Real Estate Commission Changes: A New Era for Homebuyers and Sellers

The real estate landscape is undergoing a significant transformation following a landmark lawsuit settlement by the National Association of Realtors (NAR) in March 2024. The new regulations, which took effect on August 17, 2024, have stirred a mix of reactions across the industry. While some predict a competitive price war that could drive down commissions, others worry that the changes might deter buyers from using agents altogether due to increased costs.

What Changed?

Under the new rules, listing agents can no longer make offers of compensation to buy-side agents on any NAR-affiliated multiple listing service (MLS). Additionally, a buyer’s agent must now have a written contract with a home shopper, clearly specifying their fee, before showing them any property. This shift aims to bring greater transparency to the process, ensuring homebuyers are fully aware of how much they’re paying for an agent’s services.

Impact on Commissions

Despite the anticipated upheaval, the effects have been relatively muted as of early 2025. According to Redfin reports, the average buyer’s agent commission has barely changed, hovering around 2.37 percent in the fourth quarter of 2024. This slight adjustment reflects a modest decrease from 2.45 percent a year earlier.

Good or Bad for Consumers?

The new regulations have sparked debate over their impact on consumers. Some industry experts foresee a “buy-side price war” that could benefit homebuyers, allowing them to shop around for agents similarly to how they compare mortgage lenders. However, others caution that the added complexity may prolong the homebuying process as buyers, sellers, and agents negotiate fees and responsibilities.

Challenges for First-Time Buyers

First-time homebuyers, already burdened by high prices and mortgage rates, may face additional challenges under the new structure. Without the option to roll commission costs into their mortgages, many may struggle to afford professional representation. The industry is urging the Federal Housing Finance Agency to allow these costs to be included in mortgage financing to alleviate the financial strain on new buyers.

Options for Sellers

For sellers looking to save on commissions, alternative options are available. They can opt for a for sale by owner transaction, negotiate commission rates with agents, hire a low-commission real estate agent, or sell to a cash-homebuying company.

In conclusion, while the real estate commission changes are designed to enhance transparency and competition, their long-term effects on the market remain to be seen. As the industry adjusts to these new dynamics, both homebuyers and sellers must navigate the evolving landscape with careful consideration of their options and potential costs.

For a more in-depth analysis, refer to the original article on Bankrate.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

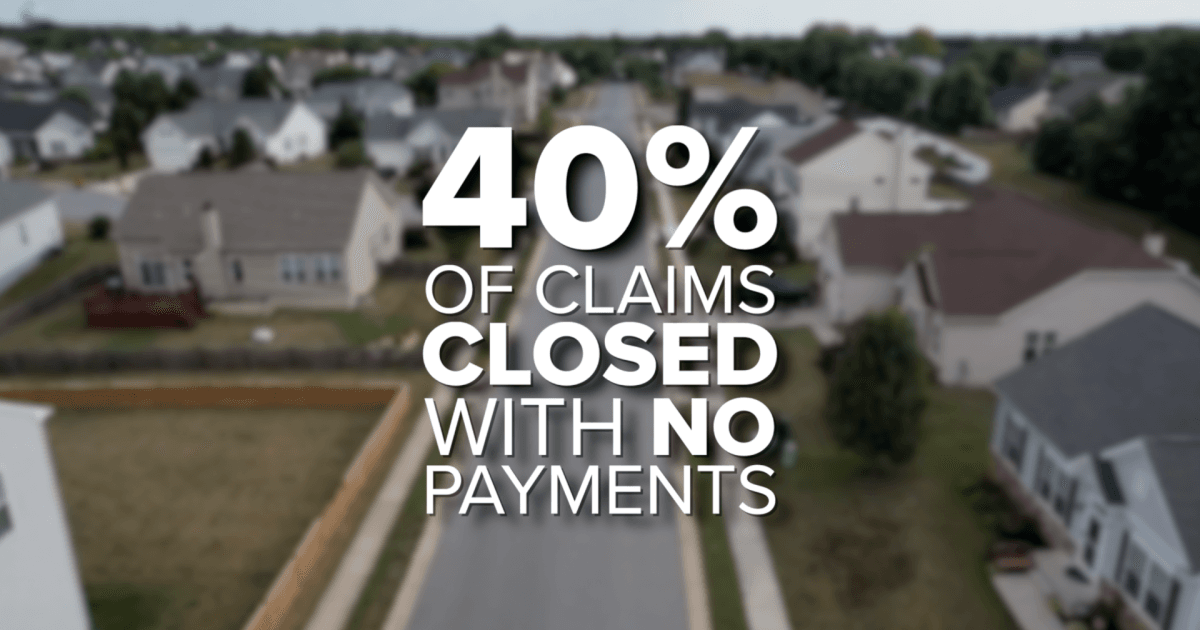

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

What Changed?

What Changed?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}