In recent years, the rise of Decentralised Finance (DeFi) has signaled a seismic shift in the financial landscape, leveraging blockchain technology to disrupt traditional financial systems. This innovative approach offers financial services without intermediaries, bringing unprecedented levels of transparency, accessibility, and efficiency to the sector.

Opportunities Unlocked by DeFi

DeFi is poised to revolutionize financial inclusion by extending services to those previously excluded from traditional banking systems. By eliminating identification and geographical barriers, DeFi empowers individuals in underserved regions to engage in saving, borrowing, and investing.

Moreover, DeFi’s peer-to-peer model removes the need for centralized intermediaries, significantly reducing fees and enhancing efficiency. The transparency inherent in blockchain technology allows for open auditing of all transactions, reducing opportunities for fraud and corruption.

DeFi also introduces programmability and automation through smart contracts, paving the way for innovative financial instruments such as Automated Market Makers (AMMs), yield farming, and decentralized insurance.

Challenges on the Horizon

Despite its potential, DeFi faces substantial challenges, primarily in the areas of regulation, security, and scalability. The decentralized and borderless nature of DeFi complicates regulatory oversight, necessitating a delicate balance to protect consumers while fostering innovation.

Security remains a critical concern, as the open and complex nature of smart contracts makes the ecosystem vulnerable to hacks. Additionally, as DeFi adoption grows, there is an urgent need for more advanced infrastructure to support increased transaction volumes.

The user experience also presents a hurdle, with current platforms being anything but user-friendly for the average individual. Enhancements in user interface and experience are crucial for broader DeFi adoption.

DeFi’s Disruptive Promise

DeFi platforms are already challenging traditional banking models by enabling direct lending and borrowing without intermediaries. This shift is particularly impactful in developing markets, where traditional institutions may be less prevalent.

Furthermore, stablecoins are transforming payments and remittances, offering faster and more cost-effective cross-border transactions compared to conventional banking systems. DeFi also introduces decentralized insurance platforms, providing new methods for risk management without reliance on traditional insurers.

As highlighted in a recent FinTech Futures article, the rise of DeFi marks the beginning of a fundamental shift in our interaction with financial systems. While the challenges are formidable, the opportunities for financial inclusion, efficiency, and innovation are immense.

About the Author

Hesham Zreik, a renowned investor and entrepreneur, was recognized by Forbes in 2018 as one of the top 50 investors. With investments in over 100 startups and co-founding more than 40, Zreik is the founder and CEO of FasterCapital, an online incubator that supports startups in raising capital.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

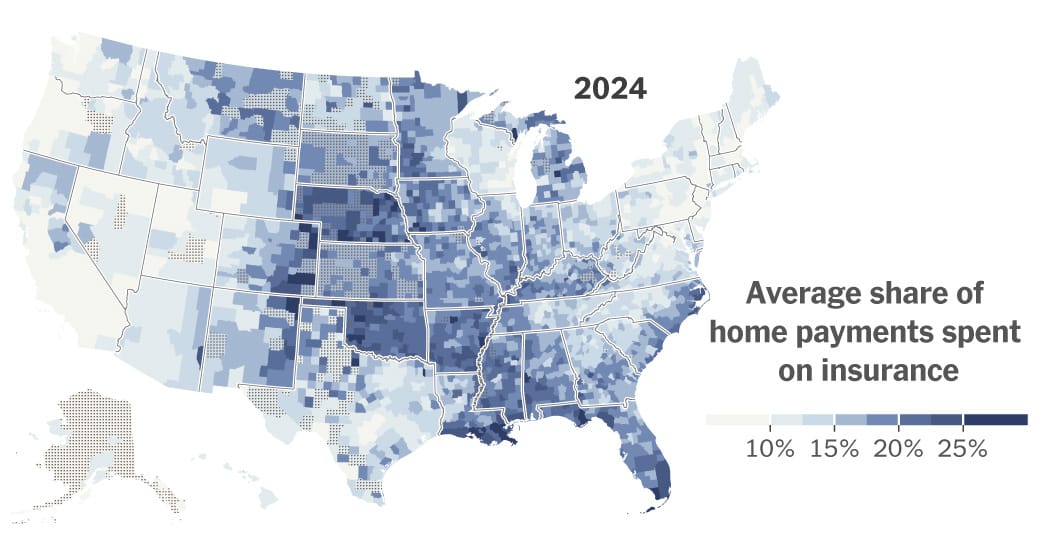

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}