Self‑Storage Sales Surge 62% as Investors Target High‑Barrier Markets

Investor confidence roared back into the U.S. self‑storage sector in the third quarter of 2025, pushing transaction volume to nearly $1.6 billion — a powerful 62% jump compared to the same period last year. With 266 facilities changing hands between July and September, the industry is experiencing its sharpest resurgence since early‑cycle expansion years.

The full analysis, originally reported by Scotsman Guide and supported by StorageCafe, shows a sector where both private buyers and institutional giants moved aggressively — though with interesting differences in strategy.

REITs Pay a Premium as Portfolios Consolidate

Non‑REIT buyers dominated transaction count, yet real estate investment trusts still played a very strategic role — involved in roughly a quarter of all deals. REITs specifically targeted high‑barrier, high‑performance markets and paid an average of $146 per square foot, outpacing the $133 paid by non‑REIT buyers.

Total traded space jumped from 12.8 million sq. ft. in Q3 2024 to 18.4 million sq. ft. this year, underscoring that strong self‑storage inventory remains one of the most resilient commercial real estate categories.

Sun Belt Still Dominates — But Investors Are Spreading Out

The Sun Belt continued to rank as the country’s top‑performing region, capturing 53% of all transactions. But this reflects a drop from nearly 70% the previous quarter — a sign that investors are cautiously exploring fresh markets outside the region.

Florida, California, and Georgia each surpassed $200 million in total transaction value. Meanwhile, Texas saw the highest number of sales but collectively failed to break $50 million due to smaller deal sizes — a fascinating contrast in volume versus value.

New York City Takes the Crown

New York City led all metros, closing $90 million in transactions. Dense, land‑restricted Manhattan drove per‑square‑foot pricing to a national high of $526. A big contributor: Storage Post’s acquisition of three Manhattan assets, including a $60 million purchase on Amsterdam Avenue.

Las Vegas followed with $76.3 million in trades, averaging $200 per square foot, with Etude Capital notably active. Atlanta secured the No. 3 spot with nearly $43 million in volume — boosted by its low storage availability per capita.

Even California’s coastline, often considered too high‑barrier for new self‑storage plays, saw reinvigorated activity such as Etude Capital’s $26 million Temecula acquisition.

What This Means for Real Estate Professionals

For residential and commercial real estate professionals, this quarter reinforces a clear takeaway: specialty asset classes like self‑storage continue to offer stable, opportunity‑rich ground, even when other sectors soften.

Whether you’re exploring commercial specialization or simply expanding your knowledge base, staying credentialed and competitive is essential. This is where institutions like Cameron Academy shine — helping new and seasoned professionals upgrade their licenses, advance their expertise, and unlock new income streams in a market evolving toward 2026.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A growing share of American homeowners now carry mortgage rates above 5%—a dramatic shift that’s reshaping refinancing, inventory, and buyer behavior nationwide. With more than 30% of borrowers locked into rates over 5% and 20% above 6%, the market is split between owners holding on to low pandemic‑era loans and new buyers taking on higher‑rate mortgages. Federal efforts to push rates down could unlock millions of refinancing opportunities, while buyers see only modest monthly savings. For real estate professionals, understanding these rate dynamics is crucial as they increasingly drive inventory levels, affordability, and market activity.

New Moody’s data shows commercial real estate deal volume slipped 20% in December, marking a second monthly decline. Yet the full year tells a different story: 2025 ended with a 17% gain, signaling a quiet but resilient recovery. The biggest surprise came from the office sector, which posted a 21% jump in activity as return‑to‑office trends and AI‑driven job growth boosted demand. Multifamily, retail, and alternative assets like data centers also saw strong momentum, giving real estate professionals a market full of fresh opportunities heading into 2026.

Florida drivers and industry professionals are heading into 2026 with good news: auto insurance rates are dropping across the state as the market shows strong signs of stabilization. USAA leads the latest wave with a 7% average rate decrease expected in May 2026, saving members more than $125 million annually. They join several major insurers — including State Farm, Progressive, AAA, Allstate, and Florida Farm Bureau — all approving significant reductions. Officials credit recent legislative reforms, especially tort reform, for the improved loss ratios and renewed insurer confidence. With both auto and home insurance markets strengthening, Florida’s real estate, mortgage, and insurance professionals can expect more consumer confidence, smoother transactions, and expanding career opportunities.

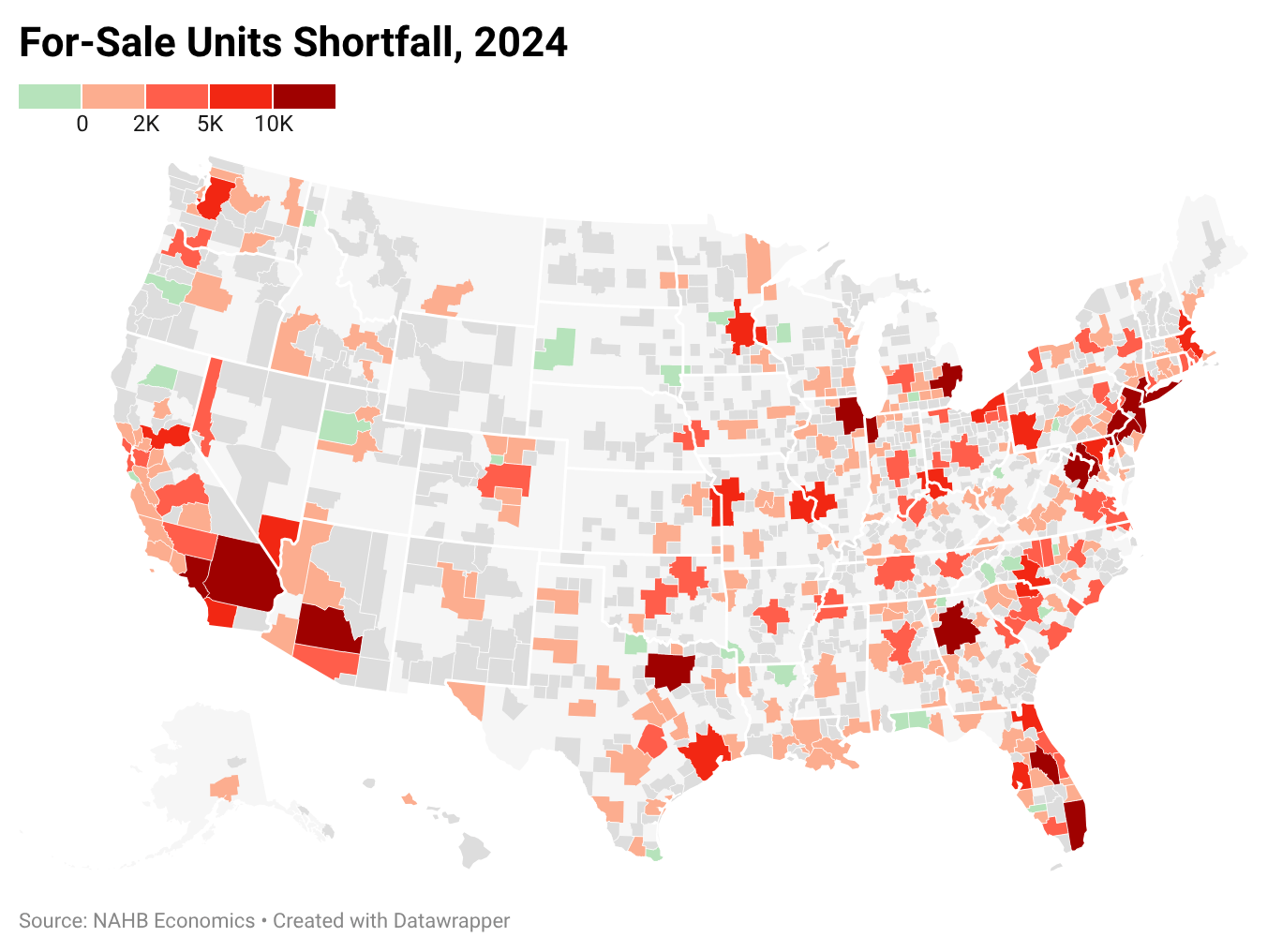

New data from Eye On Housing and the NAHB shows the U.S. remains short more than 1.2 million housing units, keeping pressure on both rents and home prices. Record‑low vacancy rates, slow single‑family construction, and restrictive zoning continue to fuel intense competition in 2024. Major metros like Chicago, New York, and Atlanta face some of the deepest deficits, and the true nationwide shortfall may be even higher when accounting for overcrowding and aging homes. For real estate professionals, the ongoing shortage means sustained demand, tighter inventory, and major opportunities for those who understand the evolving market.

Top real estate coach Jason Pantana says the divide between agents today isn’t about who has “tried” AI — it’s about who is immersed in it. In a new HousingWire interview, he explains why AI isn’t a gimmick but a full business system that amplifies output, improves authenticity, and reshapes how clients search for agents. From prompt mastery to AI‑driven visibility on Google, Pantana reveals how agents who commit even 15 minutes a day to learning AI are already outperforming those who hesitate.

Dallas–Fort Worth’s commercial real estate market closed 2025 with a split personality. Industrial dominated with massive new deliveries and soaring leasing demand, retail held steady with some of the market’s strongest fundamentals in years, and office continued to falter under remote‑work pressures. High vacancies, weak absorption, and rising demand for top‑tier space show the sector’s ongoing reset. Meanwhile, industrial and retail strength position the Metroplex for another powerhouse year heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}