Examining the Impact of Proposition 47 and the Pandemic on Crime in California

In a detailed analysis by the Public Policy Institute of California, authors Magnus Lofstrom and Brandon Martin explore the ramifications of Proposition 47 alongside the COVID-19 pandemic on crime rates in the Golden State. Proposition 47, enacted in November 2014, was a landmark reform that reclassified certain non-violent drug and property offenses from felonies to misdemeanors. This legislative shift led to a significant reduction in the state’s prison population, saving approximately $800 million, which was redirected to fund treatment and diversion programs.

The report highlights a notable increase in property crimes, particularly larcenies and burglaries, following the implementation of Proposition 47. These trends were exacerbated during the pandemic, where reduced clearance rates for these crimes were identified as a key factor. Despite the decrease in incarceration rates, the increase in crime was described as modest, with the authors emphasizing the limited impact of changes in drug arrests on overall crime rates.

The Pandemic’s Influence on Crime

The pandemic further altered the crime landscape, with lower enforcement and incarceration rates contributing to a rise in property crimes, especially commercial burglaries and auto thefts. Nonetheless, the report found no significant evidence linking drug arrests to an increase in crime during this period.

The authors recommend that California’s policymakers focus on reversing the declining clearance rates and prioritize evidence-based alternatives to incarceration. While acknowledging the successes of Proposition 47 in reducing inmate populations, the report underscores the importance of understanding the factors influencing crime rates and implementing strategies that emphasize increased apprehension rates over harsher punishments.

Recommendations for Policymakers

As California reflects on a decade of criminal justice reforms, the insights from this report are crucial. Policymakers are encouraged to delve deeper into the underlying causes of crime increases and to explore innovative solutions that balance public safety with justice reform. This includes enhancing the effectiveness of law enforcement through better resources and training, and investing in community-based programs that address the root causes of crime.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

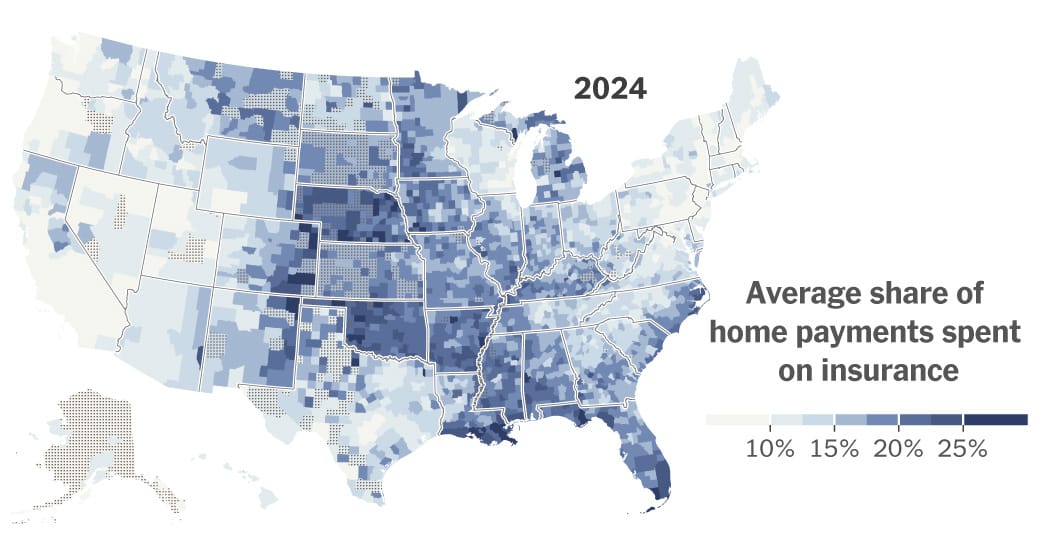

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

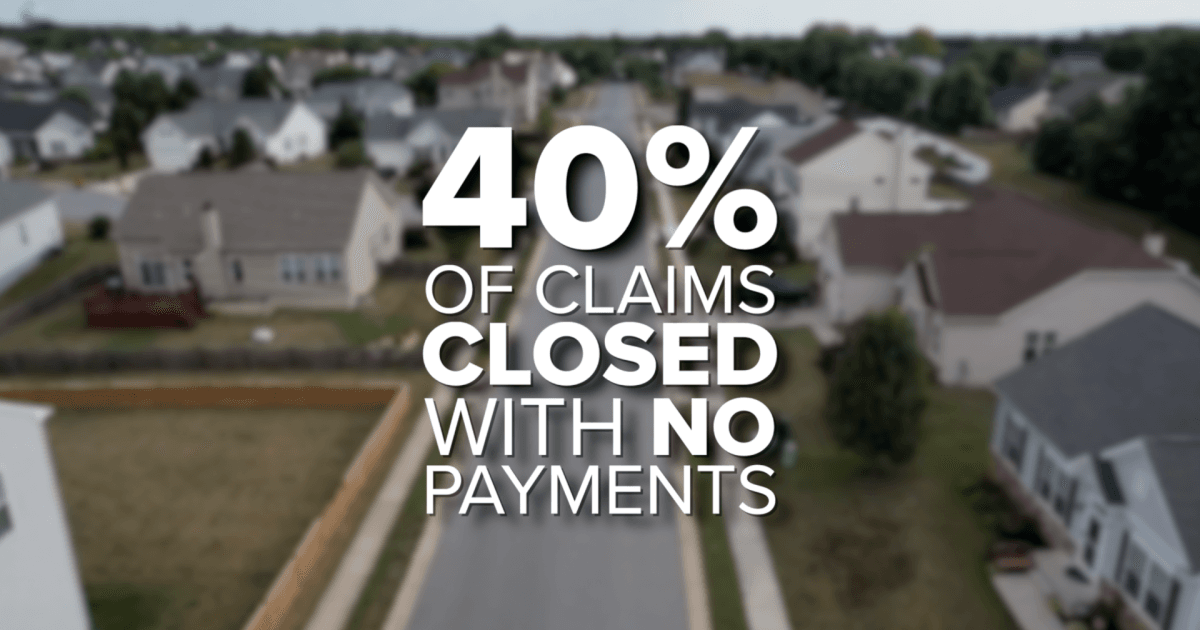

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}