The Crisis Beneath the Ashes: How the LA Wildfires Exposed a National Insurance Meltdown

When Jessica and Matt Conkle lost their Altadena home to last year’s Los Angeles wildfires, they expected their insurance coverage to help them rebuild their lives. Instead, they found themselves trapped in an exhausting maze of delays, lowball estimates, and unanswered calls — a struggle increasingly familiar to thousands of wildfire survivors across California.

Their story, originally reported by The Guardian (read full piece), highlights a crisis shaking the foundation of American homeownership: the unraveling of the national insurance system in an age of rising climate extremes.

When Disaster Strikes… and Then the Delays Begin

The Conkles received four months of temporary living assistance — but everything after that fell into a black hole. Adjusters rotated. Values fluctuated. Their Waterford crystal? Deemed to have instantly dropped more than half in value. Proof of condition? Lost in the fire — a reality their insurer seemed unmoved by.

Rebuilding wasn’t any easier. The insurer’s first estimate was far below market reality and excluded essential architectural fees and city permits. Today, their rebuild funds sit frozen in escrow as negotiations drag on.

Tap to reflect:

Are delays and lowball estimates becoming the new norm for wildfire‑zone claims? Many real estate and insurance experts say yes — and the ripple effects are reshaping markets nationwide.

A System Cracking Under Climate Pressure

A Department of Angels survey revealed that nearly 80% of wildfire survivors faced major obstacles: rotating adjusters, inconsistent valuations, and long communication gaps. Even homeowners with only partial damage — supposedly simpler claims — faced some of the steepest challenges.

This isn’t just a California hardship. Across the country, insurers are withdrawing from high‑risk areas, raising premiums, or scaling back coverage entirely. State emergency insurance programs are ballooning as under‑insurance quietly spreads nationwide.

Yet the insurance giants themselves are reporting record profits, largely off investment income — a contradiction not lost on consumers.

Regulators Under Fire

Consumer advocates argue that regulators in several states have been too lenient, bending to industry pressure and approving steep rate hikes without demanding stronger protections. In California, the Department of Insurance has faced intense scrutiny — even allegations of being “bullied” into decisions that favor insurers over homeowners.

One major shift came when LA County launched an investigation into State Farm’s wildfire claims handling. Suddenly, months‑long stalled claims saw progress — a change many advocates credit to heightened accountability.

Quick Insight:

Policy pressure — not just disaster — may be the strongest force shaping modern insurance behavior.

The Bigger Picture: An Uninsurable Future?

As climate‑driven disasters multiply, insurers are reevaluating risk faster than regulations can adapt. With billions lost annually, companies are adjusting coverage models, tightening their underwriting, and passing more risk to consumers.

Former California insurance commissioner Dave Jones warns that these trends point toward an “uninsurable future” unless climate change is addressed at scale.

For now, homeowners face rising premiums, shrinking policies, and unmet rebuild needs. As the Conkle family learned, being insured doesn’t always mean being protected.

Why This Matters for Real Estate and Professional Licensing

For real estate agents, mortgage professionals, and insurance specialists, this crisis hits close to home. Every shift in the insurance landscape affects market stability: transactions slow, lending tightens, risk premiums climb, and entire neighborhoods change overnight based on insurance availability.

This is why strong professional education is more essential than ever. At Cameron Academy, future and current professionals stay ahead of these shifting dynamics through licensing and continuing education in real estate, insurance, mortgage, and more — across all 50 states. Understanding today’s insurance volatility isn’t optional; it’s part of being truly prepared.

A Call for Fairness

Survivors like the Conkles aren’t demanding special treatment — they’re asking for the protection they paid for. As climate volatility increases, the call for transparency and accountability in insurance practices will only grow stronger.

Their fight continues — echoing across the entire nation as communities, professionals, and policymakers confront a new era of risk, resilience, and rebuilding.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida families are feeling the squeeze as everyday costs, insurance premiums, and homeownership barriers continue to climb. House District 102 candidate Jayden D’Onofrio is calling for a broader, more unified affordability strategy—one that tackles the state’s insurance crisis, supports first‑time homebuyers, and restores real competition in the market. His message centers on transparency, practical solutions, and keeping Florida livable for the professionals, workers, and families who power its economy.

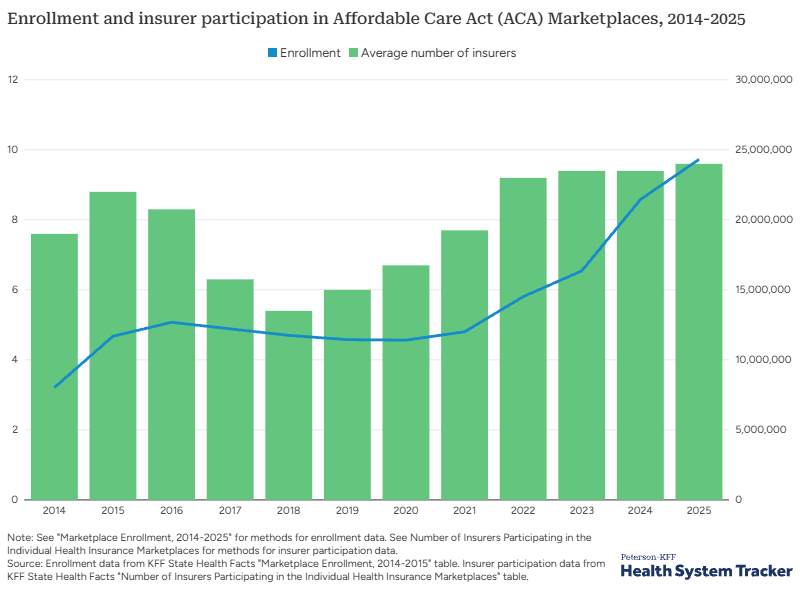

A decade of dramatic change is reshaping America’s health insurance markets. Employer group plans are becoming increasingly dominated by a few powerful insurers, while the ACA individual marketplace is experiencing record‑breaking competition and enrollment. Self‑funded plans are surging, small‑group premiums are driving employers to new coverage models, and major policy shifts in 2025 could redefine affordability for millions. This data‑driven Peterson‑KFF analysis breaks down the trends every insurance, finance, and business professional needs to understand as the industry enters a transformative new era.

Sarasota County is inching closer to approving Winchester Ranch, a massive 8,999‑home community planned for more than 3,100 acres in North Port. With a 7‑1 vote from the Planning Commission and a final decision expected in early 2026, the project could become one of Southwest Florida’s largest developments in decades—bringing new housing, commercial space, and industry while raising fresh questions about growth, the environment, and the region’s rapidly evolving real estate market.

Lument Finance Trust has closed a major $663.8 million commercial real estate CLO, marking one of the standout CRE finance deals of 2025. The transaction, LMNT 2025-FL3, features a strong reinvestment period, non‑recourse and non‑mark‑to‑market financing, and a diversified pool of 32 loans tied to 49 properties nationwide. With J.P. Morgan leading the structuring and more than $585 million placed in investment‑grade securities, the deal highlights renewed stability in transitional CRE debt—making it a development real estate and finance professionals will want to watch closely.

Walmart has partnered with Alquist 3D to roll out the nation’s first large‑scale wave of 3D‑printed commercial buildings, signaling a major shift in how future retail and industrial spaces will be constructed. After completing an 8,000‑square‑foot 3D‑printed expansion in Tennessee—the largest of its kind—the company is moving forward with over a dozen new projects nationwide, accelerating a tech‑driven transformation in commercial real estate.

Citizens Property Insurance Corp. is recommending statewide rate reductions for 2026—the first proposed decrease in more than a decade. Most Citizens policyholders could see an average 11.5% drop, reflecting recent insurance‑market reforms that have stabilized Florida’s turbulent property sector. With hundreds of thousands of policies moving back to private insurers and state‑backed Citizens shrinking to record‑low enrollment, real estate and insurance professionals should prepare for how lower premiums may influence affordability, buyer confidence, and market activity heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}