The 2025–2026 Insurance Risk Agenda: What Every Professional Needs to Know

The insurance world didn’t ease up in 2025 — and for 2026, the pressure only intensifies. Today’s insurers are being pulled in two very different directions: innovate faster than ever while simultaneously tightening controls under rising regulatory, geopolitical and economic turbulence. For professionals across insurance, finance, mortgage, and compliance, this dual reality defines the year ahead.

InsuranceNewsNet recently highlighted the key forces shaping the coming cycle, and the picture is clear: growth and innovation now require smarter, more disciplined risk management than at any point in the past decade.

1. AI Acceleration and the Governance Crunch

Artificial intelligence is no longer experimental — it’s operational. In 2025, insurers shifted rapidly to AI-supported underwriting, dynamic pricing, and real-time risk selection. The result? Massive opportunity paired with new forms of exposure.

Key risks include:

• Model drift and explainability issues

• Heightened fairness and discrimination scrutiny

• Deepened board expectations for oversight

Digital transformation demands speed, but cyber resilience and governance demand discipline. Insurers that master both will hold the competitive edge in 2026.

2. Stricter Oversight of Third-Party Vendors

Regulators increasingly view third-party vendors as extensions of the insurer itself. In 2025, the NAIC intensified scrutiny of PBMs, data providers, modeling vendors and third-party administrators.

For PBMs, the regulatory shift is especially sharp, with new examination frameworks and robust data gathering protocols. For insurers, this means documented oversight is now non-negotiable.

Other high-focus areas include:

• Predictive model vendors

• Annuity suitability partners (no more “we outsourced it”)

• Third-party administrators and standardized licensing

Vendor governance now requires the same rigor as capital management: structured, evidence-driven, and continuously updated.

3. Volatile Markets, Rates and Global Pressures

Rate volatility remained stubborn in 2025, impacting capital strategies, policyholder behavior, reinsurance structures and solvency metrics. With global tensions rising, insurers face pressure on catastrophic losses, offshore reinsurance scrutiny and earnings stability.

Property and casualty carriers continue to face elevated catastrophe losses — about $107 billion last year alone — fueled by events like the California Palisades Fire.

Health insurers grappled with premium deficiencies, while life insurers benefitted from attractive long-term spreads but struggled with legacy guarantees.

4. The Growing Talent Gap

The industry’s talent shortage is no longer looming — it’s here. Retirements are accelerating, and fewer young professionals are entering the field. Highly technical roles, from actuarial to compliance analytics, face particularly significant shortages.

This creates both a challenge and an enormous opportunity for professionals investing in upskilling and licensure.

What 2026 Demands from Insurance Leaders

Across all risk categories, four priorities stand out:

• Bring risk and compliance into strategic decision-making

• Industrialize vendor and model governance

• Invest in talent, technology and professional education

• Build pricing and capital structures that can flex with volatility

2025 was a stress test — 2026 is the proving ground.

Where Cameron Academy Fits In

With the industry evolving at record speed, staying licensed, certified and professionally competitive is more important than ever. Cameron Academy’s insurance, finance and compliance programs help both new and seasoned professionals build the expertise regulators now demand. Whether you’re upskilling, reskilling or stepping into the field for the first time, Cameron Academy keeps you ahead of the curve — in all 50 states.

For full context and deeper insights, explore the original feature at InsuranceNewsNet, a trusted source in professional insurance reporting.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

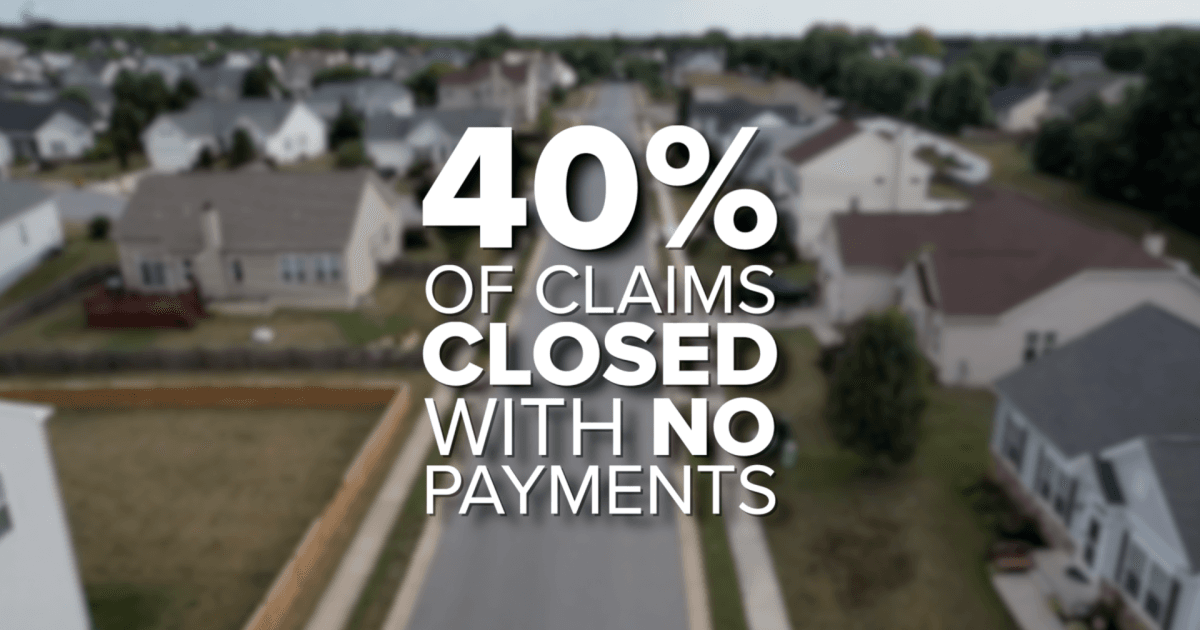

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}