The Impact of FinTech on Sub-Saharan Africa’s Financial Landscape

The financial sector worldwide has been revolutionized by the advent of Financial Technology (FinTech), marking a new phase in the evolution of financial services. According to a detailed analysis by TRENDS Research & Advisory, FinTech’s integration of technological innovations with financial services has brought about a transformative impact, offering novel, flexible, and cost-effective financial products.

Sub-Saharan Africa: A Fertile Ground for FinTech

Sub-Saharan Africa, with its youthful demographic—approximately 40% of its population is under 15—presents a ripe opportunity for FinTech adoption. This region’s large underbanked population, estimated at 42% of adults, underscores the potential for FinTech to drive financial inclusion. The widespread use of mobile technology, with around 650 million mobile users, further enhances this potential. The GSMA Mobile Economy Report highlights that Sub-Saharan Africa leads globally in mobile money transactions, totaling $490 billion in 2020.

Challenges and Opportunities

Despite the promising landscape, FinTech adoption in Sub-Saharan Africa faces several challenges. Regulatory hurdles, infrastructure limitations, and cybersecurity threats are significant barriers. However, these challenges also present opportunities for growth. Policy reforms, investment in infrastructure, and public-private partnerships are vital to overcoming these obstacles and seizing the opportunities FinTech offers.

Success Stories and Future Prospects

Countries like Zambia and Nigeria illustrate the transformative power of FinTech. Zambia has seen a dramatic rise in digital financial inclusion, with active digital financial accounts increasing from 2% to 44% of the adult population between 2014 and 2019. Meanwhile, Nigeria’s FinTech sector is thriving, driven by a tech-savvy population and government support for digital financial solutions.

Looking ahead, the future of FinTech in Sub-Saharan Africa is promising. Emerging technologies such as AI-driven solutions and blockchain applications hold significant potential for enhancing financial services accessibility and efficiency. With continued investment and innovation, FinTech is poised to play a pivotal role in transforming the financial landscape of the region and improving the lives of millions.

Conclusion

The impact of FinTech on Sub-Saharan Africa’s financial services sector is profound, fostering financial inclusion and reshaping traditional banking paradigms. As the region continues to embrace innovative solutions, collaboration among policymakers, regulators, and stakeholders is crucial to harnessing the full potential of FinTech for sustainable growth.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

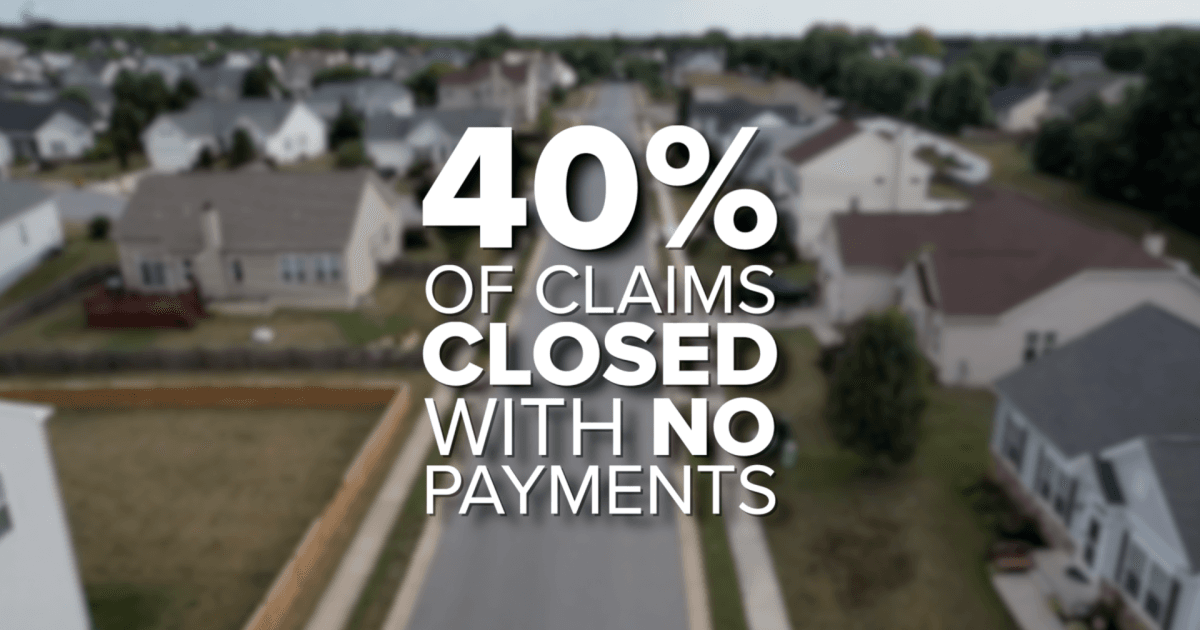

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}