As Hurricane Milton looms over Florida’s Gulf Coast, residents brace for yet another bout of extreme weather. Despite the increasing frequency and intensity of hurricanes, wealthy homeowners in Florida seem unfazed. In fact, the impact of these natural disasters on the housing market is reshaping the demographic landscape, but not in the way one might expect.

A recent Slate article delves into the phenomenon of climate migration, revealing that it’s not leading to an exodus of affluent individuals from Florida. Instead, the hurricanes are driving up housing prices and attracting higher-income groups, while lower-income residents face displacement. This trend, often referred to as “climate gentrification,” contradicts the popular notion that wealthier households would relocate to safer areas.

Florida’s post-pandemic growth has been remarkable, with the state surpassing New York as the third-most populous in the U.S. Four of the nation’s five fastest-growing metro areas are in Florida, including Cape Coral–Fort Myers, which was severely impacted by Hurricane Ian in 2022. Yet, the Wall Street Journal warns of a potential unraveling of the state’s growth due to climate challenges.

However, the data suggests otherwise. Research by Joshua Graff Zivin highlights how hurricanes constrain housing supply, leading to increased demand and higher prices. Economic instability often results in evictions, as landlords replace long-standing tenants with higher-income newcomers. The costs of recovery, such as emergency reconstruction and higher insurance premiums, are more manageable for affluent households.

Moreover, hurricanes not only drive up housing prices but also lead to demographic changes. A study by the National Low Income Housing Coalition found that affluent communities tend to lose their low-income housing stock during recovery, as landlords are incentivized to redevelop existing low-cost rentals into higher-cost housing.

In response to these challenges, some regions are taking legislative action. For instance, Sonoma County in Northern California recently passed an ordinance to pause evictions during disaster declarations. This measure aims to counter the trend of rising evictions post-disasters, but Florida has yet to implement similar rules.

Despite the insurance crisis following Hurricane Helene, the Reforming Disaster Recovery Act proposes long-term federal funding for low-income housing after disasters. Yet, the design of federal disaster assistance can sometimes lead to price gouging. For instance, in Hawai’i, rental assistance after the Lahaina fire resulted in landlords raising prices and evicting tenants.

Ultimately, the allure of Florida’s coastal properties remains strong. Even as insurance premiums rise and maintenance costs increase, people continue to pay a premium to live in these risky areas. No disaster has yet altered this calculus.

Styling and Design

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Skyrocketing insurance premiums and soaring rebuilding costs are transforming communities across Southwest Florida, especially in the wake of Hurricane Ian. As longtime residents struggle to keep up with rising financial pressure, wealthier newcomers and stricter building standards are reshaping the identity of places like Fort Myers Beach. With insurance rates now driving home sales, triggering potential foreclosures, and squeezing both owners and renters, Florida’s middle-class families face a growing question: can they afford to stay in the state they love?

Florida’s insurance industry is stabilizing fast, with nearly 1.6 million policies shifting from Citizens to private insurers and litigation dropping sharply. Regulators report stronger market confidence, decreasing premiums, and renewed competition—signaling one of the healthiest periods the state has seen in years.

A Leon County judge has ordered the restart of arbitration for Citizens Property Insurance claims, directly conflicting with a previous ruling that halted the process as potentially unconstitutional. With more than 400 cases now back in motion, real estate, insurance, and mortgage professionals can expect renewed activity in claim disputes and fresh uncertainty as Florida courts clash over the legality of Citizens’ arbitration system.

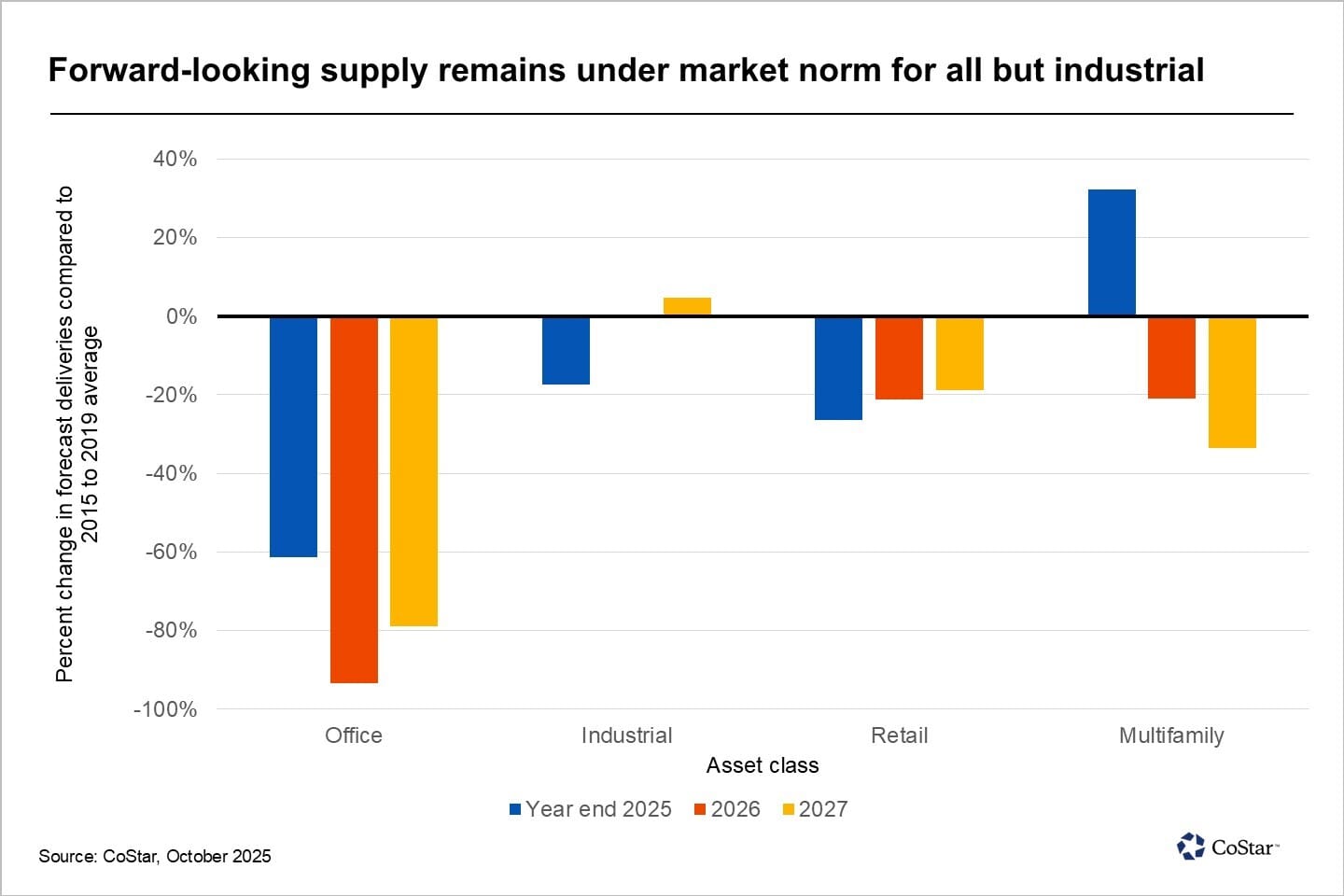

The DFW market is transitioning into a new construction phase marked by a slowdown in office development, a more selective approach to industrial projects, and an evolving housing landscape shaped by affordability and population growth. Developers are recalibrating their priorities, and for real estate professionals, understanding these shifts offers a critical edge in navigating—and capitalizing on—the next phase of the metroplex’s growth.

A new federal lawsuit claims Zillow pushed homebuyers toward Zillow Home Loans by rewarding affiliated agents with valuable leads — all without proper disclosure. The suit alleges undisclosed incentives, referral quotas, and potential RESPA violations, raising major concerns about steering, fiduciary duties, and Zillow’s expanding mortgage ambitions.

The mortgage industry is evolving fast, and the lenders who come out on top will be those who innovate without uprooting what already works. By building on strong technology foundations, streamlining workflows and adopting smart automation, lenders can reduce costs, improve customer experience and stay resilient in any market cycle. This article breaks down why innovation matters now, how a stable tech ecosystem protects lenders in volatile conditions and why small, strategic steps can drive long-term transformation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}