Nevada’s Wildfire Insurance Shake-Up: A Bold Experiment With National Implications

Nevada has officially become the first state in the nation to allow insurers to sell homeowners’ policies that exclude wildfire coverage — a sweeping move that could reshape how disaster risk is priced across the West. The groundbreaking law, passed unanimously by both parties and signed by Governor Joe Lombardo, is designed to help contain rising insurance premiums in a climate‑challenged era.

But while some see a creative solution, others see a dangerous gamble.

The Nevada law, effective January 1, allows insurers to lower premiums by excluding wildfire damage — but consumer advocates warn this could leave homeowners financially devastated. Michele Steinberg of the National Fire Protection Association expressed shock that wildfire could be removed from standard coverage, fearing many homeowners may unknowingly opt into risky policies.

“It’s not a matter of losing your kitchen for a month,” Steinberg warned. “You’re homeless.”

The law also permits the sale of wildfire‑only policies and will remain in effect until the end of 2029. Industry groups supporting the measure argue it provides needed flexibility to keep insurers operating in high‑risk regions.

Why Nevada Is Different

Unlike states like California and Florida, Nevada is not currently facing an insurance crisis. In fact, it enjoys some of the lowest homeowners’ premiums in the country. A recent Consumer Federation of America report placed Nevada 46th nationally in average annual premiums.

Nor is Nevada heavily burdened by wildfire losses compared to its neighbors. FEMA data shows Nevada has received just $25 million in wildfire disaster aid since 1998 — a fraction of California’s $6.8 billion.

Yet wealthy, forest‑adjacent communities near Lake Tahoe, such as Incline Village, have experienced increasing insurance cancellations. Some residents even expressed willingness to waive wildfire coverage if it meant securing a policy. Lawmakers took notice.

The Mortgage Factor: A Hard Stop for Many

Despite the new law, many homeowners simply won’t be eligible for wildfire‑free policies. Mortgage giants Fannie Mae and Freddie Mac require fire coverage on insured homes. With nearly 60 percent of U.S. homes under mortgage, demand for these alternative policies may be limited.

Florida offers a comparable example: only about 4 percent of homeowners opt for wind‑excluded policies despite state approval.

A “Regulatory Sandbox” for Innovation

What truly excited some advocates wasn’t the wildfire exclusion itself but Nevada’s creation of an insurance regulatory sandbox. This framework lets insurers test innovative ideas — from on‑demand coverage to data‑driven auto premiums — while temporarily bypassing certain regulations.

Libertarian‑leaning think tanks have long promoted such sandboxes to accelerate innovation and reduce regulatory friction, and Nevada’s new law places it among roughly 15 states experimenting with this model.

Insurance analyst Sridhar Manyem described sandboxes as a way to “foster innovation and new products before you can make wholesale regulatory changes.”

Consumer Risks and Industry Hopes

Critics argue the new system sets a dangerous precedent. Insurance researcher Michael DeLong called it an “early prototype” of a troubling trend toward excluding natural disasters from standard policies.

Others believe this could be the blueprint insurers nationwide have been waiting for — particularly as wildfire threats grow alongside climate change.

But with no insurer yet announcing plans to sell wildfire‑excluded policies, Nevada’s bold move remains a test case, one the industry and regulators across the country are now watching closely.

What This Means for Real Estate & Insurance Professionals

For those in real estate, mortgage, or insurance — especially students or licensed professionals expanding their career — understanding shifts in risk, policy structure, and regulatory direction is more important than ever. This Nevada experiment could spark copycat policies across Western states, influencing underwriting, property valuations, and financing options.

At Cameron Academy, we prepare professionals to navigate exactly these kinds of evolving landscapes across real estate, mortgage, finance, and insurance industries. Staying ahead of regulatory trends isn’t just smart — it’s essential.

As Nevada’s wildfire experiment unfolds, it may redefine how risk is priced in high‑fire‑danger areas and reshape the future of property insurance nationwide.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

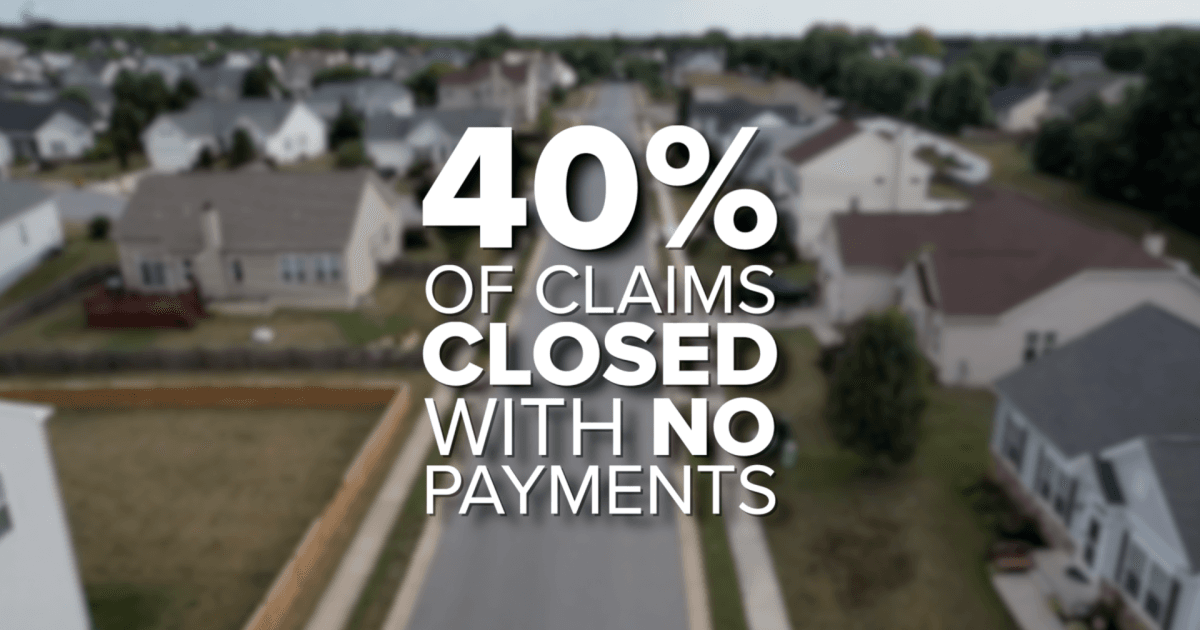

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}