Florida’s Insurance Showdown: The Political Storm Driving 2026 — And Why It Matters for Every Property Professional

Florida’s insurance market is reshaping itself in real time — and the rest of the country is watching. With 2026 on the horizon, Florida’s leaders have launched a fierce debate over whether the state’s sweeping insurance reforms are a breakthrough or a breakdown, leaving homeowners, condo owners, and real estate professionals caught in the middle.

This political tug‑of‑war was spotlighted in a recent

WPTV investigation, which examined how Florida’s affordability crisis — driven by soaring property and auto insurance — is becoming the defining issue of the next election cycle.

Republicans Say Reforms Are Working: “Things Are Looking Up”

Florida CFO Blaise Ingoglia insists that the state’s multi-year insurance overhaul is finally delivering results. In an interview with Scripps Capitol reporter Forrest Saunders, Ingoglia pointed to what he calls “drastic movement” in Florida’s auto insurance market.

He referenced recent developments in which major insurers have been forced to return excess profits to policyholders — including a

$1 billion refund by Progressive — as well as a 10% rate reduction from State Farm.

“When you look at the reforms we did three years ago, clearly the reforms are working. We’re just asking for people to continue to be patient on the homeowner’s insurance market.”

Republican leaders say reinsurance prices are easing and new carriers are coming back into Florida’s marketplace. They argue that the worst is behind the state — as long as Florida does not reverse course.

Democrats: “Families Can’t Wait”

Democratic lawmakers reject the optimism, arguing that the relief is not reaching real Floridians — especially homeowners and condo owners squeezed by skyrocketing premiums.

Senate Minority Leader Lori Berman said Florida remains one of the most expensive states in the nation for insurance, calling the situation “unacceptable” during an October

press conference.

Supporting their position, new data from

Realtor.com

shows condo prices dropping more than 8% year‑over‑year due to massive post‑Surfside insurance spikes and rising HOA fees. Five Florida cities remain among the nation’s highest insurance-burdened markets.

On top of that,

Bankrate

ranks Florida as the most expensive state in the nation for auto insurance — averaging over $4,100 per year.

“We want to make sure we are approaching the affordability crisis in a way that actually helps families,” said House Minority Leader Fentrice Driskell. She argues for stronger regulation, rate‑hike caps, and more transparency.

Democrats also warn that Republican-backed property tax amendments could threaten public services while distracting from the real cost driver: insurance.

A Defining Battle Ahead of 2026

From homeowners locked into rising premiums to condo associations hitting breaking points, Florida is bracing for a pivotal year. Insurance, not taxes, is increasingly becoming the issue voters are talking about — and candidates cannot ignore it.

Lawmakers return to Tallahassee on January 13, where the debate will almost certainly intensify.

Want to understand Florida’s real estate and insurance landscape from a professional perspective?

Whether you’re expanding your career in real estate, insurance, mortgage, or other professional fields,

Cameron Academy helps you stay licensed, informed, and ahead of industry changes.

Visit CameronAcademy.com to explore courses built for working professionals.

To explore the original investigation and follow ongoing coverage of Florida’s insurance challenges, visit

WPTV’s full report here.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

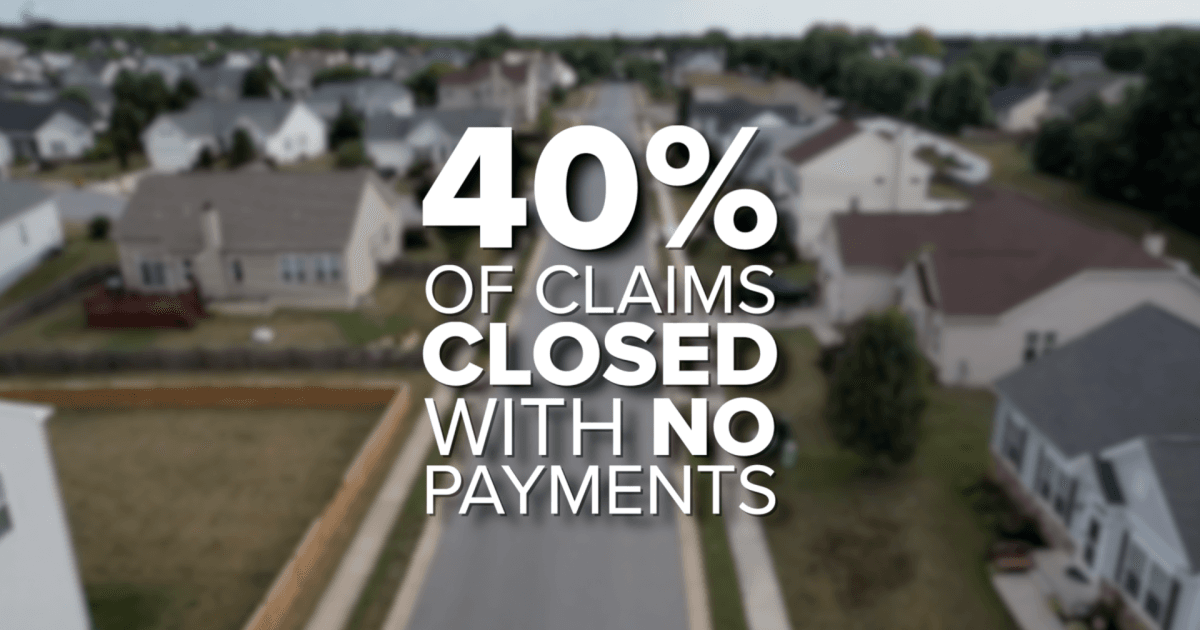

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}