In the heated arena of the U.S. presidential race, Vice President Kamala Harris has been making waves with her pointed critiques of former President Donald Trump’s business history. During a rally in Charlotte, North Carolina, on September 12, Harris unveiled her proposal for a $50,000 tax deduction aimed at small business startups. She then took a direct jab at Trump, asserting, “You know, not everybody started out with $400m on a silver platter and then filed for bankruptcy six times.”

Harris’s remarks have sparked a flurry of fact-checking, with many turning to a recent article from Al Jazeera that delves into the veracity of these claims. The article references a comprehensive 2018 analysis by The New York Times, revealing that Trump did indeed receive approximately $413 million from his father, Fred Trump, over his lifetime. However, this sum was not a single lump sum at the start of his career but rather dispersed over many years.

During a recent debate, Trump countered Harris’s claims, stating, “I wasn’t given $400m. I wish I was. My father was a Brooklyn builder. Brooklyn, Queens. And a great father, and I learned a lot from him. But I was given a fraction of that, a tiny fraction, and I built it into many, many billions of dollars.” The debate further intensified when Harris reiterated her points in a conversation hosted by Oprah Winfrey.

The Al Jazeera article also examines the claim of Trump’s six bankruptcies, confirming its accuracy. Trump’s financial struggles included high-profile bankruptcies such as the Trump Taj Mahal casino in 1991 and Trump Entertainment Resorts in 2009, among others. Experts have noted that while Trump did experience these financial setbacks, they are not uncommon in the business world.

Our Ruling

While Harris’s statement about Trump’s business beginnings contains elements of truth, it omits significant details. The New York Times investigation clarifies that Trump did not start his business career with $400 million readily available. Instead, he had the prospect of inheriting a portion of his father’s substantial real estate empire. This nuanced reality leads us to rate Harris’s statement as Half True.

Conclusion

As the presidential race progresses, the scrutiny of candidates’ claims remains crucial. Harris’s comments highlight the ongoing debate about wealth and privilege in America, while Trump’s rebuttal underscores the complexities of his business legacy. The full story, as always, is layered and multifaceted.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

The title insurance industry is entering 2026 with a renewed focus on technology, operational efficiency, and stronger agent support after years of volatility. Leaders from major underwriters report rising transaction activity, improved affordability, and a surge in automation and fraud‑prevention tools—signs that smarter systems and better training will define the next wave of growth.

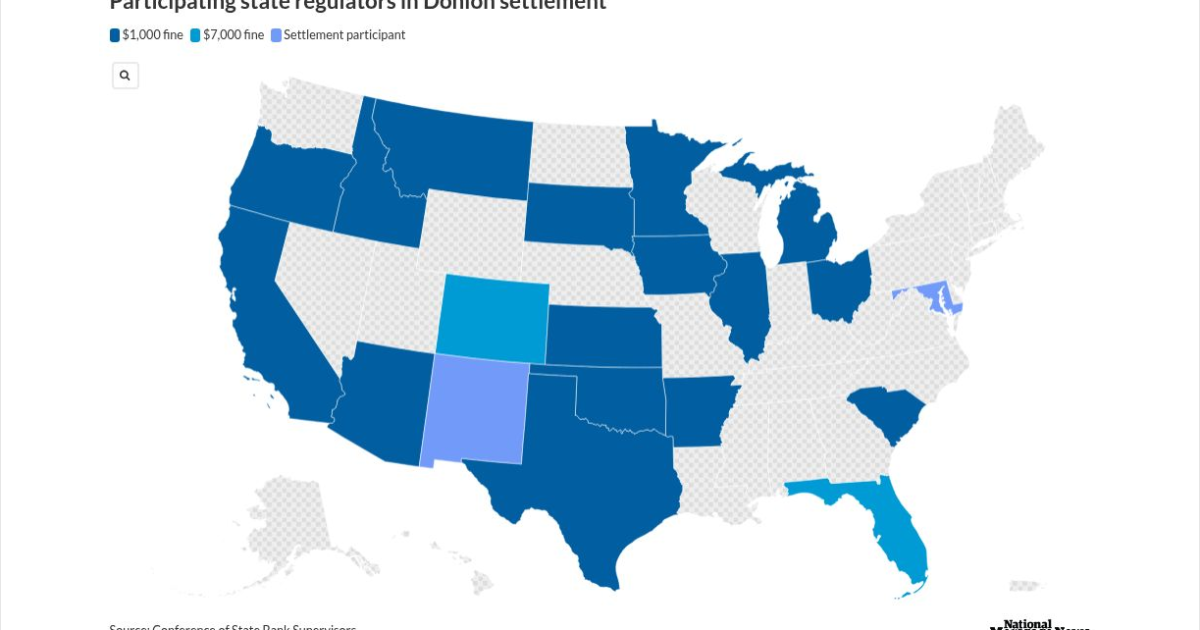

A multistate crackdown has sent shockwaves through the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, accepted a sweeping settlement that bans him from working as a mortgage loan originator in 21 states—19 of them permanently. Regulators say Donlon had another individual complete his mandatory licensing and continuing‑education courses, a violation that triggered a coordinated investigation and a $31,000 penalty. The case underscores regulators’ growing intolerance for education fraud and serves as a sharp reminder to industry professionals: cutting corners on licensing can end careers.

Florida’s once‑booming housing market is cooling fast as rising insurance premiums, increasing foreclosures, and expanding flood zones push buyers to back out of deals and force sellers to cut prices. With insurance now adding thousands to annual housing costs, professionals across real estate, mortgage, and insurance are navigating a dramatically shifting landscape that’s redefining affordability in the Sunshine State.

Florida begins 2026 with a wave of more than 250 new laws now in effect, impacting healthcare, insurance, real estate, and consumer protections statewide. From free breast cancer screenings for state employees to tighter pet insurance regulations, mandatory healthcare refund rules, enhanced animal‑cruelty penalties, and new condo‑management requirements, these updates carry major implications for professionals navigating Florida’s evolving regulatory landscape.

Florida’s barrier islands may offer postcard-perfect beaches and soaring real estate demand, but they’re also some of the most fragile and costly places to build in the United States. With 765,000 residents living on land that shifts, sinks, and takes the brunt of every major hurricane, the financial and insurance risks are accelerating fast. From billion‑dollar beach rebuilds to towers settling into the sand, today’s coastal development challenges are reshaping conversations around property values, disclosure, and long‑term resilience. For real estate professionals, understanding these risks isn’t just smart — it’s becoming essential.

A Cedar City development is turning heads with its fresh approach to affordability. The team behind Temple View Commons is delivering luxury‑inspired twin homes at prices below the local median by using a small, hands‑on staff and cutting traditional costs like realtor commissions. In a tight Utah housing market where inventory is scarce and prices remain high, their strategy offers a realistic path to homeownership without sacrificing high‑end finishes.

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}