Florida’s 3.35% Home Insurance Non‑Renewal Rate: Why Hundreds of Thousands Lost Coverage

Florida’s insurance market has always had a flair for the dramatic, but last year’s numbers took things to a new level. A 3.35% non-renewal rate may sound small, yet in a state with millions of homeowners, it translates to hundreds of thousands suddenly losing their insurance coverage. It’s the kind of statistic that makes any Floridian pause mid‑coffee sip.

For real estate agents, mortgage professionals, insurance licensees, and homeowners, this shift is more than a headline—it’s a reshaping of Florida’s risk profile. And understanding these changes is becoming essential for anyone working around property. If you’re in the industry and need to stay ahead, continuing education through Cameron Academy can help keep your expertise sharp.

When Storm Damage Becomes a Breaking Point

Florida’s storms are practically characters in our yearly storyline—dramatic, recurring, and often costly. Over recent years, however, the financial aftermath has escalated. NAIC data reveals that Florida leads the nation in non-renewals, with insurers stepping back after repeated storm‑related claims.

Insurers aren’t acting on emotion. When storms become more frequent and more destructive, payouts skyrocket. Eventually, companies tighten underwriting standards or withdraw entirely from high‑risk zones. The irony is hard to miss: the same storms that make insurance essential also make it harder to keep.

The Rising Cost of Rebuilding

The weather isn’t the only culprit. Rising construction expenses—driven by labor shortages, material costs, and lingering supply chain issues—mean each claim costs insurers more than it would have just a few years ago.

As construction costs continue climbing, insurers adjust their risk models, premiums shift upward, and coverage criteria tighten. Homeowners feel the effects long before they ever see the spreadsheets causing it all.

The Legal Landscape: Fraud and Litigation

Florida has long been known for its intense volume of insurance-related litigation. While many claims are legitimate, the sheer quantity of lawsuits—some unnecessary—adds immense financial pressure to insurers.

These expenses ripple outward to homeowners as higher premiums or lost coverage. Even with recent reforms meant to cool the market, improvements will take time. Until then, detailed documentation remains a homeowner’s strongest defense.

Insurers Shrinking Their Footprint

One of the most dramatic developments has been the number of insurers reducing—or outright ending—their operations in Florida. When providers leave, competition shrinks, prices rise, and homeowners face fewer options.

Many affected residents turn to Citizens Property Insurance Corporation, the state-backed insurer of last resort. While essential, Citizens was never intended to hold such a large market share. Today, shopping early and comparing multiple carriers is becoming a must-do rather than an option.

Everyday Homeowners Caught in the Middle

Losing insurance coverage isn’t just inconvenient—it can jeopardize mortgages, stall repairs, or create major financial strain. Many homeowners report receiving premium increases double or triple what they previously paid.

Proactive upgrades—modern roofs, wind mitigation improvements, regular maintenance, and detailed documentation—can help maintain good standing with insurers.

What Homeowners Can Do Moving Forward

While homeowners can’t control the weather or underwriting algorithms, they can take steps to stay protected. Start shopping for renewal options early, maintain your property diligently, and stay informed as legislative shifts continue.

For real estate and insurance professionals, knowledge is your currency. If you’re earning or upgrading your license, Cameron Academy offers flexible, affordable programs built to keep you competitive in a changing market.

A Market in Motion

Florida’s 3.35% non-renewal rate isn’t just a statistic—it’s a snapshot of an evolving marketplace shaped by storms, rising costs, legal pressures, and insurer strategies. The professionals who understand these forces will be the ones best positioned to guide homeowners through uncertainty.

What changes have you seen in your own insurance situation? Share your experience below.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

In 2026, financial advisors are no longer just experimenting with AI — they’re relying on it. Once confined to back-office duties, AI now supports meeting prep, portfolio analysis, and even early-stage financial planning. Advisors say the tech is strengthening client relationships by freeing them from administrative overload, though entry-level roles like paraplanners may feel the squeeze as automation accelerates.

Cybercriminals are weaponizing AI to launch highly convincing email scams and system breaches across the mortgage industry, overwhelming lenders and servicers whose cybersecurity measures can’t keep up. With major companies already hit and regulation lagging behind, experts warn the sector—now considered critical infrastructure—must rapidly upgrade protections, collaborate on threat intelligence, and improve AI governance before the risks escalate further.

Escrow payments are quietly surging across the country as property taxes and insurance premiums spike—pushing many homeowners toward delinquencies and even foreclosure. New data from Cotality shows the sharpest increases hitting the South and Midwest, with Florida among the hardest‑hit states. Even with fixed mortgage rates, rising escrow requirements are driving monthly payments higher and threatening affordability heading into 2026.

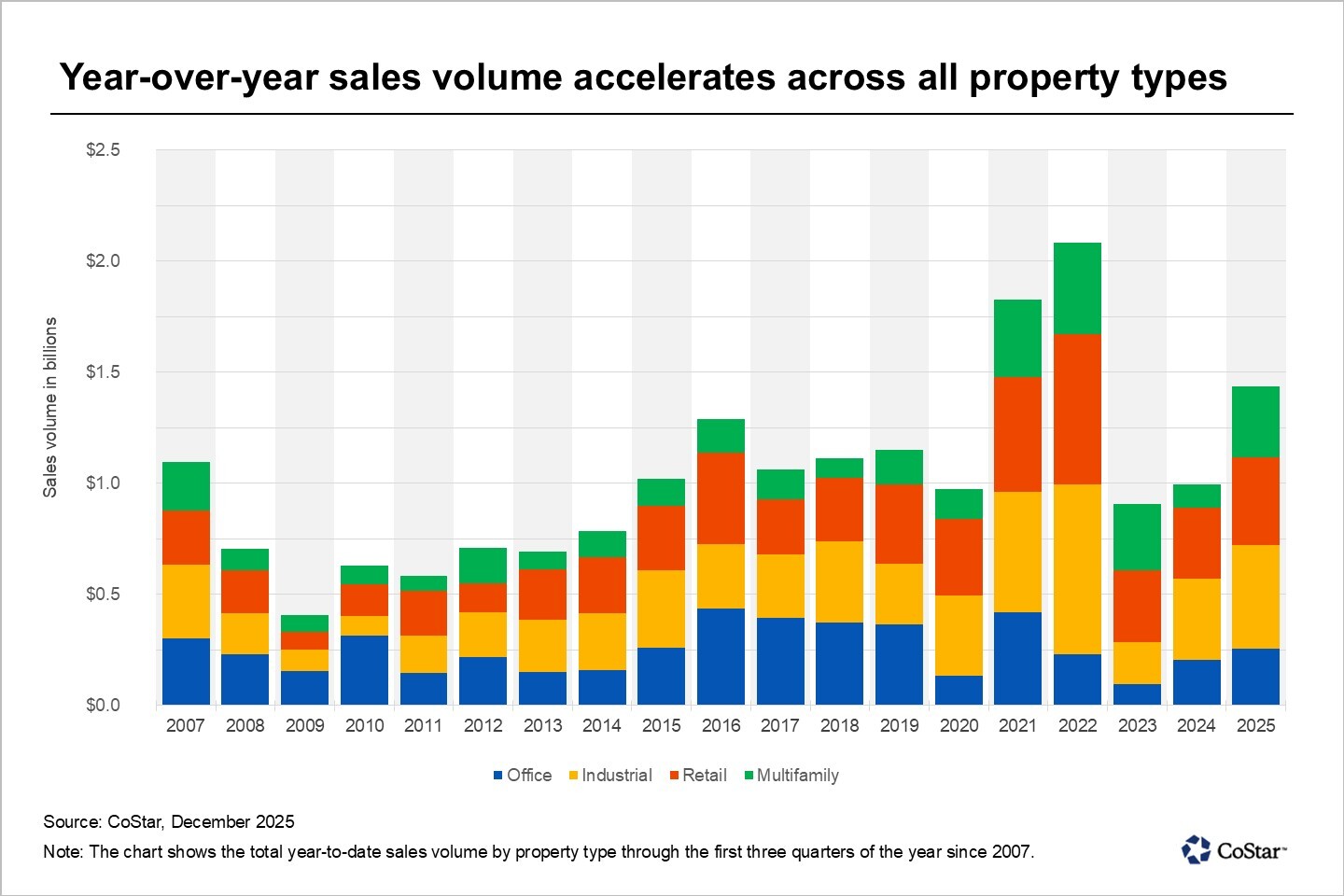

Milwaukee entered 2025 with renewed momentum, posting its strongest commercial real estate sales volume in three years. After a period of uncertainty and high capital costs, investors are returning with a sharper focus on quality assets, realistic pricing, and reliable cash flow. Activity is increasing across industrial, office, multifamily, and retail sectors, signaling a broad-based recovery fueled by stabilizing interest rates and improved market confidence.

As 2026 approaches, the title insurance industry is navigating a complex mix of market recovery, rising fraud threats, and sweeping regulatory changes. Industry leaders say the path forward centers on smarter technology, leaner operations, and stronger support for title agents. With AI-driven workflows, enhanced fraud prevention, and new compliance demands—including FinCEN’s expanded Geographic Targeting Orders—companies like Stewart and First American are reshaping how title work gets done. For real estate and mortgage professionals, the year ahead promises more automation, heightened standards, and major opportunities for those who stay ahead of the curve.

The real estate industry is undergoing a major transformation in 2025 as advancements in AI, proptech, blockchain, and data intelligence redefine how properties are marketed, valued, financed, and experienced. From instant digital valuations and immersive virtual tours to tokenized investments and predictive analytics, technology is reshaping every stage of the real estate lifecycle. Professionals who embrace these innovations—while maintaining the human expertise clients still rely on—will lead the next era of the industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}