Starting Your Career? The Best and Worst States to Launch Your Professional Journey

Where you choose to begin your career can influence your earning potential, job stability, and long-term financial growth. A new analysis highlighted by Investopedia reveals which states offer the strongest footing for entry-level professionals and which ones create steep challenges right out of the gate.

TopResume evaluated thousands of entry-level job postings across the United States, measuring job availability, competition, local salaries, and living costs. For newcomers trying to build savings, secure housing, and establish themselves professionally, these factors matter more than ever.

The Best States for Starting a Career

Wyoming stands out as the top state for launching a new career, offering 129 entry-level jobs per 100,000 people, low competition, and an adjusted median salary of $52,163. With median home prices near $356,688 and rent averaging about $1,300 per month, young professionals get a strong balance of opportunity and affordability.

Vermont also performs well, with 118 entry-level jobs per 100,000 people and low competition. Although the median salary is under $42,000, Vermont remains attractive for those seeking a quieter environment. Housing costs are higher, with median home prices over $382,000 and average rent around $2,075.

North Dakota offers roughly 92 entry-level positions per 100,000 residents, alongside median home prices of about $277,556 and rent near $1,100. These lower housing costs help entry-level workers get ahead faster.

Alaska provides about 88 entry-level jobs per 100,000 people. Its lower median salary, just under $42,500, can make housing a challenge, but average rents around $1,800 and median home prices under $376,000 still create room for financial freedom with careful planning.

South Dakota rounds out the top group with approximately 80 entry-level roles per 100,000 residents. With a median home price near $310,000 and average rent around $1,200, it is a strong option for newcomers seeking stability and manageable living costs.

The Most Challenging States for New Professionals

California ranks last for entry-level job opportunity, offering only 1.84 positions per 100,000 people. With an adjusted median salary of $36,982, median home prices above $750,000, and average rent at $2,750, financial progress is extremely difficult for newcomers.

Hawaii pairs a very small job market with high living costs. Adjusted median salaries sit near $24,500, while median home prices exceed $819,000 and rent averages $3,000. For entry-level professionals, financial mobility is limited.

Massachusetts also presents challenges, with limited entry-level openings and an adjusted median salary of $38,492. Housing is costly, with median home prices around $640,000 and rent near $2,930, which can restrict early financial growth.

Related States Worth Noting

New York is highly competitive, offering about three entry-level jobs per 100,000 people. Even for those who secure a position, median home prices near $502,000 and average rent at $3,500 can deter relocation.

Florida offers similar job competition, with only around three entry-level roles per 100,000 people. Housing is more approachable, though, with median home prices around $372,000 and average rents near $2,325. For newcomers pursuing real estate, mortgage, insurance, or finance careers, Florida continues to be a strong long-term market. If you are aiming to enter these fields, Cameron Academy provides industry-focused licensing programs to help you build a competitive edge no matter where you start.

To explore the full analysis behind these rankings, visit Investopedia for the original report. And if you are launching a career in real estate or another licensed profession, Cameron Academy can help you move forward with confidence and industry-ready education.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida’s property insurance system is once again spiraling as new “market-friendly” reforms fail to stabilize rising premiums, insurer failures, and mounting homeowner frustration. Despite aggressive efforts to shift policyholders from Citizens to private carriers, many of the new insurers stepping in are tied to past insolvencies, questionable ratings, and political influence. For real estate, mortgage, and insurance professionals, these systemic cracks are reshaping closings, valuations, and risk across the state—making it essential to stay ahead of ongoing regulatory and market shifts.

Commercial real estate is heading into a turning‑point year in 2026, driven by economic uncertainty, AI‑powered transformation, shifting demographics and rising portfolio risk. Insights from The Counselors of Real Estate highlight the top issues shaping the year ahead—from fiscal pressures and capital constraints to housing shortages, global volatility and the future of data‑driven decision‑making. For real estate, mortgage, insurance and finance professionals, these trends offer a clear roadmap for staying competitive and preparing for the next wave of industry change.

AI-powered tools, fraud protection systems, and smarter MLS integrations are sweeping through the real estate industry as major organizations adopt new technologies. From RealReports hitting its 50th partnership to BeachesMLS unveiling instant AI home visualizations and Doorify boosting security, professionals are seeing rapid advancements that promise sharper insights, safer transactions, and more efficient rental workflows. This evolving tech landscape underscores the importance of staying educated and adaptable — especially for agents preparing for a competitive, AI-enhanced 2025 market.

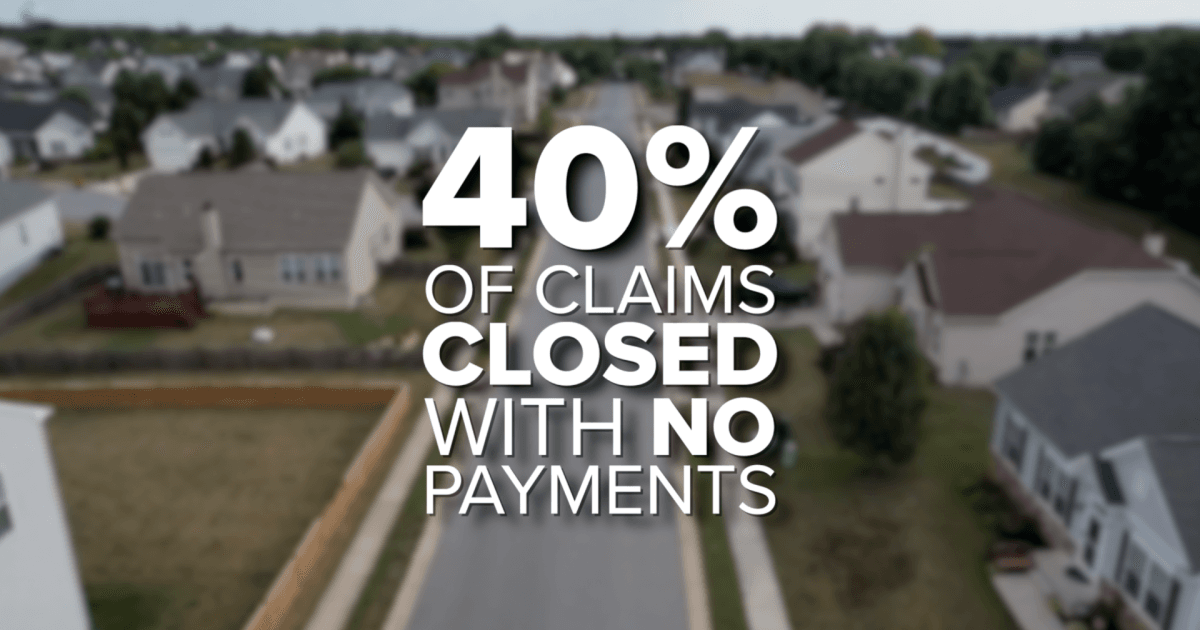

Florida homeowners are being hit with the highest insurance premiums in the nation, averaging $5,838 per year—nearly double the U.S. average. As costs skyrocket, many residents are reporting denied claims, non‑renewals, and impossible financial choices. New investigations reveal that more than 40 percent of claims in Florida close with no payment, while lawmakers push for transparency, fair pricing, and meaningful reform to stabilize a market that’s rapidly becoming unsustainable.

Vend Park, a Boston-based proptech company, has raised $17.5 million in Series A funding to reinvent parking as a high-performing commercial real estate asset. By replacing outdated operator–vendor systems with a unified AI-driven platform, Vend Park is helping major property owners boost NOI by up to 30%, slash operating costs, and modernize the tenant experience. As the company expands from three to fifteen cities and partners with giants like Nuveen and Jamestown, its technology highlights a major shift: real estate professionals must now understand AI, automation, and digital infrastructure to stay competitive.

Keller Williams Realty Atlanta Partners has formed an exclusive partnership with Southeast Mortgage, Georgia’s largest non‑bank mortgage lender. The collaboration promises faster, tech‑enhanced transactions for both agents and homebuyers, combining real estate expertise with streamlined mortgage services. This move reflects a growing trend toward integrated real‑estate ecosystems designed to reduce delays, boost transparency, and modernize the homebuying experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}