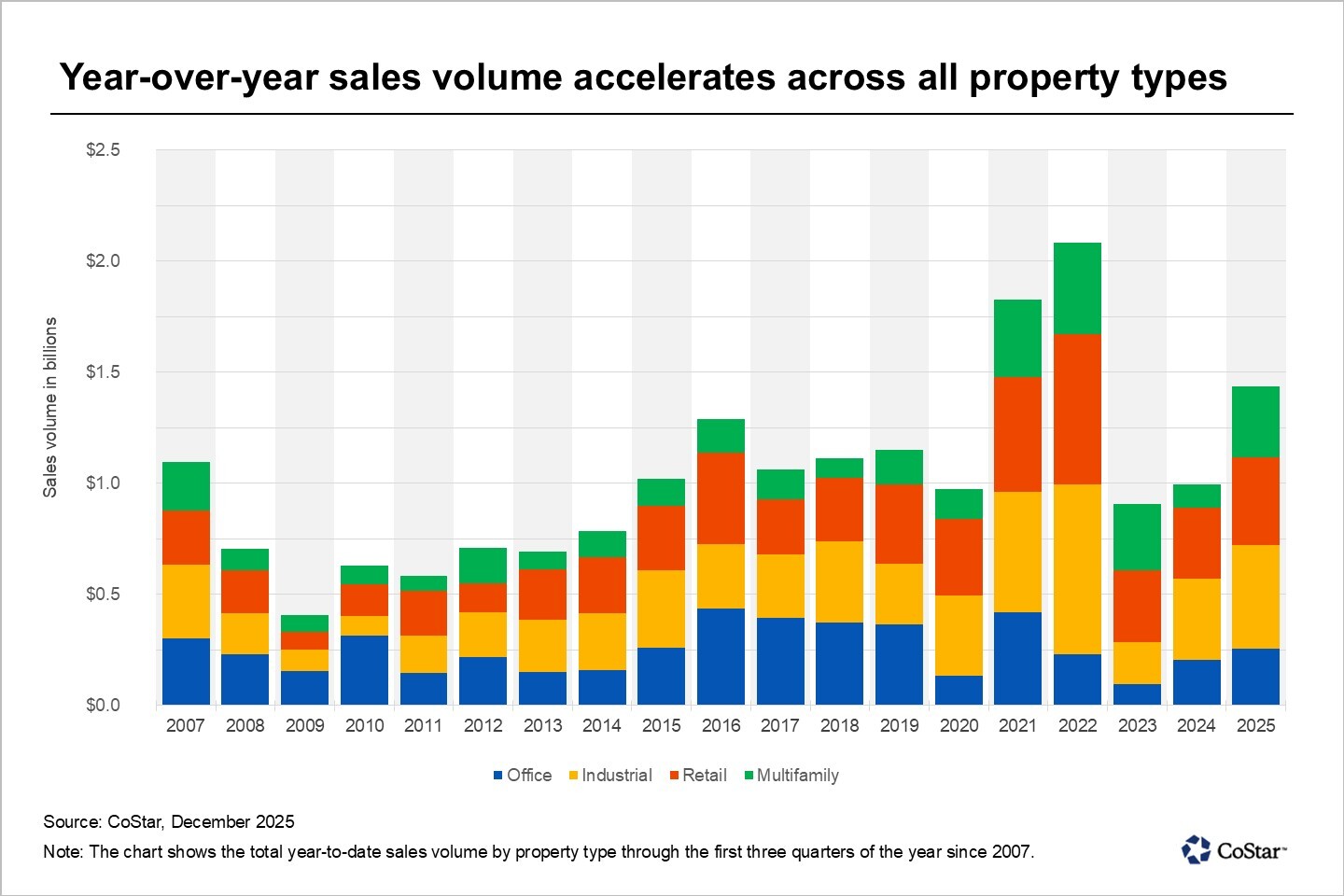

Across southwest Florida, the middle class is experiencing a financial squeeze unlike anything in recent memory. Surging insurance premiums, soaring construction costs, and the long shadow of Hurricane Ian have created a perfect storm — one that threatens the very communities that once made Florida’s Gulf Coast feel like paradise.

A recent NPR investigation illustrates the growing strain: families leaving homes they’ve lived in for decades, small hotels disappearing, and Realtors warning of a looming rise in foreclosures.

Three Years After Ian, Recovery Is Still Out of Reach

In Fort Myers Beach, the constant hum of construction is a reminder of what was destroyed and what is slowly being rebuilt. The charming cottages and locally owned hotels that once defined the shoreline are vanishing, replaced by elevated, high‑cost structures built for modern code requirements.

“Only well‑heeled players can play now,” says builder Rob Fowler, describing the wave of gentrification reshaping the island.

Many of the new buildings are simply out of reach for the workers and families who once formed the backbone of the community — the bartenders, clerks, hotel staff, and multi‑generation locals.

Insurance: The Silent Force Behind the Crisis

Florida’s insurance premiums are now among the highest in the nation. According to Bankrate, the average homeowner pays over $5,700 per year — more than double the national average. Flood insurance costs have also surged due to FEMA’s updated risk‑based pricing system.

“Insurance has gone through the roof,” says Karen Rodriguez of Habitat for Humanity. “It has impacted every single person here.”

Some families pay more than $10,000 annually just to stay insured — a breaking point for many.

Realtors Brace for Trouble

Local agents are reporting growing anxiety as repair costs and insurance prices soar. Many homeowners are stuck in limbo — unable to afford staying, yet unable to sell unless they invest in costly mitigation upgrades like flood gates.

In Lee County, homes are sitting on the market longer, and values have dropped more than 10% year‑over‑year. Zillow reports that prices are now substantially below their pre‑Ian levels.

“If this economy continues for another year, we’re going to see a lot of foreclosures,” warns Realtor Jessica Gatewood.

Renters Aren’t Safe Either

As landlords pass down their own insurance increases, rents in parts of Lee County have doubled. Families who once moved to Florida for affordability are now leaving for states like Ohio and North Carolina.

The Florida Chamber of Commerce confirms the trend: more than half a million people left the state in 2023, citing rising housing costs as a primary factor.

A Community Rebuilt — But For Whom?

Despite the struggles, construction continues. New resorts open, rebuilt restaurants welcome guests, and sunsets still draw crowds. Local leaders remain hopeful that investment will eventually stabilize the region — assuming another major storm doesn’t set recovery back again.

“People will come here, and they will build, and they will stay,” says Chamber CEO Jacki Liszak. “But we’re racing the next hurricane.”

What This Means for Real Estate Professionals

For both aspiring and established real estate professionals, Florida’s shifting market offers challenges — but also tremendous opportunity. Understanding insurance trends, climate‑resilient construction, and changing buyer psychology is becoming essential.

Educational providers like Cameron Academy play a key role in preparing professionals for these evolving conditions, offering up‑to‑date courses on regulations, market dynamics, and Florida’s uniquely challenging real estate environment.

A State at a Crossroads

The question isn’t just how Florida will rebuild — but who will still be able to call it home. Middle‑class families are being priced out, long‑standing communities are shifting, and hurricane season is always just around the corner.

What remains is a coastline filled with beauty, opportunity, risk, and rapid transformation — a story still unfolding with every passing storm.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}