The 3D Printing Construction Market: A Future of Growth and Innovation

The global 3D printing construction market is on the brink of a remarkable transformation. Currently valued at USD 0.34 billion in 2023, it is projected to surge to USD 910 million by 2024, and ultimately reach USD 2.3 billion by 2032. This rapid expansion is fueled by the sector’s potential to revolutionize traditional building processes through innovative additive manufacturing technologies.

Key Market Trends

The rise of sustainable construction practices is one of the most significant trends driving this market. 3D printing not only reduces material waste but also facilitates the use of eco-friendly materials, a crucial factor as the construction industry seeks to reduce its carbon footprint. Moreover, this technology supports accelerated affordable housing solutions, cutting down both construction times and costs, which is essential in addressing global housing shortages.

Drivers of Market Growth

Labor shortages are a pressing issue in the construction industry, prompting a shift towards 3D printing. With an aging workforce and a scarcity of skilled labor, companies are increasingly turning to automation to reduce labor dependency. Additionally, the growing demand for customized construction projects is encouraging the adoption of 3D printing, allowing for the creation of intricate, tailored designs that cater to urban and cultural needs.

Government support is also playing a pivotal role in market growth. Initiatives like Saudi Arabia’s Vision 2030 and the European Union’s Horizon 2020 program are promoting the use of 3D printing in construction, further bolstering the market’s expansion.

Challenges and Opportunities

Despite its promising advancements, the 3D printing construction market faces challenges such as the high initial capital investment required for equipment and a lack of skilled workforce to operate these technologies. However, opportunities abound, particularly in disaster-relief housing and the integration of 3D printing with smart city initiatives.

Regional Insights

In 2023, North America led the market, holding a 35.8% share, thanks to significant investments and technological advancements. Europe is also experiencing robust growth driven by sustainability initiatives, while Asia-Pacific remains the fastest-growing region due to rapid urbanization and a high demand for affordable housing.

Key Players and Recent Developments

Major companies such as WinSun, Apis Cor, and ICON are at the forefront of exploring new frontiers in 3D construction. Recent advancements include Apis Cor’s development of robotic printers and CyBe Construction’s collaborations in the Middle East for affordable housing projects. The introduction of the BetAbram P1 printer and Sika AG’s innovative concrete mix further highlight the industry’s ongoing efforts towards scalability and sustainability.

Overall, the 3D printing construction market is poised for significant growth, driven by its potential to redefine construction methodologies and effectively meet global demands.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A growing share of American homeowners now carry mortgage rates above 5%—a dramatic shift that’s reshaping refinancing, inventory, and buyer behavior nationwide. With more than 30% of borrowers locked into rates over 5% and 20% above 6%, the market is split between owners holding on to low pandemic‑era loans and new buyers taking on higher‑rate mortgages. Federal efforts to push rates down could unlock millions of refinancing opportunities, while buyers see only modest monthly savings. For real estate professionals, understanding these rate dynamics is crucial as they increasingly drive inventory levels, affordability, and market activity.

New Moody’s data shows commercial real estate deal volume slipped 20% in December, marking a second monthly decline. Yet the full year tells a different story: 2025 ended with a 17% gain, signaling a quiet but resilient recovery. The biggest surprise came from the office sector, which posted a 21% jump in activity as return‑to‑office trends and AI‑driven job growth boosted demand. Multifamily, retail, and alternative assets like data centers also saw strong momentum, giving real estate professionals a market full of fresh opportunities heading into 2026.

Florida drivers and industry professionals are heading into 2026 with good news: auto insurance rates are dropping across the state as the market shows strong signs of stabilization. USAA leads the latest wave with a 7% average rate decrease expected in May 2026, saving members more than $125 million annually. They join several major insurers — including State Farm, Progressive, AAA, Allstate, and Florida Farm Bureau — all approving significant reductions. Officials credit recent legislative reforms, especially tort reform, for the improved loss ratios and renewed insurer confidence. With both auto and home insurance markets strengthening, Florida’s real estate, mortgage, and insurance professionals can expect more consumer confidence, smoother transactions, and expanding career opportunities.

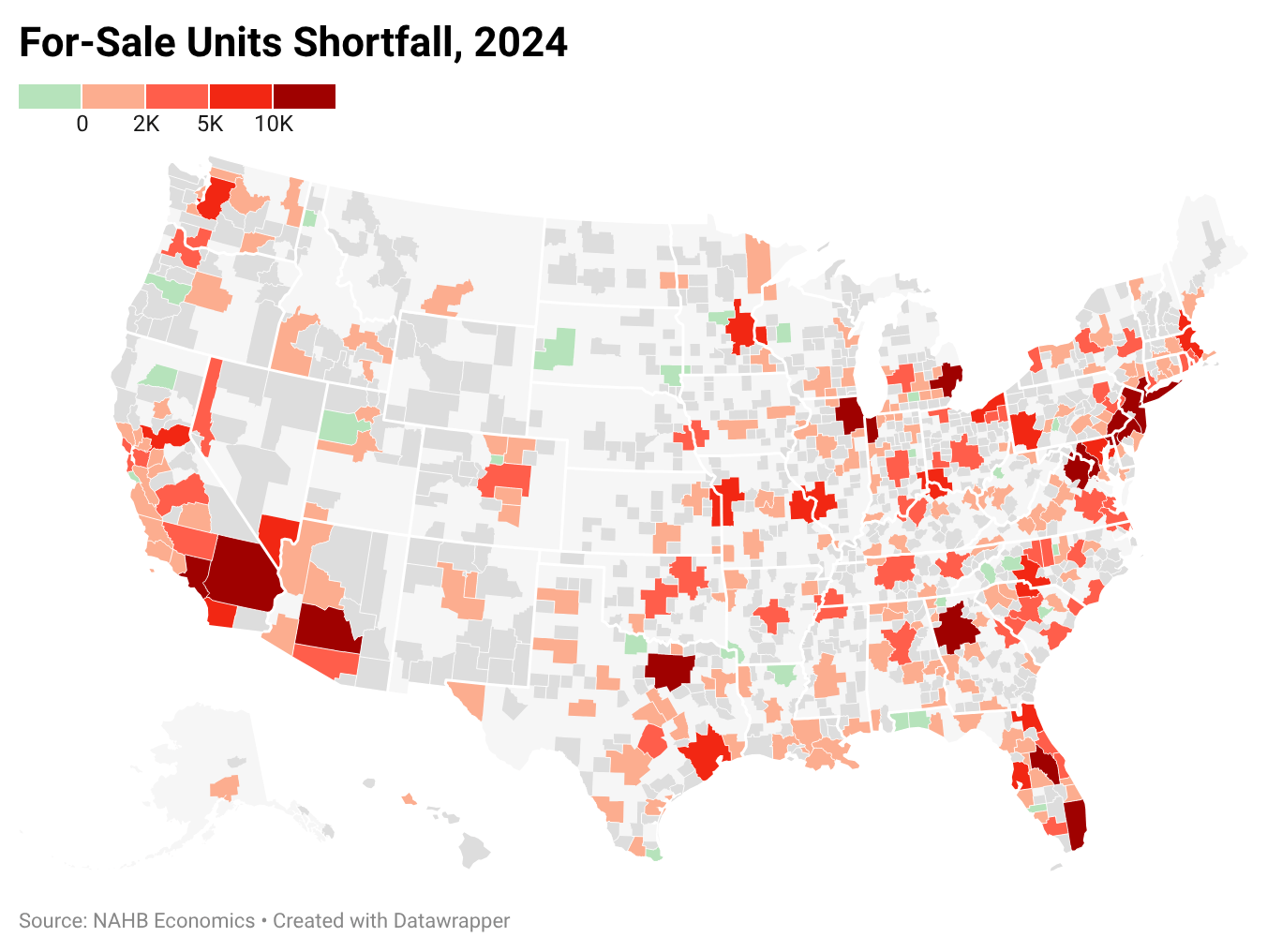

New data from Eye On Housing and the NAHB shows the U.S. remains short more than 1.2 million housing units, keeping pressure on both rents and home prices. Record‑low vacancy rates, slow single‑family construction, and restrictive zoning continue to fuel intense competition in 2024. Major metros like Chicago, New York, and Atlanta face some of the deepest deficits, and the true nationwide shortfall may be even higher when accounting for overcrowding and aging homes. For real estate professionals, the ongoing shortage means sustained demand, tighter inventory, and major opportunities for those who understand the evolving market.

Top real estate coach Jason Pantana says the divide between agents today isn’t about who has “tried” AI — it’s about who is immersed in it. In a new HousingWire interview, he explains why AI isn’t a gimmick but a full business system that amplifies output, improves authenticity, and reshapes how clients search for agents. From prompt mastery to AI‑driven visibility on Google, Pantana reveals how agents who commit even 15 minutes a day to learning AI are already outperforming those who hesitate.

Dallas–Fort Worth’s commercial real estate market closed 2025 with a split personality. Industrial dominated with massive new deliveries and soaring leasing demand, retail held steady with some of the market’s strongest fundamentals in years, and office continued to falter under remote‑work pressures. High vacancies, weak absorption, and rising demand for top‑tier space show the sector’s ongoing reset. Meanwhile, industrial and retail strength position the Metroplex for another powerhouse year heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}