Trump Predicts Major Mortgage Rate Drop in 2026: What It Really Means for Homebuyers and Professionals

Your morning coffee just got a big splash of real estate intrigue. During a recent White House speech, President Trump declared that mortgage rates will fall “a lot lower” by early 2026 — a bold prediction that instantly sparked conversation among buyers, sellers, agents, lenders, and economic analysts nationwide.

The original report — published by The Truth About Mortgage — dives into the meaning behind the president’s comments and whether current data supports the optimism. According to the source, Trump pointed out that the annual cost of a typical new mortgage rose $15,000 under Democratic leadership, but has dropped by about $3,000 since he returned to office. He hinted that rates will continue falling, teasing “shocking” numbers on the horizon.

Are Mortgage Rates Really Dropping This Fast?

The current 30‑year fixed mortgage rate sits around 6.25%, down from roughly 7.25% earlier this year. That’s solid movement — though not quite “shocking.” For the dramatic drop Trump suggests to become reality, the economy would likely need to show signs of cooling: slower job growth, higher unemployment, or inflation dipping sharply.

Mortgage rates rarely fall without underlying catalysts. Typically, major declines follow:

Weak or softening economic indicators

Improving inflation trends

Narrower spreads between mortgage‑backed securities and Treasuries

Increased MBS purchasing from agencies like Fannie Mae and Freddie Mac

Interestingly, The Truth About Mortgage highlights that while none of these conditions guarantee a rapid drop, they could align in 2026, especially as markets respond to upcoming policy shifts.

A New Fed Chair Could Shake Things Up

Trump also vowed to install a Federal Reserve chair who “believes in lower interest rates by a lot.” Although this made headlines, it’s important to understand the distinction: the Fed does not directly control long‑term mortgage rates. They influence short‑term borrowing costs, but mortgages track long‑term bond yields.

Still, expectations around the Fed heavily influence the bond market. If economic conditions justify lower yields, mortgage rates can follow — but the underlying data must support such movement. Policy alone can’t force rates down.

So… Should Real Estate and Mortgage Pros Prepare?

Here’s the encouraging news: independent forecasts already project mortgage rates drifting into the mid‑5% range by 2026, even without dramatic political intervention. That’s a far more favorable environment for buyers, sellers, lenders, and agents alike.

For real estate agents — especially those navigating Florida’s fast‑changing markets — staying informed about rate cycles is a strategic advantage. Understanding how rate movements shape buyer urgency and affordability can dramatically elevate your performance and value to clients.

And if you’re earning your license, advancing your skills, or knocking out CE credits, Cameron Academy remains a trusted partner for real estate, mortgage, and professional licensing education across all 50 states — helping you stay ahead no matter which direction rates swing.

Read the Full Original Breakdown

Ready to explore the deeper economic context and Trump’s full remarks? Visit the original article by The Truth About Mortgage:

Read the full story here.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

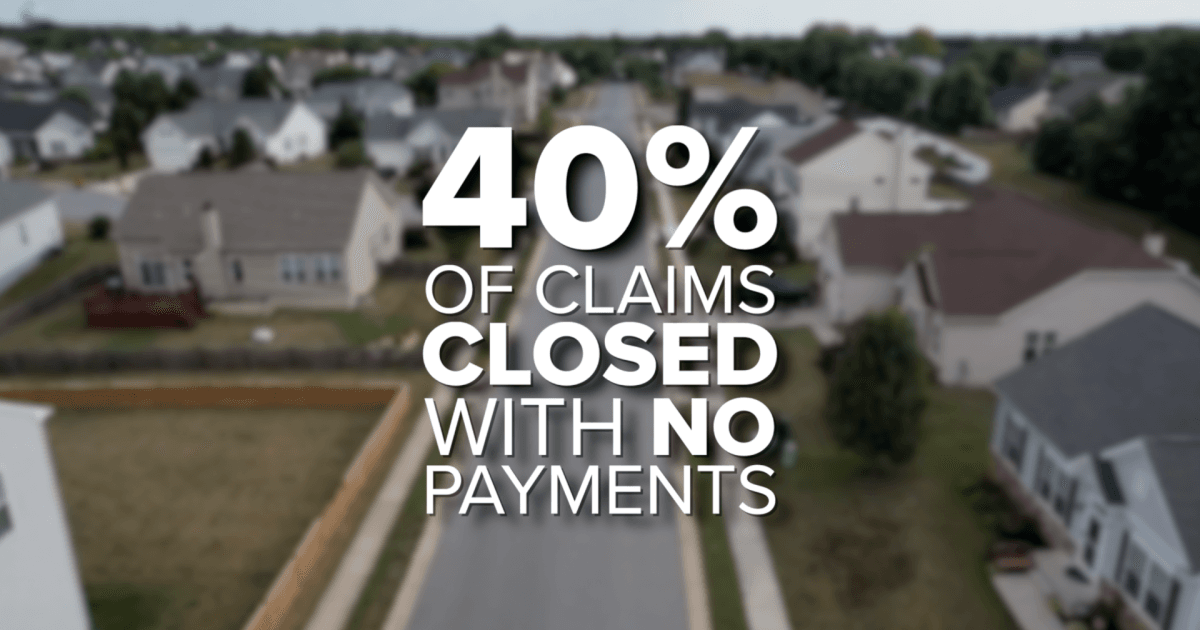

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}