How the LA Wildfires Exposed a Cracking Insurance System — And Why Professionals Across Industries Should Be Paying Attention

For a brief moment last January, after losing their Altadena home to the devastating Los Angeles wildfires, Jessica and Matt Conkle thought hope had arrived. Their insurer, State Farm, responded swiftly with emergency living expense checks — a gesture that felt like a lifeline during chaos.

But what followed was months of slow-motion frustration: multiple adjusters, lowball valuations, unreturned calls, and a rebuilding offer so far below market cost it couldn’t get construction started. What should have been a straightforward process became an exhausting battle for basic fairness.

“It was all delays and denials,” Jessica said. “It’s consuming all our time… and it’s inhuman.”

The Conkles’ story is far from unique — and that should concern every homeowner, real estate professional, and insurance provider in America.

A Crisis That Reaches Well Beyond Los Angeles

A much larger pattern is emerging. Reports from the nonprofit Department of Angels reveal that nearly 8 out of 10 wildfire survivors faced major obstacles collecting claims. Many who lost only part of their home faced even bigger hurdles than those who lost everything.

The LA recovery has become a symbol of a national crisis: an insurance system straining — and in some places breaking — under extreme climate volatility. Providers are raising premiums dramatically, reducing coverage, or abandoning high-risk regions altogether.

Yet, ironically, insurers aren’t suffering financially. The industry earned $169 billion in profit last year — a record — thanks largely to strong investment gains.

The Tension Between Risk and Responsibility

Insurance companies argue they need higher premiums to remain sustainable amid escalating disasters. Meanwhile, investigations show many are leveraging loopholes to avoid covering the customers who need them most — especially those living in fire-prone regions.

Regulators haven’t escaped criticism either. California insurance commissioner Ricardo Lara has faced accusations of prioritizing industry concerns over consumer protections, allowing steep price increases while offering minimal systemic reforms.

This imbalance sparked community backlash — including leaders like Joy Chen, whose public pressure helped accelerate stalled claims within days.

Climate Risk: The Growing Force Reshaping Homeownership

Global catastrophe losses are exploding. In 2025 alone, natural disasters caused over $145 billion in underwriting losses. Wildfires are only a portion of the total; storms and hurricanes contribute even more.

As private insurers pull back, government options like California’s Fair Plan are becoming the default — yet these programs are financially strained and unsustainable long-term.

“We’re marching toward an uninsurable future,” warns Dave Jones, former California insurance commissioner.

Experts say the industry must take bolder action: rewarding mitigation, rewriting replacement-cost formulas, and even leveraging their investment power to pressure fossil-fuel producers.

Why This Matters for Professionals Nationwide

Real estate agents, mortgage brokers, insurance agents, and financial planners are already feeling the tremors of this system shift.

Homebuyers can’t close deals without secured insurance.

Lenders face risk exposure when insurers drop coverage.

Agents must discuss climate risk disclosures more than ever.

Insurance professionals face tighter rules and scrutiny.

For those in Florida — where climate volatility and insurance instability are already present — the LA wildfire crisis is not a distant story. It is a preview.

Where Cameron Academy Fits Into This Moment

Cameron Academy continues to prepare rising and established professionals for real-world conditions, not just exam day. Whether you’re entering real estate, insurance, mortgage, finance, or expanding your licenses, understanding the impact of climate risk makes you more valuable — and indispensable to your clients.

Education isn’t just a requirement — it’s a professional advantage.

A Turning Point for the American Middle Class

Wildfire survivors like the Conkles aren’t asking for special treatment — just a fair return on the coverage they paid for. But their struggle reveals something deeper: the stability of American homeownership is being shaken by forces larger than any one family, insurer, or state.

Reform, price increases, and entirely new systems may emerge. But one truth remains: professionals across real estate and insurance will shape how Americans navigate the storms ahead.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida’s property insurance system is once again spiraling as new “market-friendly” reforms fail to stabilize rising premiums, insurer failures, and mounting homeowner frustration. Despite aggressive efforts to shift policyholders from Citizens to private carriers, many of the new insurers stepping in are tied to past insolvencies, questionable ratings, and political influence. For real estate, mortgage, and insurance professionals, these systemic cracks are reshaping closings, valuations, and risk across the state—making it essential to stay ahead of ongoing regulatory and market shifts.

Commercial real estate is heading into a turning‑point year in 2026, driven by economic uncertainty, AI‑powered transformation, shifting demographics and rising portfolio risk. Insights from The Counselors of Real Estate highlight the top issues shaping the year ahead—from fiscal pressures and capital constraints to housing shortages, global volatility and the future of data‑driven decision‑making. For real estate, mortgage, insurance and finance professionals, these trends offer a clear roadmap for staying competitive and preparing for the next wave of industry change.

AI-powered tools, fraud protection systems, and smarter MLS integrations are sweeping through the real estate industry as major organizations adopt new technologies. From RealReports hitting its 50th partnership to BeachesMLS unveiling instant AI home visualizations and Doorify boosting security, professionals are seeing rapid advancements that promise sharper insights, safer transactions, and more efficient rental workflows. This evolving tech landscape underscores the importance of staying educated and adaptable — especially for agents preparing for a competitive, AI-enhanced 2025 market.

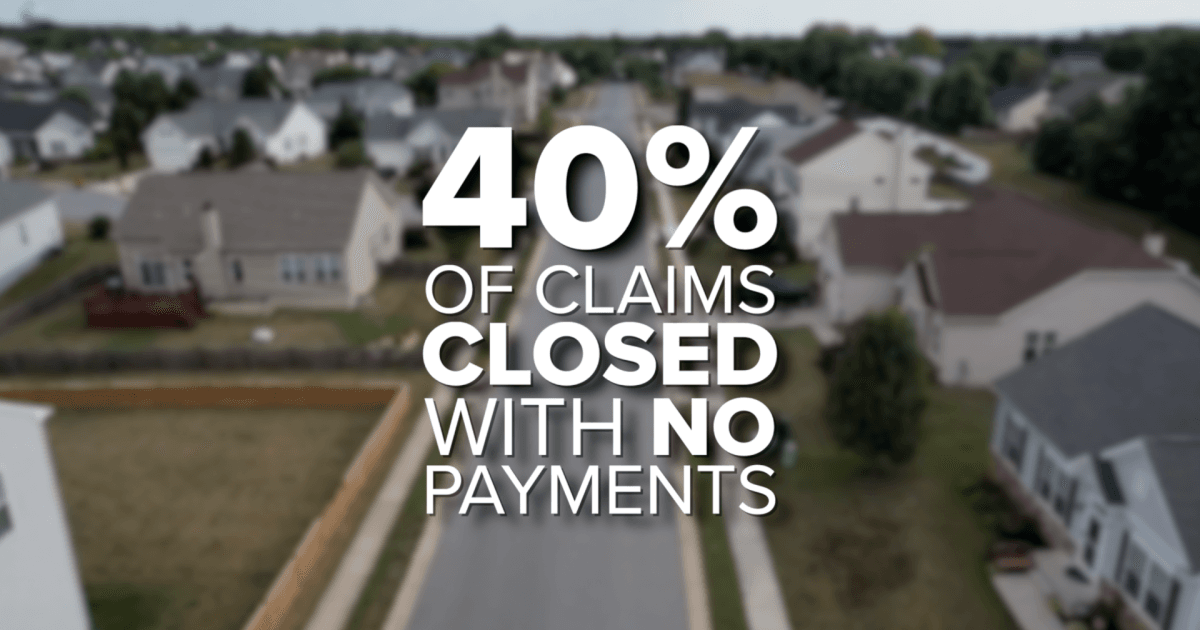

Florida homeowners are being hit with the highest insurance premiums in the nation, averaging $5,838 per year—nearly double the U.S. average. As costs skyrocket, many residents are reporting denied claims, non‑renewals, and impossible financial choices. New investigations reveal that more than 40 percent of claims in Florida close with no payment, while lawmakers push for transparency, fair pricing, and meaningful reform to stabilize a market that’s rapidly becoming unsustainable.

Vend Park, a Boston-based proptech company, has raised $17.5 million in Series A funding to reinvent parking as a high-performing commercial real estate asset. By replacing outdated operator–vendor systems with a unified AI-driven platform, Vend Park is helping major property owners boost NOI by up to 30%, slash operating costs, and modernize the tenant experience. As the company expands from three to fifteen cities and partners with giants like Nuveen and Jamestown, its technology highlights a major shift: real estate professionals must now understand AI, automation, and digital infrastructure to stay competitive.

Keller Williams Realty Atlanta Partners has formed an exclusive partnership with Southeast Mortgage, Georgia’s largest non‑bank mortgage lender. The collaboration promises faster, tech‑enhanced transactions for both agents and homebuyers, combining real estate expertise with streamlined mortgage services. This move reflects a growing trend toward integrated real‑estate ecosystems designed to reduce delays, boost transparency, and modernize the homebuying experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}