Rising Home Insurance Costs Are Quietly Reshaping America’s Real Estate Market

Across the United States, a new force is beginning to reshape local real estate markets — and it isn’t mortgage rates, inflation, or even inventory shortages. It’s home insurance. In the most disaster‑prone areas, skyrocketing premiums are eating directly into home values, upending long‑held assumptions about affordability, risk, and long‑term investment viability.

The New York Times recently published a deeply reported investigation into this rapidly expanding crisis, revealing how rising premiums — often fueled by global reinsurance upheavals — are placing thousands of homeowners under intense financial pressure. Their reporting, grounded in national data and real‑world interviews, highlights an emerging trend that real estate professionals must watch closely.

When Insurance Becomes the Dealbreaker

In coastal Louisiana, residents are facing insurance increases that would have seemed unimaginable just a few years ago. Sandra Rojas, a fifth‑generation resident of Lafitte, saw her annual premium soar to $8,312 — more than double what she paid four years earlier. She considered selling, but with home values in her region down 38% since 2020, her options are limited. “You’re kind of stuck where you are,” she said.

Similar stories are emerging nationwide. In Colorado, buyers are walking away from deals after failing to secure affordable wildfire coverage. In California, 13% of real estate agents report transactions falling apart because buyers couldn’t obtain insurance at all.

New research from the National Bureau of Economic Research provides numbers to match the stories. Disaster‑exposed ZIP codes are seeing home values fall in direct response to rising insurance costs. According to researchers Benjamin Keys and Philip Mulder, homes in the top 10% most exposed areas are selling for an average of $43,900 less than they would have otherwise.

Their study of 74 million payment records from 2014–2024 found that nearly one‑fifth of the national increase in premiums since 2017 is tied to “rapid repricing” of climate‑driven risks. Meanwhile, global reinsurers — absorbing mounting losses — have doubled the rates they charge insurers, who then pass the burden directly to homeowners.

A Growing National Ripple Effect

In hail‑risk Midwest states, insurance now consumes more than 20% of total housing payments. In parts of Louisiana, it exceeds 30%. For buyers, this means steeper monthly costs. For sellers, it means fewer qualified buyers and declining property values.

Some homeowners are even dropping coverage entirely. In Lafitte, Clarence Guidry received a quote for a $20,000 premium — plus a $50,000 hurricane deductible. Unable to sustain the cost, he paid off his mortgage and now self‑insures. He’s not alone: 13% of U.S. homeowners are now uninsured.

What This Means for Real Estate and Professional Licensees

Insurance‑driven pricing pressures are no longer hypothetical — they are here, reshaping how agents, lenders, appraisers, and insurance professionals work. Deals stall, lenders tighten, buyers hesitate, and municipalities face shrinking tax revenue as home values cool.

For professionals, especially those working in high‑risk states like Florida, staying current on these shifts is essential. Cameron Academy offers real‑estate and insurance licensing education designed to help professionals understand not only the rules of their industry but also the evolving economic forces that shape it. Understanding how climate‑risk and insurance impacts property value is now a core professional skill.

Looking Forward

As reinsurers adjust their risk models and climate‑driven disasters grow more severe, insurance premiums are projected to keep rising. Industry analysts expect home values in high‑risk markets to adjust further downward as buyers push for affordability.

For many Americans, the dilemma is becoming painfully clear: pay soaring premiums, sell at a loss, or self‑insure and hope for the best.

Real estate, insurance, lending, and financial professionals will need to stay educated and adaptable — and up‑to‑date training is one of the most powerful tools available.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida families are feeling the squeeze as everyday costs, insurance premiums, and homeownership barriers continue to climb. House District 102 candidate Jayden D’Onofrio is calling for a broader, more unified affordability strategy—one that tackles the state’s insurance crisis, supports first‑time homebuyers, and restores real competition in the market. His message centers on transparency, practical solutions, and keeping Florida livable for the professionals, workers, and families who power its economy.

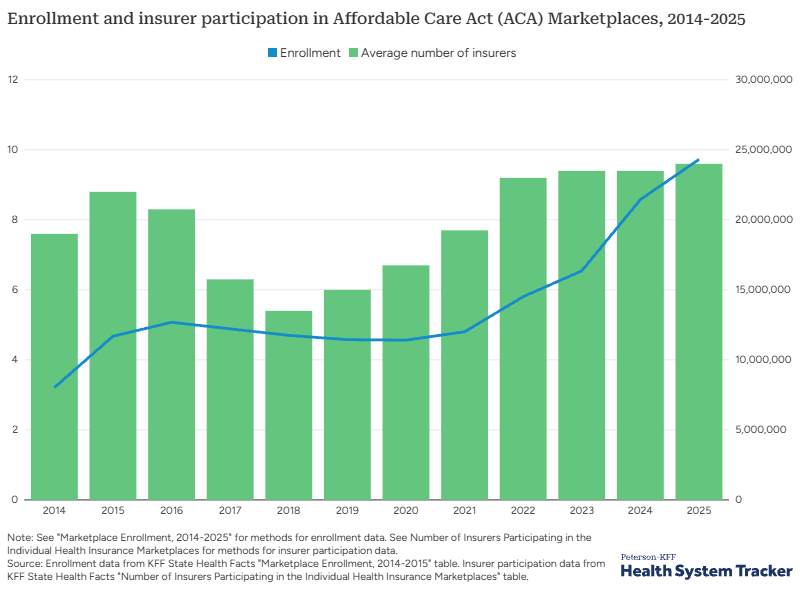

A decade of dramatic change is reshaping America’s health insurance markets. Employer group plans are becoming increasingly dominated by a few powerful insurers, while the ACA individual marketplace is experiencing record‑breaking competition and enrollment. Self‑funded plans are surging, small‑group premiums are driving employers to new coverage models, and major policy shifts in 2025 could redefine affordability for millions. This data‑driven Peterson‑KFF analysis breaks down the trends every insurance, finance, and business professional needs to understand as the industry enters a transformative new era.

Sarasota County is inching closer to approving Winchester Ranch, a massive 8,999‑home community planned for more than 3,100 acres in North Port. With a 7‑1 vote from the Planning Commission and a final decision expected in early 2026, the project could become one of Southwest Florida’s largest developments in decades—bringing new housing, commercial space, and industry while raising fresh questions about growth, the environment, and the region’s rapidly evolving real estate market.

Lument Finance Trust has closed a major $663.8 million commercial real estate CLO, marking one of the standout CRE finance deals of 2025. The transaction, LMNT 2025-FL3, features a strong reinvestment period, non‑recourse and non‑mark‑to‑market financing, and a diversified pool of 32 loans tied to 49 properties nationwide. With J.P. Morgan leading the structuring and more than $585 million placed in investment‑grade securities, the deal highlights renewed stability in transitional CRE debt—making it a development real estate and finance professionals will want to watch closely.

Walmart has partnered with Alquist 3D to roll out the nation’s first large‑scale wave of 3D‑printed commercial buildings, signaling a major shift in how future retail and industrial spaces will be constructed. After completing an 8,000‑square‑foot 3D‑printed expansion in Tennessee—the largest of its kind—the company is moving forward with over a dozen new projects nationwide, accelerating a tech‑driven transformation in commercial real estate.

Citizens Property Insurance Corp. is recommending statewide rate reductions for 2026—the first proposed decrease in more than a decade. Most Citizens policyholders could see an average 11.5% drop, reflecting recent insurance‑market reforms that have stabilized Florida’s turbulent property sector. With hundreds of thousands of policies moving back to private insurers and state‑backed Citizens shrinking to record‑low enrollment, real estate and insurance professionals should prepare for how lower premiums may influence affordability, buyer confidence, and market activity heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}