Surviving the Storm: Navigating Insurance and FEMA After Hurricane Helene

In the aftermath of Hurricane Helene, homeowners in North Carolina face the daunting challenge of securing compensation from insurance companies and the federal government. As reported by Christopher Flavelle and Emily Flitter of The New York Times, the process can be both infuriating and baffling, yet it is essential for recovery.

The key to overcoming these obstacles lies in meticulous documentation and understanding of insurance policies. As homeowners grapple with the aftermath, experts emphasize the importance of photographing damage and keeping detailed records of all interactions with insurers and government agencies.

Insurance Challenges

Many insurers are increasingly dropping customers who file claims, making it crucial for policyholders to understand their coverage specifics. With disaster-related deductibles often ranging from $1,000 to $5,000, homeowners must weigh the potential risks of filing claims for minor damages.

Flood damage presents another layer of complexity. Most standard home insurance policies do not cover flood damage, and distinguishing between flood and other types of damage is essential. According to Douglas Heller of the Consumer Federation of America, many homes in North Carolina suffered from landslides or mudflows, which may not be covered without specialized flood insurance.

Seeking Professional Help

When disputes arise, public adjusters and legal aid can be invaluable. Public adjusters negotiate with insurers to secure larger settlements, while legal assistance may be necessary if disputes remain unresolved. Chip Merlin, a Tampa-based lawyer, advises consulting legal professionals, especially for substantial claims.

FEMA Assistance

For those without adequate insurance, FEMA’s Individual Assistance program offers a lifeline. The program provides emergency housing assistance and other forms of aid. However, as highlighted by Reese May of SBP, appealing FEMA’s decisions can significantly increase the amount of assistance received.

For more information on FEMA housing assistance, visit their official website.

Community and Government Aid

In addition to insurance and FEMA, survivors can explore other avenues for assistance. Low-interest loans from the U.S. Small Business Administration, crowdfunding campaigns, and charitable organizations provide vital support. In cases of major disasters, Congress may authorize additional funding through the U.S. Department of Housing and Urban Development.

As the journey to recovery continues, the resilience and persistence of affected communities remain crucial. By staying informed and proactive, homeowners can navigate the complexities of post-disaster recovery with greater confidence and assurance.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Skyrocketing insurance premiums and soaring rebuilding costs are transforming communities across Southwest Florida, especially in the wake of Hurricane Ian. As longtime residents struggle to keep up with rising financial pressure, wealthier newcomers and stricter building standards are reshaping the identity of places like Fort Myers Beach. With insurance rates now driving home sales, triggering potential foreclosures, and squeezing both owners and renters, Florida’s middle-class families face a growing question: can they afford to stay in the state they love?

Florida’s insurance industry is stabilizing fast, with nearly 1.6 million policies shifting from Citizens to private insurers and litigation dropping sharply. Regulators report stronger market confidence, decreasing premiums, and renewed competition—signaling one of the healthiest periods the state has seen in years.

A Leon County judge has ordered the restart of arbitration for Citizens Property Insurance claims, directly conflicting with a previous ruling that halted the process as potentially unconstitutional. With more than 400 cases now back in motion, real estate, insurance, and mortgage professionals can expect renewed activity in claim disputes and fresh uncertainty as Florida courts clash over the legality of Citizens’ arbitration system.

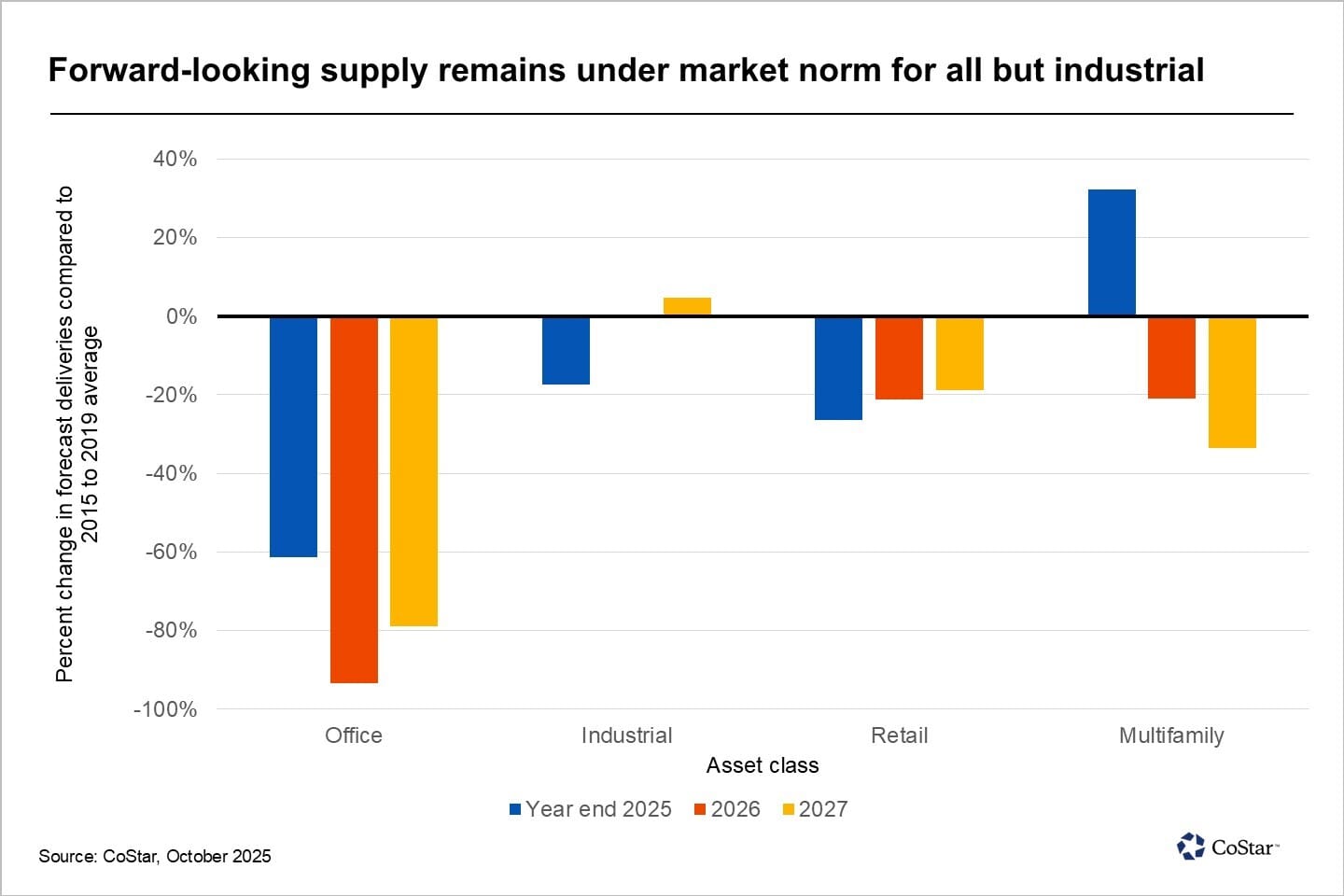

The DFW market is transitioning into a new construction phase marked by a slowdown in office development, a more selective approach to industrial projects, and an evolving housing landscape shaped by affordability and population growth. Developers are recalibrating their priorities, and for real estate professionals, understanding these shifts offers a critical edge in navigating—and capitalizing on—the next phase of the metroplex’s growth.

A new federal lawsuit claims Zillow pushed homebuyers toward Zillow Home Loans by rewarding affiliated agents with valuable leads — all without proper disclosure. The suit alleges undisclosed incentives, referral quotas, and potential RESPA violations, raising major concerns about steering, fiduciary duties, and Zillow’s expanding mortgage ambitions.

The mortgage industry is evolving fast, and the lenders who come out on top will be those who innovate without uprooting what already works. By building on strong technology foundations, streamlining workflows and adopting smart automation, lenders can reduce costs, improve customer experience and stay resilient in any market cycle. This article breaks down why innovation matters now, how a stable tech ecosystem protects lenders in volatile conditions and why small, strategic steps can drive long-term transformation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}