The Outlook for Housing Starts: A Future Defined by Demographics and Demand

The Congressional Budget Office (CBO) has released a comprehensive report on the outlook for housing starts over the next 30 years, highlighting the critical role of population growth and demographic shifts in shaping the future of housing construction in the United States. This analysis, available in full at CBO’s official website, underscores the complex interplay between economic factors and housing demand.

Strong Beginnings and Future Declines

According to the CBO’s projections, housing starts will remain robust through the end of the current decade, driven by the pent-up demand for more living space post-pandemic and the sustained household formation by new immigrants. The report anticipates an average of 1.6 million housing starts per year over the next decade. However, as the 2030s and 2040s approach, a notable decline is expected, with housing starts averaging 1.1 million per year from 2034 to 2043 and 0.8 million per year from 2044 to 2053. This decline is attributed to a slowdown in population growth, an aging demographic, and a return of immigration levels to historical norms.

Key Factors Influencing Housing Starts

The report identifies several factors that could lead to variations in housing starts compared to the projections. Changes in net immigration, for instance, could significantly alter outcomes over the 30-year period. Additionally, financial conditions such as mortgage rates and lending standards play a crucial role in determining the number of housing starts in any given year.

The Demographic Shift

The CBO’s analysis emphasizes the significance of demographic changes in shaping the housing market. As the population ages, the number of deaths rises, slowing the growth of the adult population. By the 2040s, net immigration is projected to contribute almost as much to the demand for new housing as domestic population growth, marking a significant shift from past trends.

Economic Implications

Housing construction is a vital component of the U.S. economy, accounting for over 2% of the gross domestic product (GDP). The CBO projects that the contribution of housing starts to GDP will decline as housing starts decrease in the coming decades. This decline may be partially offset by increased residential improvements, as households choose to upgrade existing homes rather than purchase new ones.

Uncertainty and Future Projections

Despite the detailed projections, the CBO acknowledges significant uncertainty in the forecast of housing starts. Financial and cyclical conditions, demographic factors, and changes in headship rates contribute to this uncertainty. The report also explores alternative scenarios, such as differing rates of net immigration and life expectancy, to illustrate the potential variability in housing starts.

For a deeper dive into the methods used for these projections and the potential implications for the economy, readers can access the full report at CBO’s official website. The analysis provides valuable insights for policymakers, economists, and stakeholders in the housing industry as they navigate the evolving landscape of U.S. housing starts.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

The title insurance industry is entering 2026 with a renewed focus on technology, operational efficiency, and stronger agent support after years of volatility. Leaders from major underwriters report rising transaction activity, improved affordability, and a surge in automation and fraud‑prevention tools—signs that smarter systems and better training will define the next wave of growth.

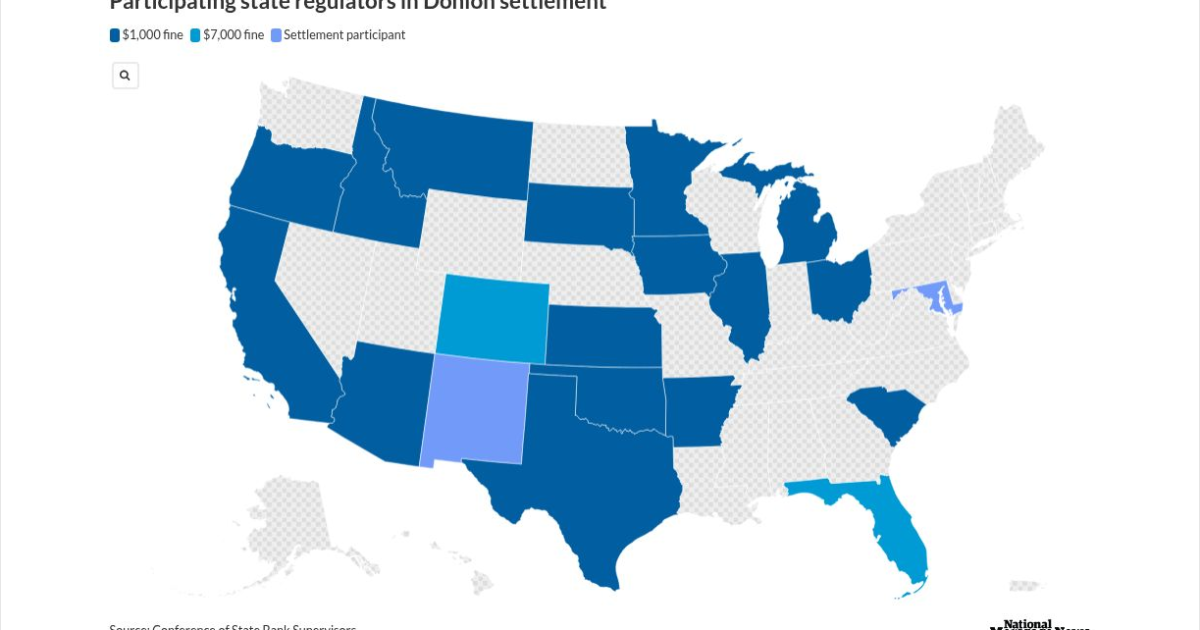

A multistate crackdown has sent shockwaves through the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, accepted a sweeping settlement that bans him from working as a mortgage loan originator in 21 states—19 of them permanently. Regulators say Donlon had another individual complete his mandatory licensing and continuing‑education courses, a violation that triggered a coordinated investigation and a $31,000 penalty. The case underscores regulators’ growing intolerance for education fraud and serves as a sharp reminder to industry professionals: cutting corners on licensing can end careers.

Florida’s once‑booming housing market is cooling fast as rising insurance premiums, increasing foreclosures, and expanding flood zones push buyers to back out of deals and force sellers to cut prices. With insurance now adding thousands to annual housing costs, professionals across real estate, mortgage, and insurance are navigating a dramatically shifting landscape that’s redefining affordability in the Sunshine State.

Florida begins 2026 with a wave of more than 250 new laws now in effect, impacting healthcare, insurance, real estate, and consumer protections statewide. From free breast cancer screenings for state employees to tighter pet insurance regulations, mandatory healthcare refund rules, enhanced animal‑cruelty penalties, and new condo‑management requirements, these updates carry major implications for professionals navigating Florida’s evolving regulatory landscape.

Florida’s barrier islands may offer postcard-perfect beaches and soaring real estate demand, but they’re also some of the most fragile and costly places to build in the United States. With 765,000 residents living on land that shifts, sinks, and takes the brunt of every major hurricane, the financial and insurance risks are accelerating fast. From billion‑dollar beach rebuilds to towers settling into the sand, today’s coastal development challenges are reshaping conversations around property values, disclosure, and long‑term resilience. For real estate professionals, understanding these risks isn’t just smart — it’s becoming essential.

A Cedar City development is turning heads with its fresh approach to affordability. The team behind Temple View Commons is delivering luxury‑inspired twin homes at prices below the local median by using a small, hands‑on staff and cutting traditional costs like realtor commissions. In a tight Utah housing market where inventory is scarce and prices remain high, their strategy offers a realistic path to homeownership without sacrificing high‑end finishes.

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}