Exploring Innovative Strategies for Managing Student Loan Payments

In a landscape where student loan debt is a growing concern, borrowers are exploring creative methods to manage their financial obligations. According to EducationData.org’s 2023 report, the average federal student loan borrower owes $37,574, while private borrowers face an even steeper average of $54,921. With these daunting figures, many are considering unconventional methods to ease their financial burden.

Contact Your Lender

For those with private loans, reaching out to your lender can reveal whether credit card payments are an option. While not all lenders offer this flexibility, some do, providing a possible avenue for managing payments more conveniently.

Utilize Third-Party Payment Platforms

Federal student loan borrowers might consider third-party platforms like PaySimply and Plastiq. These services enable payments via credit card by converting them into wire transfers or cash equivalents, although fees ranging from 2.5% to 3% can offset any potential rewards benefits.

Consider a Balance Transfer

For those nearing the end of their loan term, transferring the balance to a 0% APR balance transfer credit card could be a viable option. This method can provide an interest-free period of up to 21 months, though it comes with a transfer fee of 2% to 3%.

Creative Budgeting

A strategic approach involves reallocating expenses. For example, paying for groceries with a credit card can free up cash for student loan payments, achieving the same financial effect without direct loan charges.

Cash Advances

While not ideal due to high APR rates and immediate interest accrual, cash advances can be a last-resort option. Borrowers should weigh the costs carefully before proceeding.

Explore Deferment and Forbearance

Federal loan holders should explore deferment and forbearance options, which offer payment relief without credit damage. Private lenders may also provide hardship plans, though these vary by institution.

While these strategies can provide temporary relief, borrowers must remain vigilant about the potential pitfalls, such as high interest rates and the risk of accumulating more debt. The original article by Erica Sandberg on CardRates.com emphasizes the importance of informed financial decisions and responsible credit management.

CSS for Styling

“`css

h3 {

color: #b40101;

margin-bottom: 20px;

}

h4 {

color: #b40101;

margin-top: 30px;

margin-bottom: 10px;

}

p {

margin-bottom: 15px;

}

b {

color: #b40101;

}

a {

color: #b40101;

text-decoration: none;

}

a:hover {

text-decoration: underline;

}

img {

margin: 20px 0;

max-width: 100%;

height: auto;

}

“`

This approach ensures that borrowers are equipped with the knowledge to navigate their financial landscape effectively, prioritizing both short-term relief and long-term financial health.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

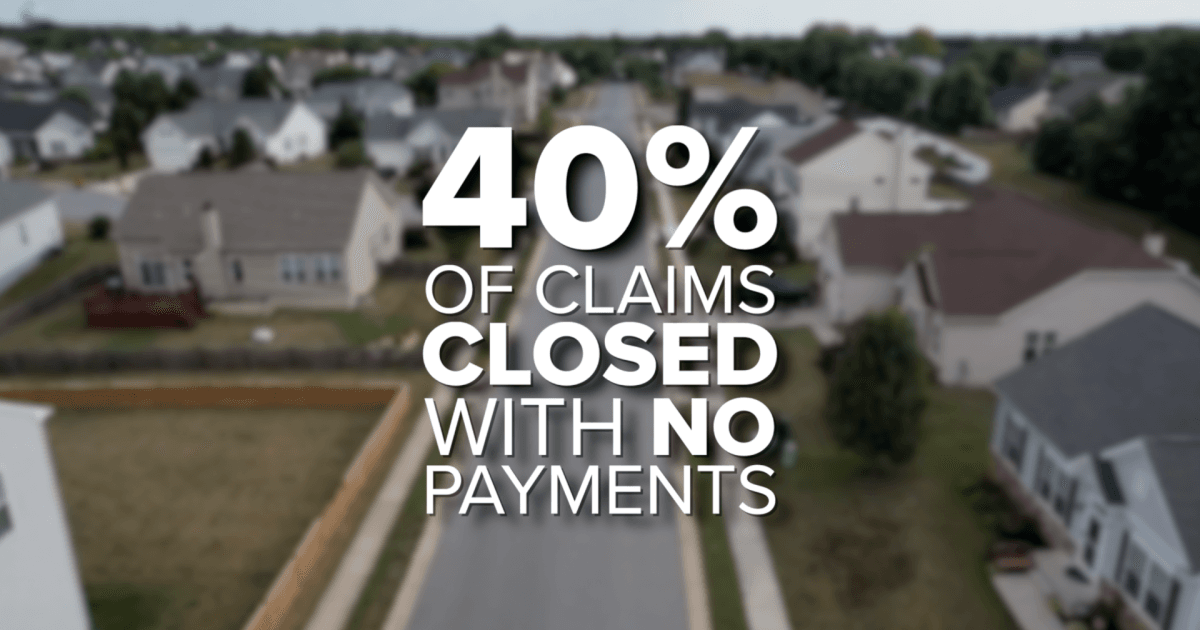

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}