Virtual Care in 2024: Challenges and Opportunities for Telehealth

The telehealth market is experiencing a remarkable surge, driven by the increasing adoption of digital health solutions and remote care services. As reported by PharmiWeb.com, the market was valued at USD 91.4 billion in 2023 and is projected to soar to USD 789.7 billion by 2032, with a compound annual growth rate (CAGR) of 27.4%. This growth highlights telehealth’s transformative role in enhancing healthcare delivery, promising improved accessibility, efficiency, and cost-effectiveness.

Several key drivers are propelling this expansion. Advancements in digital health platforms, such as mobile health applications and live video consultations, are breaking down geographical barriers, providing unprecedented access to quality healthcare. The increasing demand for remote patient monitoring (RPM) technologies allows for real-time patient data tracking, ensuring proactive healthcare management. Additionally, the rising prevalence of chronic diseases like diabetes and hypertension accentuates the necessity for telehealth solutions. Government initiatives promoting digital healthcare adoption, particularly during the COVID-19 pandemic, have further strengthened the industry.

Moreover, telehealth’s cost-effective nature significantly reduces healthcare expenses for both providers and patients by minimizing the need for in-person visits and optimizing resource allocation.

Telehealth Market Segmentation

The telehealth market is segmented by component (software, services, hardware), mode of delivery (web-based, cloud-based, on-premises), and end-users (healthcare providers, patients, payers). Regionally, North America leads in telehealth adoption due to advanced technology, high healthcare spending, and favorable regulations. However, the Asia-Pacific region is expected to witness rapid growth, driven by increasing smartphone penetration and supportive governmental policies.

Challenges and Innovations

Despite the positive outlook, the industry faces challenges, notably data privacy and security concerns, infrastructure limitations in developing regions, and regulatory hurdles for cross-border healthcare services. Innovations driving market growth include AI and machine learning for enhanced diagnostics, integration of wearable devices for continuous monitoring, blockchain for secure data management, and AR/VR technologies for immersive healthcare experiences.

The COVID-19 pandemic dramatically accelerated telehealth adoption, acting as a catalyst for virtual healthcare solution uptake—a trend expected to continue post-pandemic as telehealth becomes integral to healthcare systems.

Prominent players in the telehealth market, such as Teladoc Health, American Well, and MDLIVE, are heavily investing in research and development to innovate and bolster their market standing, paving the way for a promising future in telehealth.

For more detailed insights, access the sample report or purchase the full report from Ameco Research.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Skyrocketing insurance premiums and soaring rebuilding costs are transforming communities across Southwest Florida, especially in the wake of Hurricane Ian. As longtime residents struggle to keep up with rising financial pressure, wealthier newcomers and stricter building standards are reshaping the identity of places like Fort Myers Beach. With insurance rates now driving home sales, triggering potential foreclosures, and squeezing both owners and renters, Florida’s middle-class families face a growing question: can they afford to stay in the state they love?

Florida’s insurance industry is stabilizing fast, with nearly 1.6 million policies shifting from Citizens to private insurers and litigation dropping sharply. Regulators report stronger market confidence, decreasing premiums, and renewed competition—signaling one of the healthiest periods the state has seen in years.

A Leon County judge has ordered the restart of arbitration for Citizens Property Insurance claims, directly conflicting with a previous ruling that halted the process as potentially unconstitutional. With more than 400 cases now back in motion, real estate, insurance, and mortgage professionals can expect renewed activity in claim disputes and fresh uncertainty as Florida courts clash over the legality of Citizens’ arbitration system.

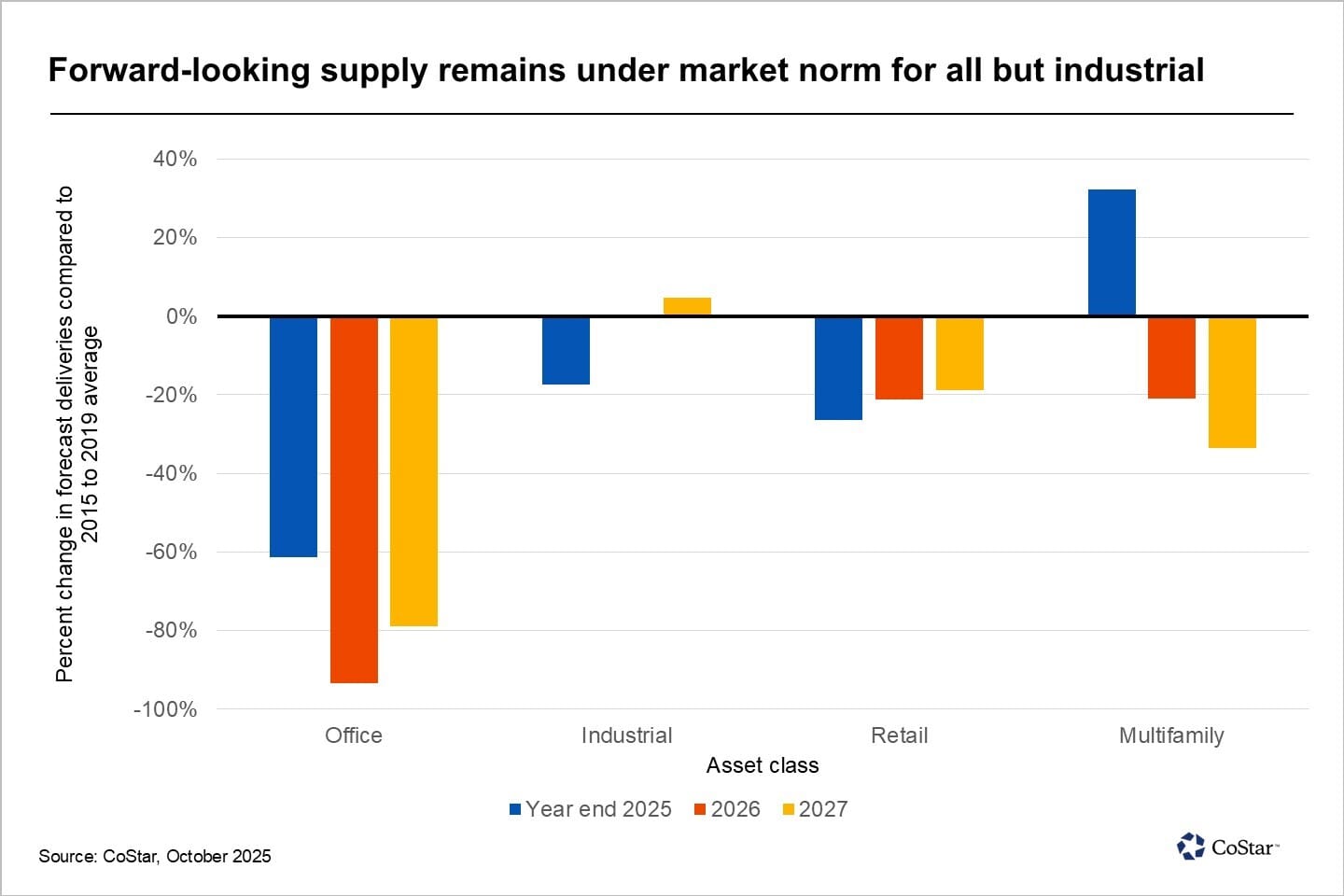

The DFW market is transitioning into a new construction phase marked by a slowdown in office development, a more selective approach to industrial projects, and an evolving housing landscape shaped by affordability and population growth. Developers are recalibrating their priorities, and for real estate professionals, understanding these shifts offers a critical edge in navigating—and capitalizing on—the next phase of the metroplex’s growth.

A new federal lawsuit claims Zillow pushed homebuyers toward Zillow Home Loans by rewarding affiliated agents with valuable leads — all without proper disclosure. The suit alleges undisclosed incentives, referral quotas, and potential RESPA violations, raising major concerns about steering, fiduciary duties, and Zillow’s expanding mortgage ambitions.

The mortgage industry is evolving fast, and the lenders who come out on top will be those who innovate without uprooting what already works. By building on strong technology foundations, streamlining workflows and adopting smart automation, lenders can reduce costs, improve customer experience and stay resilient in any market cycle. This article breaks down why innovation matters now, how a stable tech ecosystem protects lenders in volatile conditions and why small, strategic steps can drive long-term transformation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}