The Rising Cost of Disaster: How Insurance Pressures Are Reshaping Florida’s Middle Class and Housing Market

Across Southwest Florida, a quiet but powerful economic shift is unfolding. Three years after Hurricane Ian struck Fort Myers Beach, the region is still buzzing with construction — yet longtime residents say the Florida they knew is slipping away. As insurance rates skyrocket and rebuilding costs soar, many middle-class families are finding that the struggle to stay rooted has become harder than ever.

The Aftermath of Ian: A Town Forever Changed

Fort Myers Beach still echoes with the sounds of jackhammers and construction trucks. For many residents and business owners, the storm’s impact went far beyond physical damage. The loss of countless mom-and-pop hotels, the disappearance of affordable housing, and the pressure to rebuild under tougher structural standards have all shifted the island’s identity.

As new, hurricane-resistant homes rise, they come with higher price tags. And with those price tags come new demographics — often wealthier, often from out of state — leaving longtime residents questioning whether they still belong in the place they once called home.

Insurance: The Pressure Point Breaking Budgets

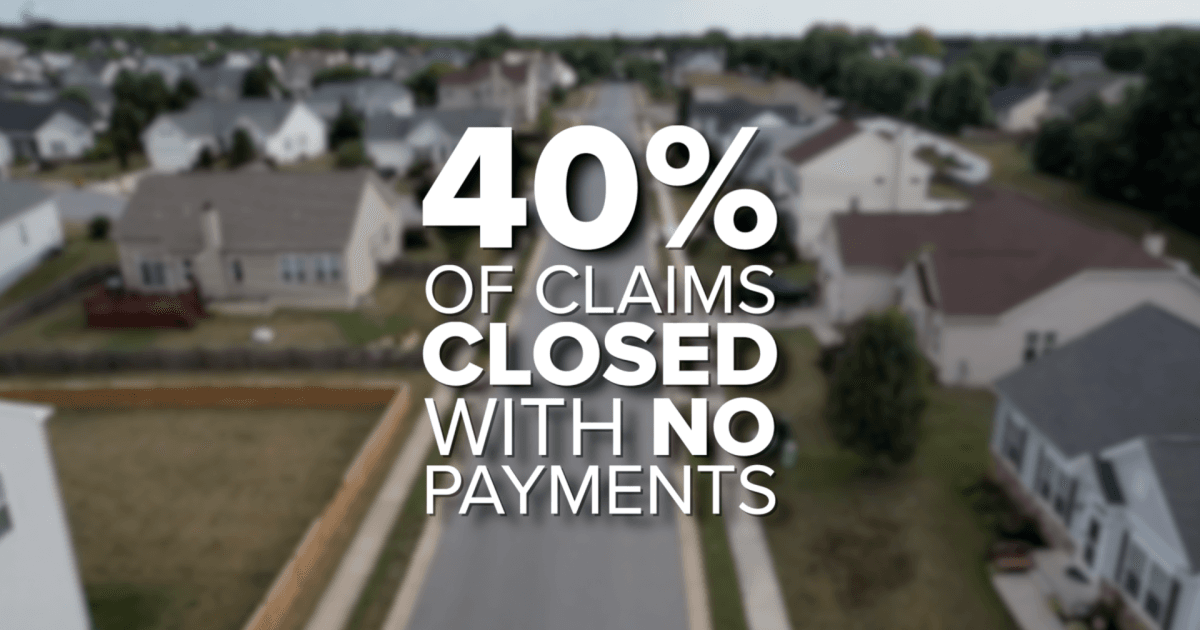

Insurance, once a manageable line item in a homeowner’s budget, has ballooned into a financial burden for many Floridians. With average premiums surpassing $5,700 a year — far above the national average — homeowners face a stark choice: pay, adapt, or move.

Realtors across Lee County report that insurance is driving deals, delaying closings, and in some cases leading homeowners to sell altogether. Even inland areas, once considered safe havens from storm surge, have seen rising flood and home insurance rates that push families to the brink.

Did You Know? In some neighborhoods, the cost of flood insurance has doubled. Many homeowners now pay over $10,000 a year for combined flood and homeowners coverage.

A Growing Threat of Foreclosures

With home values declining and insurance bills rising, many middle-class families are walking a financial tightrope. Realtors warn that if the economy tightens further, the region may see a wave of foreclosures that echo the aftermath of past economic downturns.

The stress is not evenly distributed. Renters, too, are feeling the pressure as landlords pass rising insurance costs onto tenants. Many who moved to Southwest Florida seeking affordability now say they’re reconsidering whether they can stay.

The Bigger Picture: A National Trend With Local Consequences

Although Florida stands at the center of this crisis, insurance premiums are rising across the country due to climate-driven disasters. Wildfires, floods, storms, and hurricanes all contribute to higher risk — and higher rates. But with such a large share of Florida’s population living in coastal zones, the Sunshine State is feeling the impact more intensely than most.

Economists warn that falling home values could reduce property tax revenues, threatening the fiscal stability of many local governments. For cities rebuilding after major storms, this presents a long-term challenge that will shape development for years to come.

Where Professionals Go From Here

For real estate agents, mortgage brokers, insurance specialists, and financial professionals, this evolving landscape requires a deeper understanding of risk, regulation, and consumer education. Homebuyers need guidance. Sellers need options. Renters need clarity. And every professional in the field needs to stay ahead of a rapidly changing market.

Florida’s real estate environment isn’t disappearing — but it is transforming. Those who thrive will be the ones prepared for new rules, new expectations, and a new type of client.

Professional Insight: If you’re working in Florida real estate, mortgage lending, insurance, or property management, now is the time to sharpen your expertise. Cameron Academy offers licensing and continuing education programs to help professionals stay informed and competitive in an unpredictable market.

Still, a Sense of Hope Remains

Even amid the challenges, many residents, business owners, and local leaders believe in Fort Myers Beach’s future. New businesses are opening. New homes are rising. Tourists still gather along the shore to watch the sun dip into the Gulf. But uncertainty lingers, and the next storm season is never far away.

As the area continues to rebuild, the coming years will determine whether this iconic coastal community becomes too expensive for its historic middle-class residents — or whether Florida can find a way to balance resilience with affordability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}