The Crisis Beneath the Ashes: How the LA Wildfires Exposed a National Insurance Meltdown

When Jessica and Matt Conkle lost their Altadena home to last year’s Los Angeles wildfires, they expected their insurance coverage to help them rebuild their lives. Instead, they found themselves trapped in an exhausting maze of delays, lowball estimates, and unanswered calls — a struggle increasingly familiar to thousands of wildfire survivors across California.

Their story, originally reported by The Guardian (read full piece), highlights a crisis shaking the foundation of American homeownership: the unraveling of the national insurance system in an age of rising climate extremes.

When Disaster Strikes… and Then the Delays Begin

The Conkles received four months of temporary living assistance — but everything after that fell into a black hole. Adjusters rotated. Values fluctuated. Their Waterford crystal? Deemed to have instantly dropped more than half in value. Proof of condition? Lost in the fire — a reality their insurer seemed unmoved by.

Rebuilding wasn’t any easier. The insurer’s first estimate was far below market reality and excluded essential architectural fees and city permits. Today, their rebuild funds sit frozen in escrow as negotiations drag on.

Tap to reflect:

Are delays and lowball estimates becoming the new norm for wildfire‑zone claims? Many real estate and insurance experts say yes — and the ripple effects are reshaping markets nationwide.

A System Cracking Under Climate Pressure

A Department of Angels survey revealed that nearly 80% of wildfire survivors faced major obstacles: rotating adjusters, inconsistent valuations, and long communication gaps. Even homeowners with only partial damage — supposedly simpler claims — faced some of the steepest challenges.

This isn’t just a California hardship. Across the country, insurers are withdrawing from high‑risk areas, raising premiums, or scaling back coverage entirely. State emergency insurance programs are ballooning as under‑insurance quietly spreads nationwide.

Yet the insurance giants themselves are reporting record profits, largely off investment income — a contradiction not lost on consumers.

Regulators Under Fire

Consumer advocates argue that regulators in several states have been too lenient, bending to industry pressure and approving steep rate hikes without demanding stronger protections. In California, the Department of Insurance has faced intense scrutiny — even allegations of being “bullied” into decisions that favor insurers over homeowners.

One major shift came when LA County launched an investigation into State Farm’s wildfire claims handling. Suddenly, months‑long stalled claims saw progress — a change many advocates credit to heightened accountability.

Quick Insight:

Policy pressure — not just disaster — may be the strongest force shaping modern insurance behavior.

The Bigger Picture: An Uninsurable Future?

As climate‑driven disasters multiply, insurers are reevaluating risk faster than regulations can adapt. With billions lost annually, companies are adjusting coverage models, tightening their underwriting, and passing more risk to consumers.

Former California insurance commissioner Dave Jones warns that these trends point toward an “uninsurable future” unless climate change is addressed at scale.

For now, homeowners face rising premiums, shrinking policies, and unmet rebuild needs. As the Conkle family learned, being insured doesn’t always mean being protected.

Why This Matters for Real Estate and Professional Licensing

For real estate agents, mortgage professionals, and insurance specialists, this crisis hits close to home. Every shift in the insurance landscape affects market stability: transactions slow, lending tightens, risk premiums climb, and entire neighborhoods change overnight based on insurance availability.

This is why strong professional education is more essential than ever. At Cameron Academy, future and current professionals stay ahead of these shifting dynamics through licensing and continuing education in real estate, insurance, mortgage, and more — across all 50 states. Understanding today’s insurance volatility isn’t optional; it’s part of being truly prepared.

A Call for Fairness

Survivors like the Conkles aren’t demanding special treatment — they’re asking for the protection they paid for. As climate volatility increases, the call for transparency and accountability in insurance practices will only grow stronger.

Their fight continues — echoing across the entire nation as communities, professionals, and policymakers confront a new era of risk, resilience, and rebuilding.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

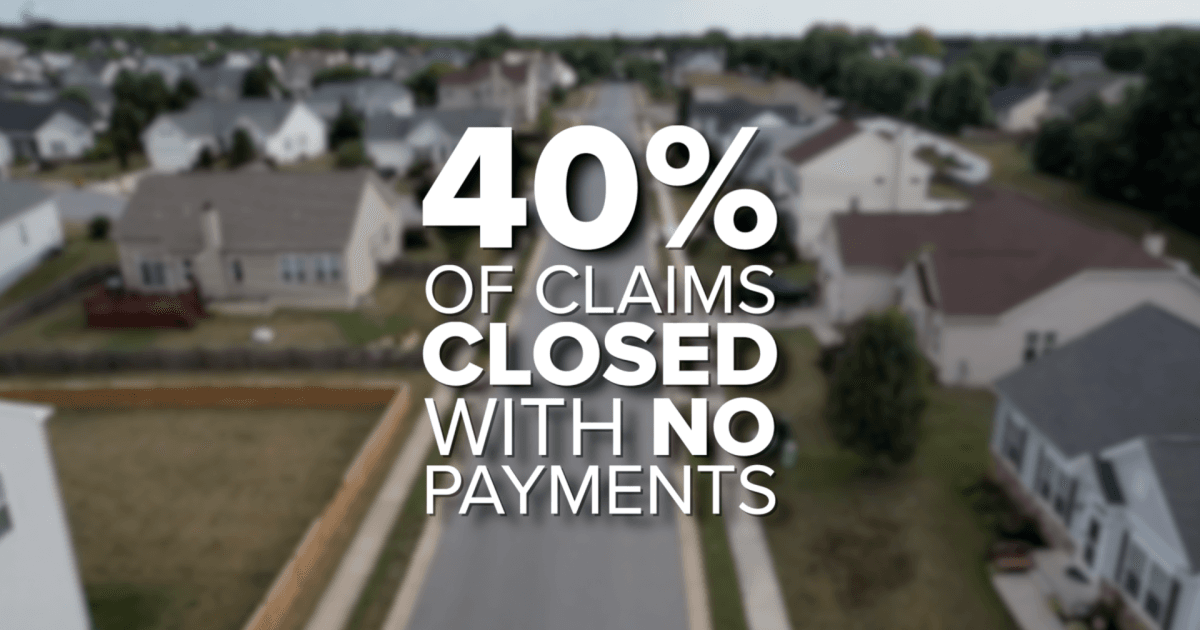

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}