Mortgage CEO Barred in 21 States After Education Fraud Settlement Shakes the Industry

A multistate enforcement action has shaken the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, agreed to a sweeping settlement that bans him from operating as a mortgage loan originator in 21 states—19 of them permanently. The Conference of State Bank Supervisors (CSBS) announced the agreement, which also includes a $31,000 penalty and strict conditions limiting Donlon’s involvement in financial services leadership roles for two years.

A Deep Dive Into the Allegations

According to settlement documents filed with the California Department of Financial Protection & Innovation, Donlon disputed the accusations but chose to resolve the matter to avoid the “time, expense, and uncertainty” of individual investigations across multiple states.

The allegations centered on a serious breach of the SAFE Act: Donlon was accused of having another person complete 22 pre‑licensing courses and three continuing education courses on his behalf—an unmistakable violation of federal and state licensing standards.

The CSBS and the American Association of Residential Mortgage Regulators coordinated the investigation after receiving a tip in early 2025, prompting a multistate response through the Nationwide Multistate Licensing System (NMLS).

Where the Ban Applies

The action involved 21 states, led by regulators in Arkansas, Colorado, Florida, Iowa, Kansas, and Texas. Other participating states include Arizona, California, Idaho, Illinois, Maryland, Michigan, Minnesota, Montana, New Mexico, Ohio, Oklahoma, Oregon, South Carolina, and South Dakota.

Donlon is permanently barred from the mortgage industry in 19 of those states. Only Colorado and Florida—where he may reapply in two years—left a pathway for reinstatement, contingent upon penalty payments and completing additional verified education.

Financial Penalties and Professional Fallout

Colorado and Florida will each receive $7,000 from the settlement, while the remaining participating states receive $1,000 each. Maryland and New Mexico—where applications were pending—are excluded from the financial distribution.

Beyond the bans, Donlon is prohibited from serving as a control person or qualified individual for any NMLS‑registered entity for two years. Trusted American Mortgage has already removed him from those internal roles.

“We require that licensed professionals complete their continuing education to ensure our licensees have the highest levels of competence and ethics,” said Susana Soriano, Acting Director of the Illinois Division of Banking. “With this action, the residential real estate market in Illinois has been protected.”

A Growing Trend of Education Fraud Crackdowns

This is not the first time CSBS has coordinated widespread actions targeting education fraud. In 2022, more than 440 loan officers settled claims with 44 state agencies for falsifying continuing education. Regulators have made it abundantly clear: education shortcuts will not be tolerated.

A Critical Reminder for Industry Professionals

For mortgage loan originators, this case reinforces the importance of legitimate education—both legally and ethically. Verified pre‑licensing and continuing education aren’t mere checkboxes; they are the cornerstone of safe, compliant lending practices.

At Cameron Academy, we understand how crucial it is for professionals to meet their education requirements truthfully and confidently. Our approved mortgage education programs are built to keep you compliant, protected, and prepared—without shortcuts or question marks.

For more details, view the original report at National Mortgage News:

Read the full article

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

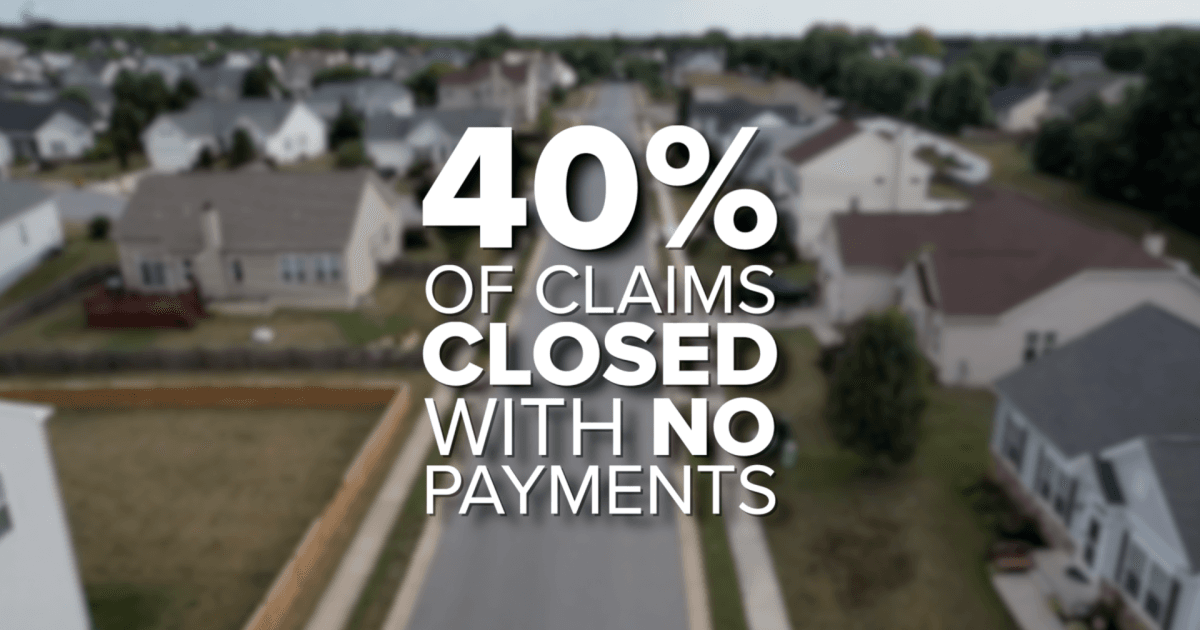

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}