.

The Legal Landscape: Fraud and Litigation

Florida has long been known for its intense volume of insurance-related litigation. While many claims are legitimate, the sheer quantity of lawsuits—some unnecessary—adds immense financial pressure to insurers.

These expenses ripple outward to homeowners as higher premiums or lost coverage. Even with recent reforms meant to cool the market, improvements will take time. Until then, detailed documentation remains a homeowner’s strongest defense.

Insurers Shrinking Their Footprint

One of the most dramatic developments has been the number of insurers reducing—or outright ending—their operations in Florida. When providers leave, competition shrinks, prices rise, and homeowners face fewer options.

Many affected residents turn to Citizens Property Insurance Corporation, the state-backed insurer of last resort. While essential, Citizens was never intended to hold such a large market share. Today, shopping early and comparing multiple carriers is becoming a must-do rather than an option.

Everyday Homeowners Caught in the Middle

Losing insurance coverage isn’t just inconvenient—it can jeopardize mortgages, stall repairs, or create major financial strain. Many homeowners report receiving premium increases double or triple what they previously paid.

Proactive upgrades—modern roofs, wind mitigation improvements, regular maintenance, and detailed documentation—can help maintain good standing with insurers.

What Homeowners Can Do Moving Forward

While homeowners can’t control the weather or underwriting algorithms, they can take steps to stay protected. Start shopping for renewal options early, maintain your property diligently, and stay informed as legislative shifts continue.

For real estate and insurance professionals, knowledge is your currency. If you’re earning or upgrading your license, Cameron Academy offers flexible, affordable programs built to keep you competitive in a changing market.

A Market in Motion

Florida’s 3.35% non-renewal rate isn’t just a statistic—it’s a snapshot of an evolving marketplace shaped by storms, rising costs, legal pressures, and insurer strategies. The professionals who understand these forces will be the ones best positioned to guide homeowners through uncertainty.

What changes have you seen in your own insurance situation? Share your experience below.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida’s property insurance system is once again spiraling as new “market-friendly” reforms fail to stabilize rising premiums, insurer failures, and mounting homeowner frustration. Despite aggressive efforts to shift policyholders from Citizens to private carriers, many of the new insurers stepping in are tied to past insolvencies, questionable ratings, and political influence. For real estate, mortgage, and insurance professionals, these systemic cracks are reshaping closings, valuations, and risk across the state—making it essential to stay ahead of ongoing regulatory and market shifts.

Commercial real estate is heading into a turning‑point year in 2026, driven by economic uncertainty, AI‑powered transformation, shifting demographics and rising portfolio risk. Insights from The Counselors of Real Estate highlight the top issues shaping the year ahead—from fiscal pressures and capital constraints to housing shortages, global volatility and the future of data‑driven decision‑making. For real estate, mortgage, insurance and finance professionals, these trends offer a clear roadmap for staying competitive and preparing for the next wave of industry change.

AI-powered tools, fraud protection systems, and smarter MLS integrations are sweeping through the real estate industry as major organizations adopt new technologies. From RealReports hitting its 50th partnership to BeachesMLS unveiling instant AI home visualizations and Doorify boosting security, professionals are seeing rapid advancements that promise sharper insights, safer transactions, and more efficient rental workflows. This evolving tech landscape underscores the importance of staying educated and adaptable — especially for agents preparing for a competitive, AI-enhanced 2025 market.

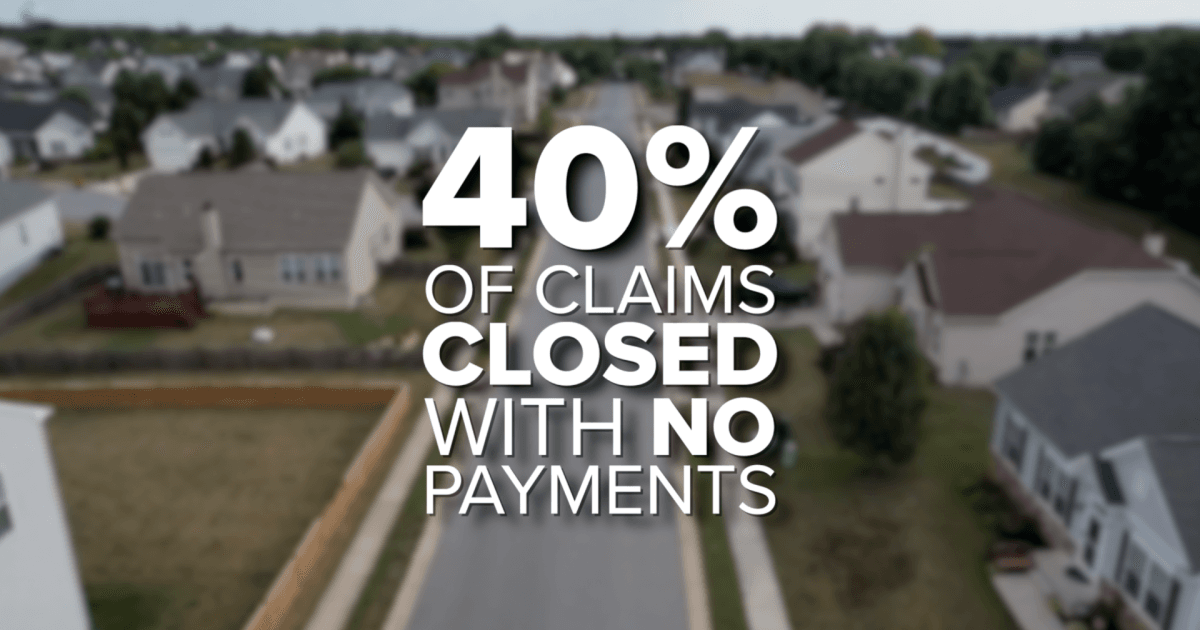

Florida homeowners are being hit with the highest insurance premiums in the nation, averaging $5,838 per year—nearly double the U.S. average. As costs skyrocket, many residents are reporting denied claims, non‑renewals, and impossible financial choices. New investigations reveal that more than 40 percent of claims in Florida close with no payment, while lawmakers push for transparency, fair pricing, and meaningful reform to stabilize a market that’s rapidly becoming unsustainable.

Vend Park, a Boston-based proptech company, has raised $17.5 million in Series A funding to reinvent parking as a high-performing commercial real estate asset. By replacing outdated operator–vendor systems with a unified AI-driven platform, Vend Park is helping major property owners boost NOI by up to 30%, slash operating costs, and modernize the tenant experience. As the company expands from three to fifteen cities and partners with giants like Nuveen and Jamestown, its technology highlights a major shift: real estate professionals must now understand AI, automation, and digital infrastructure to stay competitive.

Keller Williams Realty Atlanta Partners has formed an exclusive partnership with Southeast Mortgage, Georgia’s largest non‑bank mortgage lender. The collaboration promises faster, tech‑enhanced transactions for both agents and homebuyers, combining real estate expertise with streamlined mortgage services. This move reflects a growing trend toward integrated real‑estate ecosystems designed to reduce delays, boost transparency, and modernize the homebuying experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}