The Crisis Beneath the Ashes: How the LA Wildfires Exposed a National Insurance Meltdown

When Jessica and Matt Conkle lost their Altadena home to last year’s Los Angeles wildfires, they expected their insurance coverage to help them rebuild their lives. Instead, they found themselves trapped in an exhausting maze of delays, lowball estimates, and unanswered calls — a struggle increasingly familiar to thousands of wildfire survivors across California.

Their story, originally reported by The Guardian (read full piece), highlights a crisis shaking the foundation of American homeownership: the unraveling of the national insurance system in an age of rising climate extremes.

When Disaster Strikes… and Then the Delays Begin

The Conkles received four months of temporary living assistance — but everything after that fell into a black hole. Adjusters rotated. Values fluctuated. Their Waterford crystal? Deemed to have instantly dropped more than half in value. Proof of condition? Lost in the fire — a reality their insurer seemed unmoved by.

Rebuilding wasn’t any easier. The insurer’s first estimate was far below market reality and excluded essential architectural fees and city permits. Today, their rebuild funds sit frozen in escrow as negotiations drag on.

Tap to reflect:

Are delays and lowball estimates becoming the new norm for wildfire‑zone claims? Many real estate and insurance experts say yes — and the ripple effects are reshaping markets nationwide.

A System Cracking Under Climate Pressure

A Department of Angels survey revealed that nearly 80% of wildfire survivors faced major obstacles: rotating adjusters, inconsistent valuations, and long communication gaps. Even homeowners with only partial damage — supposedly simpler claims — faced some of the steepest challenges.

This isn’t just a California hardship. Across the country, insurers are withdrawing from high‑risk areas, raising premiums, or scaling back coverage entirely. State emergency insurance programs are ballooning as under‑insurance quietly spreads nationwide.

Yet the insurance giants themselves are reporting record profits, largely off investment income — a contradiction not lost on consumers.

Regulators Under Fire

Consumer advocates argue that regulators in several states have been too lenient, bending to industry pressure and approving steep rate hikes without demanding stronger protections. In California, the Department of Insurance has faced intense scrutiny — even allegations of being “bullied” into decisions that favor insurers over homeowners.

One major shift came when LA County launched an investigation into State Farm’s wildfire claims handling. Suddenly, months‑long stalled claims saw progress — a change many advocates credit to heightened accountability.

Quick Insight:

Policy pressure — not just disaster — may be the strongest force shaping modern insurance behavior.

The Bigger Picture: An Uninsurable Future?

As climate‑driven disasters multiply, insurers are reevaluating risk faster than regulations can adapt. With billions lost annually, companies are adjusting coverage models, tightening their underwriting, and passing more risk to consumers.

Former California insurance commissioner Dave Jones warns that these trends point toward an “uninsurable future” unless climate change is addressed at scale.

For now, homeowners face rising premiums, shrinking policies, and unmet rebuild needs. As the Conkle family learned, being insured doesn’t always mean being protected.

Why This Matters for Real Estate and Professional Licensing

For real estate agents, mortgage professionals, and insurance specialists, this crisis hits close to home. Every shift in the insurance landscape affects market stability: transactions slow, lending tightens, risk premiums climb, and entire neighborhoods change overnight based on insurance availability.

This is why strong professional education is more essential than ever. At Cameron Academy, future and current professionals stay ahead of these shifting dynamics through licensing and continuing education in real estate, insurance, mortgage, and more — across all 50 states. Understanding today’s insurance volatility isn’t optional; it’s part of being truly prepared.

A Call for Fairness

Survivors like the Conkles aren’t demanding special treatment — they’re asking for the protection they paid for. As climate volatility increases, the call for transparency and accountability in insurance practices will only grow stronger.

Their fight continues — echoing across the entire nation as communities, professionals, and policymakers confront a new era of risk, resilience, and rebuilding.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A growing share of American homeowners now carry mortgage rates above 5%—a dramatic shift that’s reshaping refinancing, inventory, and buyer behavior nationwide. With more than 30% of borrowers locked into rates over 5% and 20% above 6%, the market is split between owners holding on to low pandemic‑era loans and new buyers taking on higher‑rate mortgages. Federal efforts to push rates down could unlock millions of refinancing opportunities, while buyers see only modest monthly savings. For real estate professionals, understanding these rate dynamics is crucial as they increasingly drive inventory levels, affordability, and market activity.

New Moody’s data shows commercial real estate deal volume slipped 20% in December, marking a second monthly decline. Yet the full year tells a different story: 2025 ended with a 17% gain, signaling a quiet but resilient recovery. The biggest surprise came from the office sector, which posted a 21% jump in activity as return‑to‑office trends and AI‑driven job growth boosted demand. Multifamily, retail, and alternative assets like data centers also saw strong momentum, giving real estate professionals a market full of fresh opportunities heading into 2026.

Florida drivers and industry professionals are heading into 2026 with good news: auto insurance rates are dropping across the state as the market shows strong signs of stabilization. USAA leads the latest wave with a 7% average rate decrease expected in May 2026, saving members more than $125 million annually. They join several major insurers — including State Farm, Progressive, AAA, Allstate, and Florida Farm Bureau — all approving significant reductions. Officials credit recent legislative reforms, especially tort reform, for the improved loss ratios and renewed insurer confidence. With both auto and home insurance markets strengthening, Florida’s real estate, mortgage, and insurance professionals can expect more consumer confidence, smoother transactions, and expanding career opportunities.

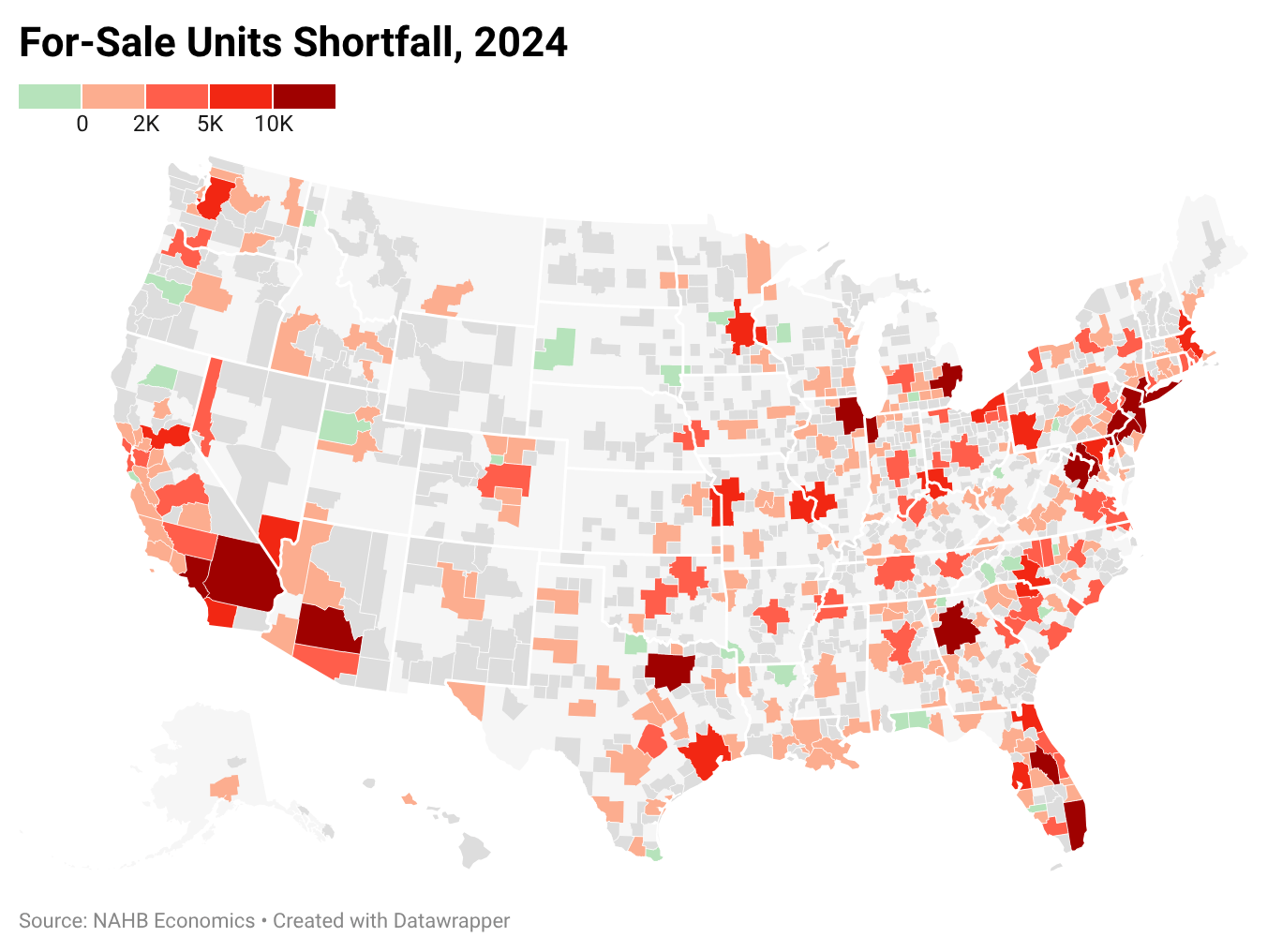

New data from Eye On Housing and the NAHB shows the U.S. remains short more than 1.2 million housing units, keeping pressure on both rents and home prices. Record‑low vacancy rates, slow single‑family construction, and restrictive zoning continue to fuel intense competition in 2024. Major metros like Chicago, New York, and Atlanta face some of the deepest deficits, and the true nationwide shortfall may be even higher when accounting for overcrowding and aging homes. For real estate professionals, the ongoing shortage means sustained demand, tighter inventory, and major opportunities for those who understand the evolving market.

Top real estate coach Jason Pantana says the divide between agents today isn’t about who has “tried” AI — it’s about who is immersed in it. In a new HousingWire interview, he explains why AI isn’t a gimmick but a full business system that amplifies output, improves authenticity, and reshapes how clients search for agents. From prompt mastery to AI‑driven visibility on Google, Pantana reveals how agents who commit even 15 minutes a day to learning AI are already outperforming those who hesitate.

Dallas–Fort Worth’s commercial real estate market closed 2025 with a split personality. Industrial dominated with massive new deliveries and soaring leasing demand, retail held steady with some of the market’s strongest fundamentals in years, and office continued to falter under remote‑work pressures. High vacancies, weak absorption, and rising demand for top‑tier space show the sector’s ongoing reset. Meanwhile, industrial and retail strength position the Metroplex for another powerhouse year heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}