Illinois Updates Insurance Supplier Diversity Reporting Rules: What Professionals Need to Know for 2026

Illinois has officially refreshed its rules for insurance supplier diversity reporting — and the changes affect nearly every major insurance‑related organization doing business in the state.

On February 6, 2026, the Illinois Department of Insurance (IDOI) released Company Bulletin 2026‑03, replacing its 2024 guidance and outlining how companies must file their annual Supplier Diversity Reports beginning April 1, 2026.

Who Must File?

According to the IDOI, the requirement applies to every company authorized or accredited to do business in Illinois with at least $50 million in total net admitted assets. This includes:

Insurance companies

Health maintenance organizations (HMOs)

Limited health service organizations

Dental service plan corporations

Accredited reinsurers

Certain entities are exempt, such as fraternal benefit societies, domestic captive insurers, qualified group workers’ compensation pools, and Medicare‑only risk‑bearing entities.

Quick Snapshot: Are You Required to File?

Use this quick checklist:

Your organization has at least $50M in admitted assets

You operate or are accredited in Illinois

You are not exclusively a Medicare Part C or D organization

You are not a captive, fraternal, or exempt pool

If this describes you, the Supplier Diversity Report is required.

How Companies Must File Their Reports

The IDOI requires reporting entities to use the official state fillable PDF template located on the Insurance Supplier Diversity webpage. Reports must be submitted through SERFF and marked as publicly accessible under 215 ILCS 5/155.49(b).

For companies operating multiple lines of business, the IDOI allows a single filing — meaning companies writing both property & casualty and life or health business may submit one unified report.

Details Matter: Formatting Requirements for Questions 3–6

The bulletin highlights precise formatting expectations for procurement categories and reporting metrics. These include:

Comma‑separated certification types

Carriage‑return formatting for goals and results

Proper use of commodity codes or procurement identifiers

Relevant symbols (# / $ / %) depending on metric type

Companies within the same holding group may file individually or as a group — but cannot combine assets to meet filing thresholds.

Why This Update Matters

Supplier diversity continues to rise as a strategic and regulatory priority across insurance and financial sectors. Illinois’ refined guidelines reflect a push for increased transparency and more equitable contracting opportunities across the industry.

For professionals in insurance, compliance, procurement, and finance, understanding and correctly completing these requirements is essential. Inaccurate or incomplete filings can lead to regulatory delays and reputational risk.

Want to Read the Full Original Report?

The full story is available via Insurance Business Magazine.

How Cameron Academy Supports Insurance Professionals

As compliance requirements evolve — from licensing rules to reporting obligations — professionals need a reliable, modern, and flexible education partner.

At Cameron Academy, we empower insurance professionals across all 50 states with streamlined licensing courses, continuing education, and real‑time regulatory insights designed to keep you ahead of every update.

Whether you’re advancing your insurance career or expanding your credentials across states, the right education partner makes all the difference. Cameron Academy is here to help you move forward confidently.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

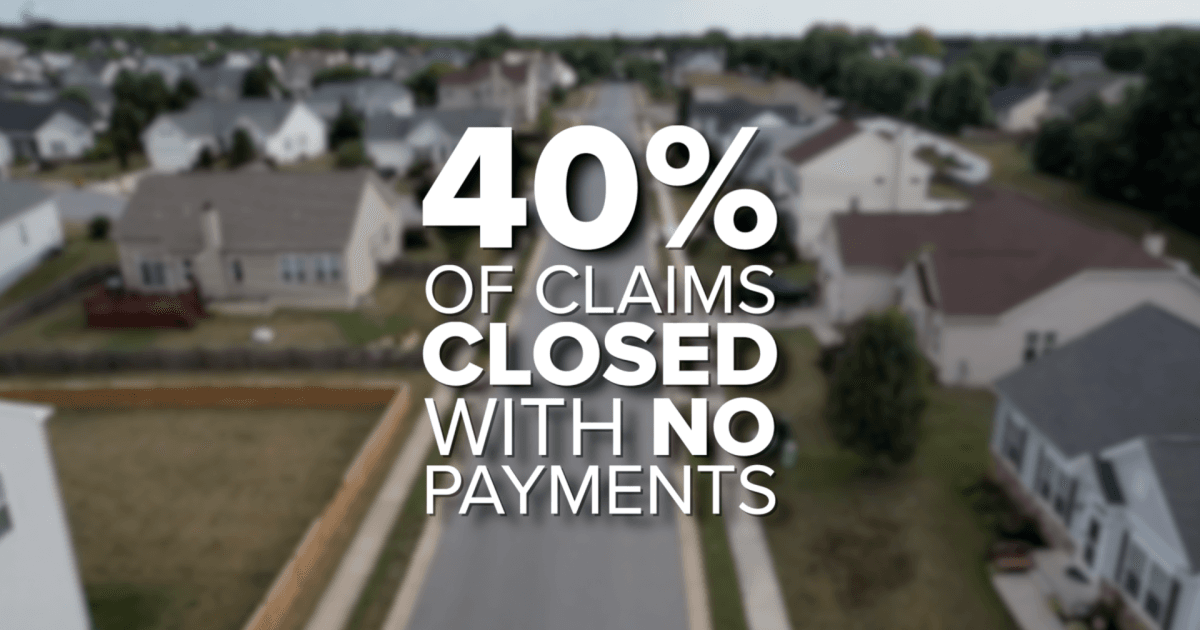

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}