Zillow Removes Climate Risk Scores: A Win for Sales or a Loss for Transparency?

The real estate world has a new storm swirling around it—and this time, it has nothing to do with hurricanes or wildfires. Zillow, the largest real estate listing platform in the United States, has quietly removed its climate‑risk scoring feature after months of pushback from real estate agents, homeowners, and listing services who argued the scores were hurting sales.

The tool, originally launched for over 1 million properties, provided estimated risks for wildfire, flooding, extreme heat, wind, and poor air quality. For many homebuyers, it served as a wake-up call. For many sellers? A headache. And for agents? A deal‑breaker.

Why Did Zillow Pull the Plug?

According to reporting from The Guardian, complaints poured in from agents and homeowners who felt the scores were arbitrary or unchallengeable—and worse, that they were tanking offers before buyers even stepped through the front door. Even the California Regional Multiple Listing Service, a major data provider for Zillow, pushed back.

No climate scores, no friction—or so the thinking goes.

Zillow’s official stance? They claim they’re still committed to informed decision‑making, directing users instead to First Street, the nonprofit that originally supplied the data.

“Flying Blind”: First Street Fires Back

Matthew Eby, First Street’s CEO, didn’t sugarcoat his reaction. He warned that removing climate‑risk data from listings means many families will be “flying blind” in an era of intensifying weather disasters.

“The risk doesn’t go away; it just moves from a pre‑purchase decision into a post‑purchase liability,” Eby said. Flooded basements, unaffordable wildfire insurance, surprise premium hikes—these are the kinds of discoveries no homeowner wants after signing a mortgage.

Eby’s message is clear: We are not eliminating climate risk. We are merely sweeping it under a slightly pricier rug.

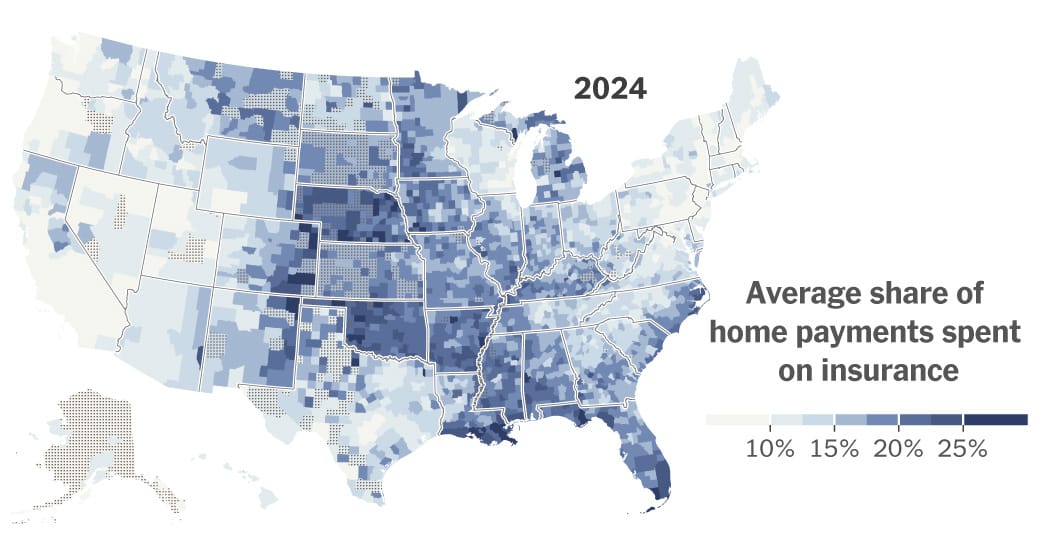

The Market Is Hot—But the Planet Is Hotter

As extreme weather worsens, the financial impacts are becoming harder to ignore. Last year alone, climate‑amplified disasters caused an estimated $182 billion in damages. At the same time, home insurance is becoming more expensive—or downright unavailable—in parts of the country, especially places like California and Florida.

Yet ironically, Americans continue moving in droves toward these high‑risk regions. Florida, with its hurricanes, heatwaves, and soaring insurance rates, remains one of the most in‑demand destinations. And luxury listings aren’t immune: A Florida mansion with a $295 million price tag, one of the most expensive in history, sat unsold and was eventually pulled from the market—its severe flood risk noted by several analysts.

Experts Say the Problem Isn’t Just the Data

Some climate experts, such as Tulane University’s Jesse Keenan, argue that hyper‑granular property‑level climate assessments can be inaccurate. Proprietary models, he warns, can sow distrust if they appear inconsistent.

But even Keenan doesn’t believe the industry is trying to hide climate information—only that the tools still need refinement and federal standardization.

Meanwhile, First Street maintains its science is strong, peer‑reviewed, and validated in real‑world scenarios. Eby puts it bluntly: when critics say the models are flawed, “we ask for evidence.” So far, he says, the data holds up.

What This Means for Real Estate Professionals

For agents, brokers, and aspiring professionals, this story lands at the intersection of ethics, economics, and education. Climate literacy is becoming an essential skill—not an optional one. Whether or not Zillow displays a score, buyers are asking smarter questions, insurers are setting tighter limits, and regulators are reconsidering disclosure standards.

And for anyone entering or advancing in a real estate career, this trend highlights why staying educated is no longer just an advantage—it’s a necessity.

That’s where institutions like Cameron Academy come in. By helping professionals understand not just contracts and closings, but also emerging market pressures—from insurance volatility to climate‑risk assessment—education becomes your best competitive edge.

A Changing Market Calls for Informed Professionals

Zillow may have removed the scores, but the climate conversation isn’t going anywhere. Whether you’re a seasoned agent in Miami, a new broker in Phoenix, or a property investor tracking shifting risk maps, understanding the forces reshaping the industry is part of staying ahead.

Because in real estate, as in weather forecasting, the one thing we can count on is change.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}