Florida’s Home Insurance Shake-Up: New Names, Old Problems

Florida’s home insurance market has become the state’s most expensive game of déjà vu. Despite bold reforms and confident promises, Floridians are still facing soaring premiums, shrinking coverage options, and mounting uncertainty each hurricane season. A recent deep‑dive by The American Prospect reveals why the “new” insurance landscape feels uncomfortably similar to the one that collapsed after Hurricane Andrew.

Gov. Ron DeSantis’s 2022 reforms were pitched as a stabilizing force after Hurricane Ian, but the evidence suggests they’ve recreated many of the same structural weaknesses that triggered earlier insurer failures—leaving homeowners, real estate professionals, and insurance agents navigating a treacherous landscape of financial risk.

The Depopulation Game and the Return of Risky Insurers

At the heart of the insurance overhaul is the depopulation of Citizens Property Insurance Corporation—the state’s “insurer of last resort.” More than 355,000 homeowners have been shifted from Citizens into private insurers, many of which charge higher premiums and show signs of shaky financial footing.

The market‑friendly reforms Gov. DeSantis passed in the wake of Hurricane Ian have failed to stabilize the state’s insurance market.

The analysis highlights a troubling trend: several newly approved insurance companies have direct connections to firms that previously collapsed. A standout example is Viceroy Preferred Insurance Company, which shares board members with Monarch National—a company fined for mishandled claims and formerly linked to another insurer that ultimately went insolvent.

Slide Insurance, one of Florida’s newest market entrants, closed over half its claims without payment—yet still holds an “A” rating from Demotech, while Weiss assigns it a stark “C‑.” This rating gulf has become too large for industry experts to ignore.

Politics, Profits, and Luxury Homes

The investigation also reveals eyebrow‑raising compensation details. Slide Insurance’s CEO and COO—who are married—took home tens of millions in earnings while residing in a lavish 9,600‑square‑foot waterfront home featured in Tampa Magazine. Meanwhile, Slide ranked among the insurers most likely to deny homeowners’ storm‑related claims.

Add political contributions to high‑profile Florida candidates into the mix, and the picture becomes even more complex.

Calls for Change: A Market Built on Sand

Experts interviewed in the report argue that Florida’s insurance system needs more than surface‑level fixes. They call for unified regulatory oversight, transparent rating standards, and stronger accountability—especially as climate risks intensify year after year.

As one analyst summarized: “We effectively have to build the market from scratch.”

What This Means for Real Estate Professionals

For Florida’s real estate agents, brokers, appraisers, mortgage lenders, property managers, and insurance professionals, understanding this evolving landscape is crucial. Insurance availability and affordability directly influence home sales, property values, and buyer confidence—making awareness a professional necessity.

At Cameron Academy, we continue helping Florida professionals stay ahead of these industry shifts—whether you’re renewing your real estate license, branching into insurance, or entering a new professional field. In a market this volatile, education isn’t optional—it’s your strongest safeguard.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

In 2026, financial advisors are no longer just experimenting with AI — they’re relying on it. Once confined to back-office duties, AI now supports meeting prep, portfolio analysis, and even early-stage financial planning. Advisors say the tech is strengthening client relationships by freeing them from administrative overload, though entry-level roles like paraplanners may feel the squeeze as automation accelerates.

Cybercriminals are weaponizing AI to launch highly convincing email scams and system breaches across the mortgage industry, overwhelming lenders and servicers whose cybersecurity measures can’t keep up. With major companies already hit and regulation lagging behind, experts warn the sector—now considered critical infrastructure—must rapidly upgrade protections, collaborate on threat intelligence, and improve AI governance before the risks escalate further.

Escrow payments are quietly surging across the country as property taxes and insurance premiums spike—pushing many homeowners toward delinquencies and even foreclosure. New data from Cotality shows the sharpest increases hitting the South and Midwest, with Florida among the hardest‑hit states. Even with fixed mortgage rates, rising escrow requirements are driving monthly payments higher and threatening affordability heading into 2026.

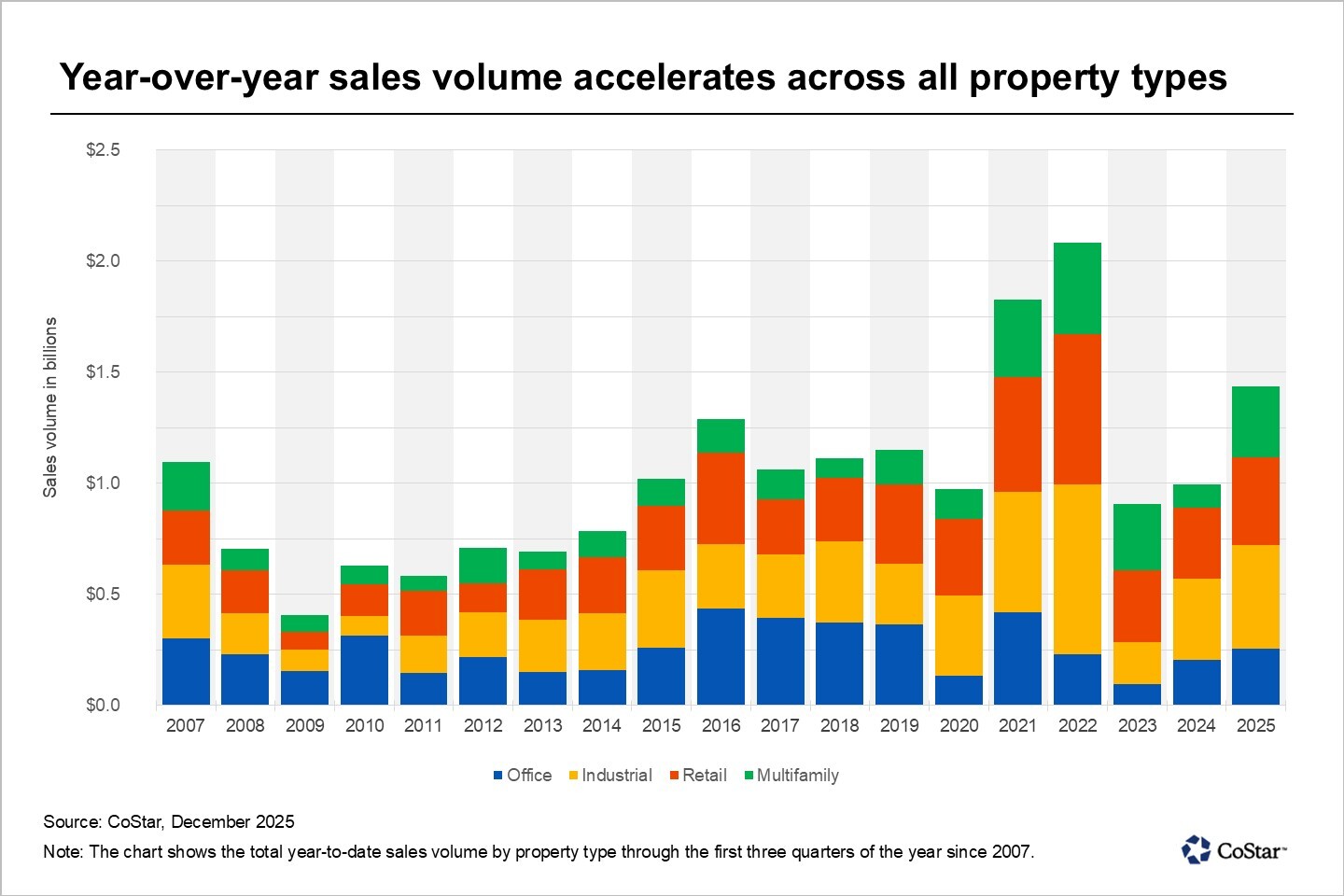

Milwaukee entered 2025 with renewed momentum, posting its strongest commercial real estate sales volume in three years. After a period of uncertainty and high capital costs, investors are returning with a sharper focus on quality assets, realistic pricing, and reliable cash flow. Activity is increasing across industrial, office, multifamily, and retail sectors, signaling a broad-based recovery fueled by stabilizing interest rates and improved market confidence.

As 2026 approaches, the title insurance industry is navigating a complex mix of market recovery, rising fraud threats, and sweeping regulatory changes. Industry leaders say the path forward centers on smarter technology, leaner operations, and stronger support for title agents. With AI-driven workflows, enhanced fraud prevention, and new compliance demands—including FinCEN’s expanded Geographic Targeting Orders—companies like Stewart and First American are reshaping how title work gets done. For real estate and mortgage professionals, the year ahead promises more automation, heightened standards, and major opportunities for those who stay ahead of the curve.

The real estate industry is undergoing a major transformation in 2025 as advancements in AI, proptech, blockchain, and data intelligence redefine how properties are marketed, valued, financed, and experienced. From instant digital valuations and immersive virtual tours to tokenized investments and predictive analytics, technology is reshaping every stage of the real estate lifecycle. Professionals who embrace these innovations—while maintaining the human expertise clients still rely on—will lead the next era of the industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}