How the LA Wildfires Exposed a Cracking Insurance System — And Why Professionals Across Industries Should Be Paying Attention

For a brief moment last January, after losing their Altadena home to the devastating Los Angeles wildfires, Jessica and Matt Conkle thought hope had arrived. Their insurer, State Farm, responded swiftly with emergency living expense checks — a gesture that felt like a lifeline during chaos.

But what followed was months of slow-motion frustration: multiple adjusters, lowball valuations, unreturned calls, and a rebuilding offer so far below market cost it couldn’t get construction started. What should have been a straightforward process became an exhausting battle for basic fairness.

“It was all delays and denials,” Jessica said. “It’s consuming all our time… and it’s inhuman.”

The Conkles’ story is far from unique — and that should concern every homeowner, real estate professional, and insurance provider in America.

A Crisis That Reaches Well Beyond Los Angeles

A much larger pattern is emerging. Reports from the nonprofit Department of Angels reveal that nearly 8 out of 10 wildfire survivors faced major obstacles collecting claims. Many who lost only part of their home faced even bigger hurdles than those who lost everything.

The LA recovery has become a symbol of a national crisis: an insurance system straining — and in some places breaking — under extreme climate volatility. Providers are raising premiums dramatically, reducing coverage, or abandoning high-risk regions altogether.

Yet, ironically, insurers aren’t suffering financially. The industry earned $169 billion in profit last year — a record — thanks largely to strong investment gains.

The Tension Between Risk and Responsibility

Insurance companies argue they need higher premiums to remain sustainable amid escalating disasters. Meanwhile, investigations show many are leveraging loopholes to avoid covering the customers who need them most — especially those living in fire-prone regions.

Regulators haven’t escaped criticism either. California insurance commissioner Ricardo Lara has faced accusations of prioritizing industry concerns over consumer protections, allowing steep price increases while offering minimal systemic reforms.

This imbalance sparked community backlash — including leaders like Joy Chen, whose public pressure helped accelerate stalled claims within days.

Climate Risk: The Growing Force Reshaping Homeownership

Global catastrophe losses are exploding. In 2025 alone, natural disasters caused over $145 billion in underwriting losses. Wildfires are only a portion of the total; storms and hurricanes contribute even more.

As private insurers pull back, government options like California’s Fair Plan are becoming the default — yet these programs are financially strained and unsustainable long-term.

“We’re marching toward an uninsurable future,” warns Dave Jones, former California insurance commissioner.

Experts say the industry must take bolder action: rewarding mitigation, rewriting replacement-cost formulas, and even leveraging their investment power to pressure fossil-fuel producers.

Why This Matters for Professionals Nationwide

Real estate agents, mortgage brokers, insurance agents, and financial planners are already feeling the tremors of this system shift.

Homebuyers can’t close deals without secured insurance.

Lenders face risk exposure when insurers drop coverage.

Agents must discuss climate risk disclosures more than ever.

Insurance professionals face tighter rules and scrutiny.

For those in Florida — where climate volatility and insurance instability are already present — the LA wildfire crisis is not a distant story. It is a preview.

Where Cameron Academy Fits Into This Moment

Cameron Academy continues to prepare rising and established professionals for real-world conditions, not just exam day. Whether you’re entering real estate, insurance, mortgage, finance, or expanding your licenses, understanding the impact of climate risk makes you more valuable — and indispensable to your clients.

Education isn’t just a requirement — it’s a professional advantage.

A Turning Point for the American Middle Class

Wildfire survivors like the Conkles aren’t asking for special treatment — just a fair return on the coverage they paid for. But their struggle reveals something deeper: the stability of American homeownership is being shaken by forces larger than any one family, insurer, or state.

Reform, price increases, and entirely new systems may emerge. But one truth remains: professionals across real estate and insurance will shape how Americans navigate the storms ahead.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

In 2026, financial advisors are no longer just experimenting with AI — they’re relying on it. Once confined to back-office duties, AI now supports meeting prep, portfolio analysis, and even early-stage financial planning. Advisors say the tech is strengthening client relationships by freeing them from administrative overload, though entry-level roles like paraplanners may feel the squeeze as automation accelerates.

Cybercriminals are weaponizing AI to launch highly convincing email scams and system breaches across the mortgage industry, overwhelming lenders and servicers whose cybersecurity measures can’t keep up. With major companies already hit and regulation lagging behind, experts warn the sector—now considered critical infrastructure—must rapidly upgrade protections, collaborate on threat intelligence, and improve AI governance before the risks escalate further.

Escrow payments are quietly surging across the country as property taxes and insurance premiums spike—pushing many homeowners toward delinquencies and even foreclosure. New data from Cotality shows the sharpest increases hitting the South and Midwest, with Florida among the hardest‑hit states. Even with fixed mortgage rates, rising escrow requirements are driving monthly payments higher and threatening affordability heading into 2026.

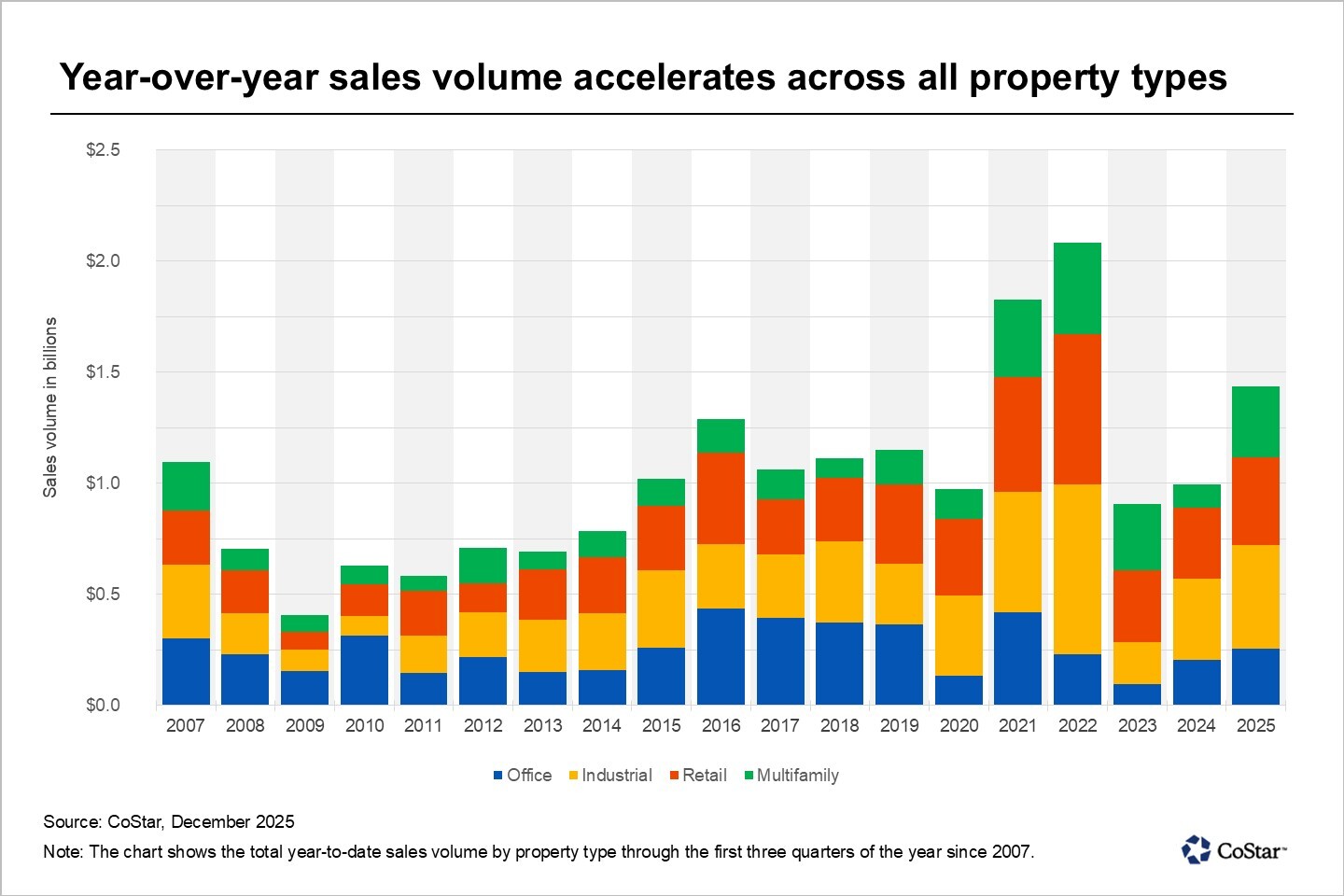

Milwaukee entered 2025 with renewed momentum, posting its strongest commercial real estate sales volume in three years. After a period of uncertainty and high capital costs, investors are returning with a sharper focus on quality assets, realistic pricing, and reliable cash flow. Activity is increasing across industrial, office, multifamily, and retail sectors, signaling a broad-based recovery fueled by stabilizing interest rates and improved market confidence.

As 2026 approaches, the title insurance industry is navigating a complex mix of market recovery, rising fraud threats, and sweeping regulatory changes. Industry leaders say the path forward centers on smarter technology, leaner operations, and stronger support for title agents. With AI-driven workflows, enhanced fraud prevention, and new compliance demands—including FinCEN’s expanded Geographic Targeting Orders—companies like Stewart and First American are reshaping how title work gets done. For real estate and mortgage professionals, the year ahead promises more automation, heightened standards, and major opportunities for those who stay ahead of the curve.

The real estate industry is undergoing a major transformation in 2025 as advancements in AI, proptech, blockchain, and data intelligence redefine how properties are marketed, valued, financed, and experienced. From instant digital valuations and immersive virtual tours to tokenized investments and predictive analytics, technology is reshaping every stage of the real estate lifecycle. Professionals who embrace these innovations—while maintaining the human expertise clients still rely on—will lead the next era of the industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}