In an era where financial security and legal protection are paramount, landlords are increasingly turning to Limited Liability Companies (LLCs) as a strategic move for managing rental properties. The decision to form an LLC can offer significant tax benefits and enhanced liability protection, making it a compelling choice for property owners.

According to a recent article by Avail Landlord Software, forming an LLC for rental properties is not just about shielding personal assets; it’s about optimizing business operations and leveraging tax advantages.

Why Consider an LLC for Your Rental Property?

The primary allure of an LLC lies in its ability to limit personal liability. If a lawsuit arises, only the assets owned by the LLC are at risk, not the owner’s personal finances. Additionally, LLCs allow for pass-through taxation, meaning income is reported on personal tax returns, potentially reducing the overall tax burden.

Setting Up Your LLC

Forming an LLC involves several steps, including choosing a unique name, filing Articles of Organization, and obtaining an Employer Identification Number (EIN). It’s crucial to open a separate bank account for the LLC to maintain clear financial records.

Once established, landlords should transfer the property title to the LLC, update insurance policies, and ensure all lease agreements are signed under the LLC’s name. This process not only simplifies accounting but also ensures compliance with state regulations.

Tax Advantages and Compliance

LLCs offer a range of tax benefits, such as deductions for mortgage interest, property taxes, and maintenance costs. However, it’s essential to stay informed about state-specific taxes and fees. Starting in 2024, landlords must comply with the Beneficial Ownership Information (BOI) reporting requirements, a move towards greater transparency in business operations.

Best Practices for Managing Your LLC

Successful management of an LLC involves keeping rigorous financial records, regularly reviewing operating agreements, and obtaining adequate insurance. Consulting with tax professionals is advisable to maximize tax benefits and ensure compliance with IRS regulations.

Who Should Form an LLC?

While any landlord can benefit from an LLC, it’s particularly advantageous for those with multiple properties or multiple owners. The operating agreement helps define rights and responsibilities, facilitating smooth property management.

For more detailed guidance, consider consulting resources like Rocket Lawyer or a certified tax professional.

Conclusion

Ultimately, forming an LLC for your rental property is a strategic decision that can offer substantial legal and financial benefits. By understanding the process and potential pitfalls, landlords can make informed choices that align with their business goals.

For more insights and detailed steps on forming an LLC, refer to the original article on Avail’s website.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

The title insurance industry is entering 2026 with a renewed focus on technology, operational efficiency, and stronger agent support after years of volatility. Leaders from major underwriters report rising transaction activity, improved affordability, and a surge in automation and fraud‑prevention tools—signs that smarter systems and better training will define the next wave of growth.

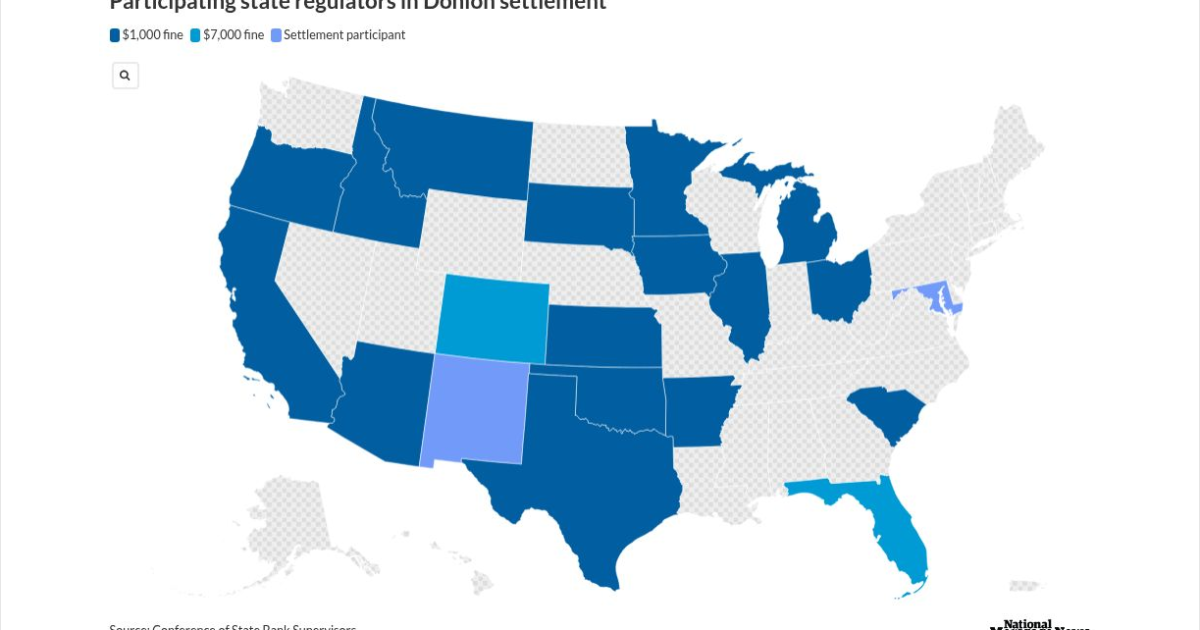

A multistate crackdown has sent shockwaves through the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, accepted a sweeping settlement that bans him from working as a mortgage loan originator in 21 states—19 of them permanently. Regulators say Donlon had another individual complete his mandatory licensing and continuing‑education courses, a violation that triggered a coordinated investigation and a $31,000 penalty. The case underscores regulators’ growing intolerance for education fraud and serves as a sharp reminder to industry professionals: cutting corners on licensing can end careers.

Florida’s once‑booming housing market is cooling fast as rising insurance premiums, increasing foreclosures, and expanding flood zones push buyers to back out of deals and force sellers to cut prices. With insurance now adding thousands to annual housing costs, professionals across real estate, mortgage, and insurance are navigating a dramatically shifting landscape that’s redefining affordability in the Sunshine State.

Florida begins 2026 with a wave of more than 250 new laws now in effect, impacting healthcare, insurance, real estate, and consumer protections statewide. From free breast cancer screenings for state employees to tighter pet insurance regulations, mandatory healthcare refund rules, enhanced animal‑cruelty penalties, and new condo‑management requirements, these updates carry major implications for professionals navigating Florida’s evolving regulatory landscape.

Florida’s barrier islands may offer postcard-perfect beaches and soaring real estate demand, but they’re also some of the most fragile and costly places to build in the United States. With 765,000 residents living on land that shifts, sinks, and takes the brunt of every major hurricane, the financial and insurance risks are accelerating fast. From billion‑dollar beach rebuilds to towers settling into the sand, today’s coastal development challenges are reshaping conversations around property values, disclosure, and long‑term resilience. For real estate professionals, understanding these risks isn’t just smart — it’s becoming essential.

A Cedar City development is turning heads with its fresh approach to affordability. The team behind Temple View Commons is delivering luxury‑inspired twin homes at prices below the local median by using a small, hands‑on staff and cutting traditional costs like realtor commissions. In a tight Utah housing market where inventory is scarce and prices remain high, their strategy offers a realistic path to homeownership without sacrificing high‑end finishes.

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}