The Fed Just Cut Rates Again — Here’s What It Really Means for Mortgage Shoppers in 2026

The Federal Reserve has officially pushed interest rates to their lowest point since 2022, marking the third rate cut in just four months — and the ripple effects are already spreading across financial markets. With the benchmark federal funds rate now sitting between 3.50% and 3.75%, homebuyers, homeowners, and real estate professionals are eagerly wondering what comes next for mortgage rates.

The original report from CBS News, written by Senior Editor Angelica Leicht, breaks down the facts behind this major shift. We’re taking that information a step further to translate it into what matters for today’s professionals — especially those in real estate, mortgage finance or anyone navigating the housing market landscape.

Tap here to read the full CBS News original article.

The Fed Cut Rates — Will Mortgage Rates Finally Follow?

Here’s the big takeaway: mortgage rates don’t automatically move when the Fed cuts rates. They’re shaped by economic expectations, bond yields and investor sentiment — not the benchmark rate itself.

Still, this cut has weight. When the Fed signals a more dovish outlook, inflation expectations begin to cool and the 10‑year Treasury yield softens — and that yield is the true driver of long‑term mortgage rate movement.

Because the market anticipated this cut weeks ahead of time, lenders have already priced in part of the change. But overall conditions point toward gradual downward pressure in the coming months.

Quick Insight: Watch the 10‑year Treasury. If it trends down, mortgage rates are likely to follow.

How This Could Affect Borrowers

Even a slight dip in mortgage rates can reshape affordability. A reduction of just 0.25% could widen buying options, reduce monthly payments or allow more buyers to qualify.

Homeowners carrying high‑peak 2023 mortgages may finally see new refinancing opportunities in 2026. If rates continue easing, millions could benefit.

Lower borrowing costs also tend to invigorate the real estate market — adding momentum for buyers, sellers, agents, brokers and mortgage originators preparing for a busier year.

Lender Competition May Heat Up

As more consumers enter the market, lenders often sharpen pricing, discounts and incentives. Borrowers who shop around could enjoy meaningful long‑term savings.

Build your edge: Thinking about entering or advancing in real estate or mortgage lending? Cameron Academy offers flexible, online licensing and continuing education programs crafted for today’s evolving market.

The Bottom Line

The Fed’s latest rate cut marks a pivotal moment — not just for financial markets, but for buyers, sellers and professionals across the housing industry. Mortgage rates won’t drop overnight, but the direction is becoming more favorable.

Professionals who stay alert, analyze rate shifts and prepare new scenarios will be best positioned as 2026 unfolds.

And as always, staying informed is one of the strongest professional advantages — and Cameron Academy is committed to keeping you ahead of the curve.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A growing share of American homeowners now carry mortgage rates above 5%—a dramatic shift that’s reshaping refinancing, inventory, and buyer behavior nationwide. With more than 30% of borrowers locked into rates over 5% and 20% above 6%, the market is split between owners holding on to low pandemic‑era loans and new buyers taking on higher‑rate mortgages. Federal efforts to push rates down could unlock millions of refinancing opportunities, while buyers see only modest monthly savings. For real estate professionals, understanding these rate dynamics is crucial as they increasingly drive inventory levels, affordability, and market activity.

New Moody’s data shows commercial real estate deal volume slipped 20% in December, marking a second monthly decline. Yet the full year tells a different story: 2025 ended with a 17% gain, signaling a quiet but resilient recovery. The biggest surprise came from the office sector, which posted a 21% jump in activity as return‑to‑office trends and AI‑driven job growth boosted demand. Multifamily, retail, and alternative assets like data centers also saw strong momentum, giving real estate professionals a market full of fresh opportunities heading into 2026.

Florida drivers and industry professionals are heading into 2026 with good news: auto insurance rates are dropping across the state as the market shows strong signs of stabilization. USAA leads the latest wave with a 7% average rate decrease expected in May 2026, saving members more than $125 million annually. They join several major insurers — including State Farm, Progressive, AAA, Allstate, and Florida Farm Bureau — all approving significant reductions. Officials credit recent legislative reforms, especially tort reform, for the improved loss ratios and renewed insurer confidence. With both auto and home insurance markets strengthening, Florida’s real estate, mortgage, and insurance professionals can expect more consumer confidence, smoother transactions, and expanding career opportunities.

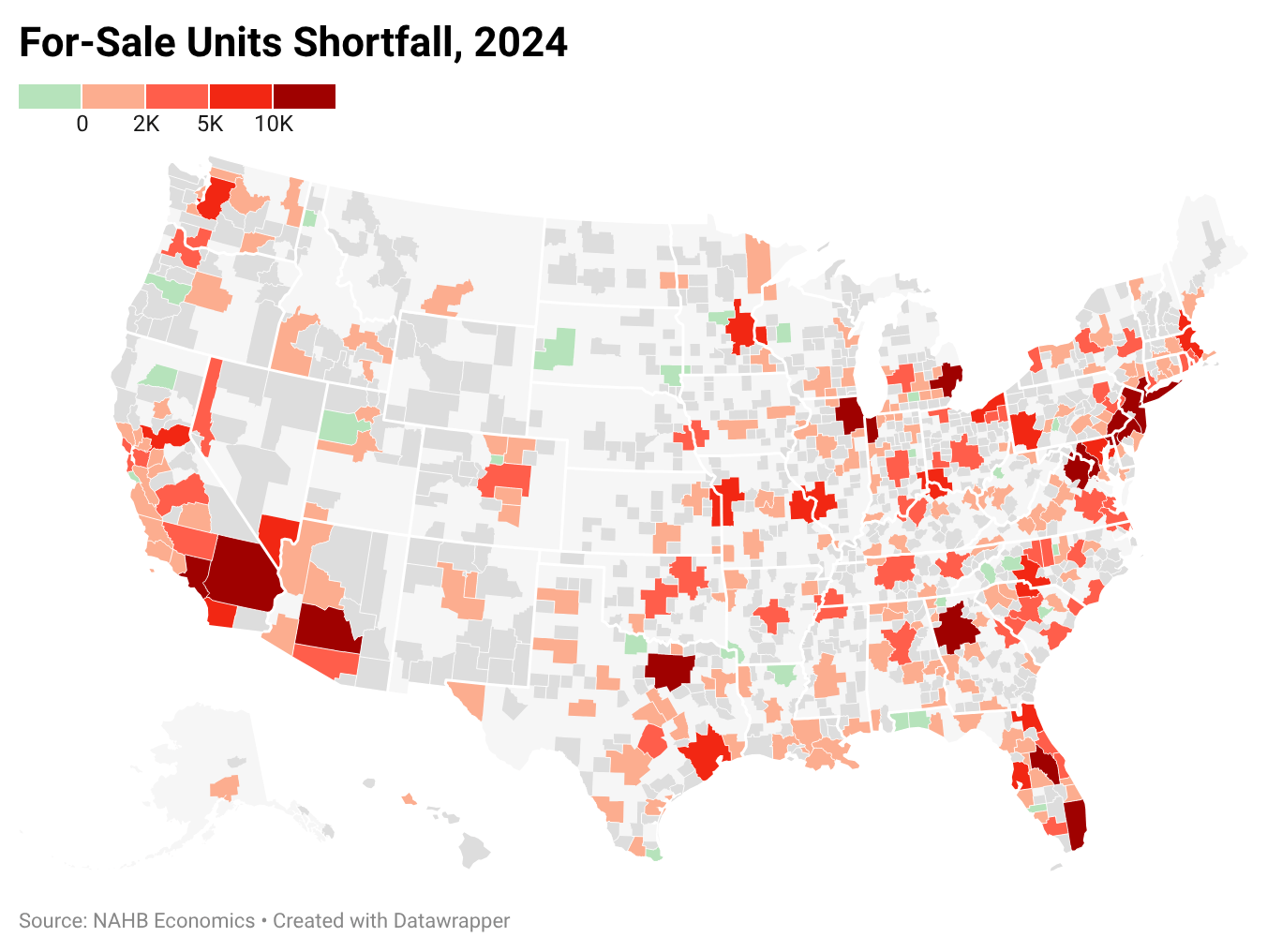

New data from Eye On Housing and the NAHB shows the U.S. remains short more than 1.2 million housing units, keeping pressure on both rents and home prices. Record‑low vacancy rates, slow single‑family construction, and restrictive zoning continue to fuel intense competition in 2024. Major metros like Chicago, New York, and Atlanta face some of the deepest deficits, and the true nationwide shortfall may be even higher when accounting for overcrowding and aging homes. For real estate professionals, the ongoing shortage means sustained demand, tighter inventory, and major opportunities for those who understand the evolving market.

Top real estate coach Jason Pantana says the divide between agents today isn’t about who has “tried” AI — it’s about who is immersed in it. In a new HousingWire interview, he explains why AI isn’t a gimmick but a full business system that amplifies output, improves authenticity, and reshapes how clients search for agents. From prompt mastery to AI‑driven visibility on Google, Pantana reveals how agents who commit even 15 minutes a day to learning AI are already outperforming those who hesitate.

Dallas–Fort Worth’s commercial real estate market closed 2025 with a split personality. Industrial dominated with massive new deliveries and soaring leasing demand, retail held steady with some of the market’s strongest fundamentals in years, and office continued to falter under remote‑work pressures. High vacancies, weak absorption, and rising demand for top‑tier space show the sector’s ongoing reset. Meanwhile, industrial and retail strength position the Metroplex for another powerhouse year heading into 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}