Surviving the Storm: Navigating Insurance and FEMA After Hurricane Helene

In the aftermath of Hurricane Helene, homeowners in North Carolina face the daunting challenge of securing compensation from insurance companies and the federal government. As reported by Christopher Flavelle and Emily Flitter of The New York Times, the process can be both infuriating and baffling, yet it is essential for recovery.

The key to overcoming these obstacles lies in meticulous documentation and understanding of insurance policies. As homeowners grapple with the aftermath, experts emphasize the importance of photographing damage and keeping detailed records of all interactions with insurers and government agencies.

Insurance Challenges

Many insurers are increasingly dropping customers who file claims, making it crucial for policyholders to understand their coverage specifics. With disaster-related deductibles often ranging from $1,000 to $5,000, homeowners must weigh the potential risks of filing claims for minor damages.

Flood damage presents another layer of complexity. Most standard home insurance policies do not cover flood damage, and distinguishing between flood and other types of damage is essential. According to Douglas Heller of the Consumer Federation of America, many homes in North Carolina suffered from landslides or mudflows, which may not be covered without specialized flood insurance.

Seeking Professional Help

When disputes arise, public adjusters and legal aid can be invaluable. Public adjusters negotiate with insurers to secure larger settlements, while legal assistance may be necessary if disputes remain unresolved. Chip Merlin, a Tampa-based lawyer, advises consulting legal professionals, especially for substantial claims.

FEMA Assistance

For those without adequate insurance, FEMA’s Individual Assistance program offers a lifeline. The program provides emergency housing assistance and other forms of aid. However, as highlighted by Reese May of SBP, appealing FEMA’s decisions can significantly increase the amount of assistance received.

For more information on FEMA housing assistance, visit their official website.

Community and Government Aid

In addition to insurance and FEMA, survivors can explore other avenues for assistance. Low-interest loans from the U.S. Small Business Administration, crowdfunding campaigns, and charitable organizations provide vital support. In cases of major disasters, Congress may authorize additional funding through the U.S. Department of Housing and Urban Development.

As the journey to recovery continues, the resilience and persistence of affected communities remain crucial. By staying informed and proactive, homeowners can navigate the complexities of post-disaster recovery with greater confidence and assurance.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

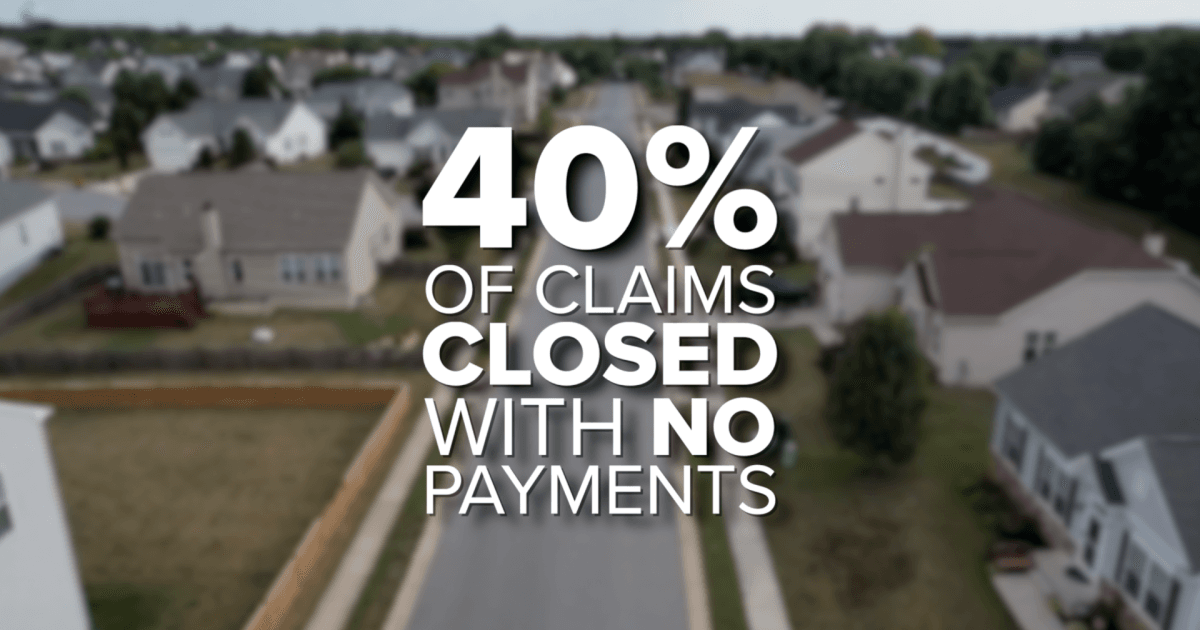

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}