Exploring Innovative Strategies for Managing Student Loan Payments

In a landscape where student loan debt is a growing concern, borrowers are exploring creative methods to manage their financial obligations. According to EducationData.org’s 2023 report, the average federal student loan borrower owes $37,574, while private borrowers face an even steeper average of $54,921. With these daunting figures, many are considering unconventional methods to ease their financial burden.

Contact Your Lender

For those with private loans, reaching out to your lender can reveal whether credit card payments are an option. While not all lenders offer this flexibility, some do, providing a possible avenue for managing payments more conveniently.

Utilize Third-Party Payment Platforms

Federal student loan borrowers might consider third-party platforms like PaySimply and Plastiq. These services enable payments via credit card by converting them into wire transfers or cash equivalents, although fees ranging from 2.5% to 3% can offset any potential rewards benefits.

Consider a Balance Transfer

For those nearing the end of their loan term, transferring the balance to a 0% APR balance transfer credit card could be a viable option. This method can provide an interest-free period of up to 21 months, though it comes with a transfer fee of 2% to 3%.

Creative Budgeting

A strategic approach involves reallocating expenses. For example, paying for groceries with a credit card can free up cash for student loan payments, achieving the same financial effect without direct loan charges.

Cash Advances

While not ideal due to high APR rates and immediate interest accrual, cash advances can be a last-resort option. Borrowers should weigh the costs carefully before proceeding.

Explore Deferment and Forbearance

Federal loan holders should explore deferment and forbearance options, which offer payment relief without credit damage. Private lenders may also provide hardship plans, though these vary by institution.

While these strategies can provide temporary relief, borrowers must remain vigilant about the potential pitfalls, such as high interest rates and the risk of accumulating more debt. The original article by Erica Sandberg on CardRates.com emphasizes the importance of informed financial decisions and responsible credit management.

CSS for Styling

“`css

h3 {

color: #b40101;

margin-bottom: 20px;

}

h4 {

color: #b40101;

margin-top: 30px;

margin-bottom: 10px;

}

p {

margin-bottom: 15px;

}

b {

color: #b40101;

}

a {

color: #b40101;

text-decoration: none;

}

a:hover {

text-decoration: underline;

}

img {

margin: 20px 0;

max-width: 100%;

height: auto;

}

“`

This approach ensures that borrowers are equipped with the knowledge to navigate their financial landscape effectively, prioritizing both short-term relief and long-term financial health.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

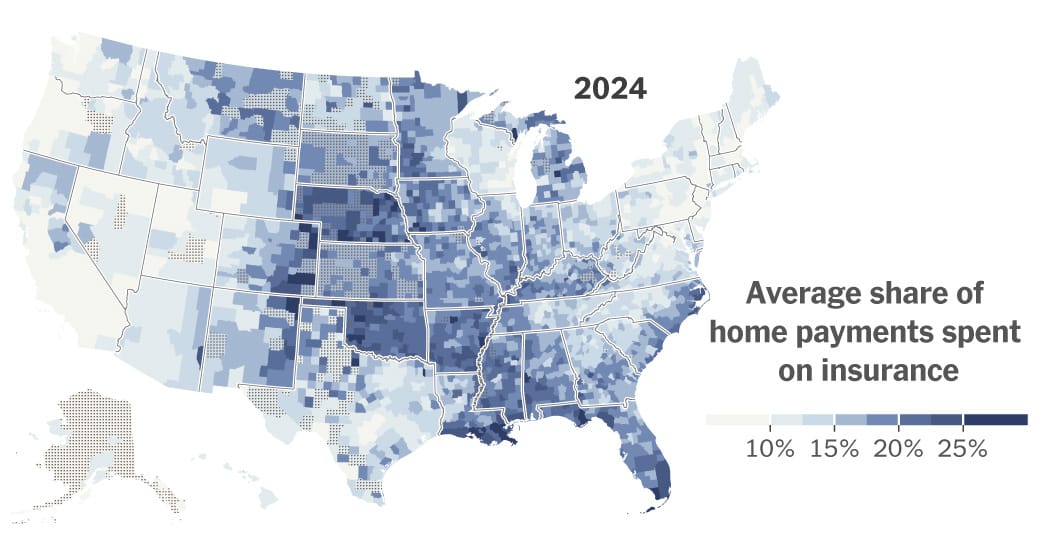

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

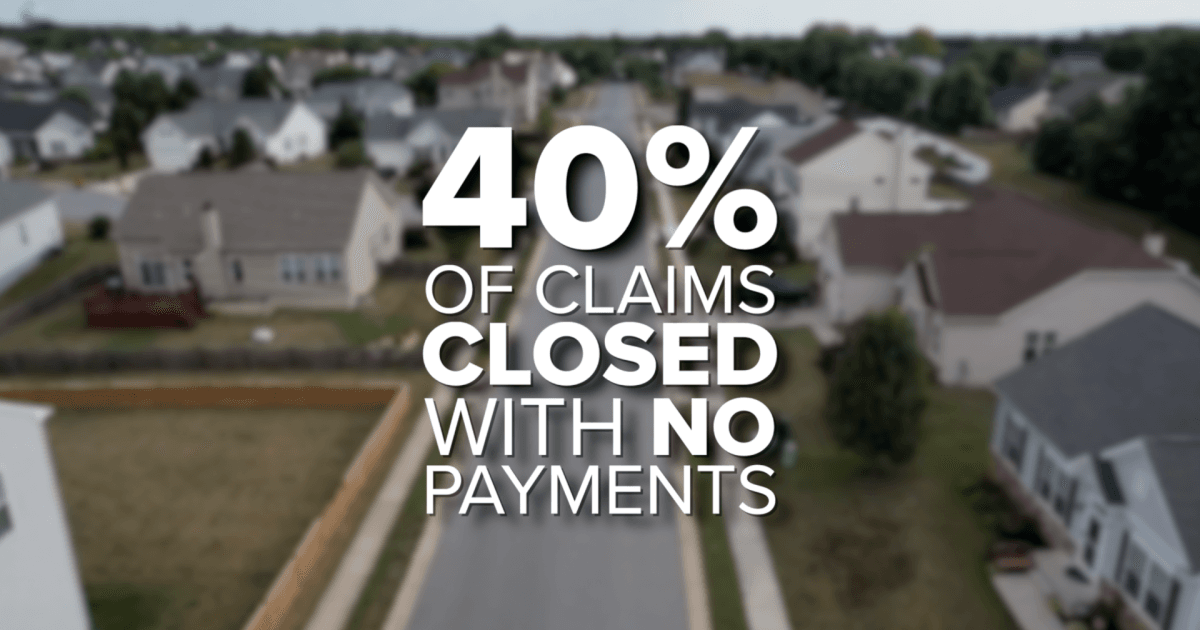

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}