Florida’s Insurance Crisis: Why Premiums Keep Rising and What It Means for Homeowners

Florida’s property insurance market is once again under the microscope, and a newly released report suggests the problems plaguing homeowners aren’t going away anytime soon. In fact, many of the issues that sparked previous market collapses appear to be resurfacing—just under new branding.

The report, published by the Insurance Fairness Project and highlighted by InsuranceNewsNet, breaks down what the organization calls the “mirage” of Florida’s insurance comeback. Despite political messaging about recovery since Hurricane Ian in 2022, the data shows rising premiums, fragile insurers, and a climate of uncertainty that leaves homeowners seriously exposed.

Click to Reveal: How Much Have Premiums Increased?

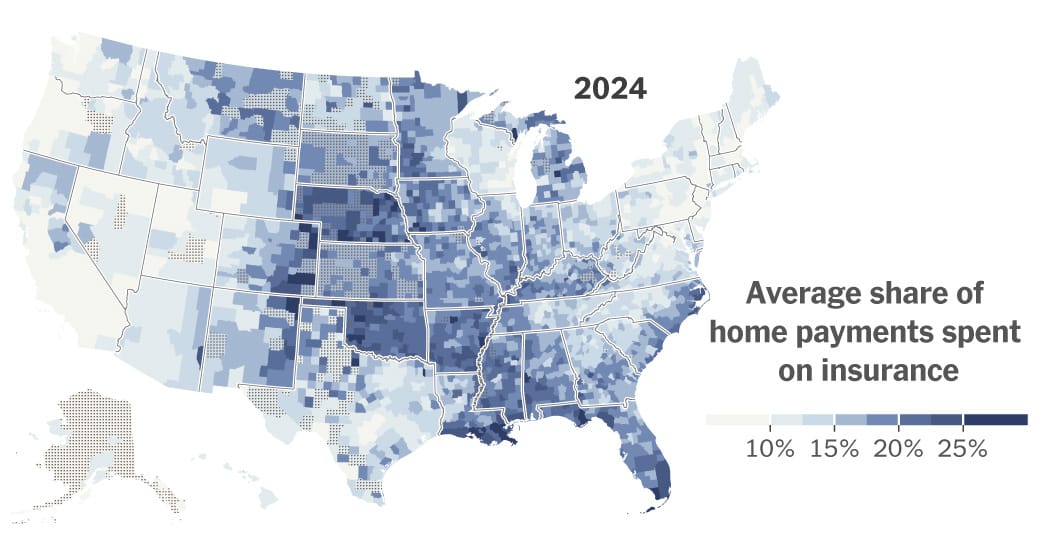

According to the report, Florida homeowners are paying 54% more for property insurance since 2019—now the highest rates in the nation. Even more alarming: an estimated 20% of Florida homeowners have stopped carrying insurance altogether.

The Hidden Weakness Behind the “Recovery”

A major concern is who is entering the insurance market. The report claims that several “new” insurers are simply rebranded versions of previously failed companies—or are led by executives tied to earlier insolvencies. Combined with weak oversight and questionable rating standards, the situation creates a landscape where consumers may feel protected but face significant vulnerability when claims actually arise.

Shifting policy risk from Citizens Property Insurance Corp. to small private firms has additionally created an ecosystem where the financial burden is concentrated among companies that may not survive a major catastrophe.

Troubling Performance Stats

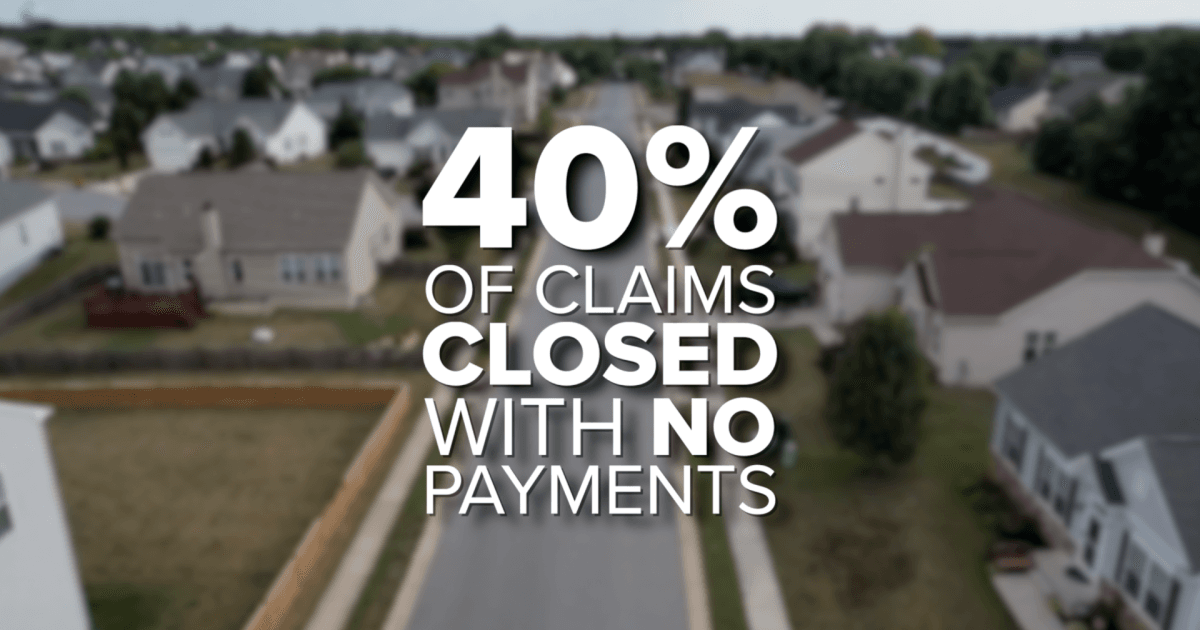

• Florida leads the nation in unpaid property claims: 40.3% closed with no payout.

• Florida ranks first in policy non-renewals: 3.3% of all in-force policies.

• Florida ranks fourth in delayed claims: 32.8% delayed more than 60 days.

Lawmakers Step In: New Bills Aim for Transparency

State Sen. Carlos Guillermo Smith has introduced two bills—SB 234 and SB 230—seeking to increase oversight, require public disclosure of insurer affiliate payments, cap managing agent fees, and limit what financial data insurers can hide by labeling it a “trade secret.”

If enacted, these bills could represent a meaningful shift toward consumer protection and market accountability.

What This Means for Homeowners, Agents, and Industry Professionals

For homeowners, the message is clear: insurance costs may remain high, and claim reliability is far from guaranteed. For real estate agents and brokers, understanding these risks is essential for advising clients and navigating transactions.

Professionals in the insurance field—especially those entering or advancing their careers—should closely follow these developments. Knowing how Florida’s market truly functions can be a major competitive advantage.

That’s where strong professional education comes in. If you’re looking to build or expand your credentials in insurance, real estate, or mortgage services, high-quality training matters. Cameron Academy offers licensing and continuing education programs designed to help professionals stay ahead in challenging markets like Florida’s.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}