Florida’s Push for Insurance Transparency: What HB 767 Could Mean for Homeowners and Professionals

As insurance premiums climb statewide, a new bill gaining momentum in Tallahassee is aiming to give Floridians something they’ve been demanding for years: transparency.

The Florida House has unanimously passed HB 767 by a vote of 114–0 — a rare display of unity in a time when homeowners are searching for answers. Rather than capping premiums, the bill focuses on something more foundational: forcing insurers to publicly disclose rates, premiums, and related information not protected as trade secrets.

If it becomes law, this information would be posted directly on the state’s insurance website, giving policyholders a clearer look at why rates are rising and how insurers determine what they charge.

Why Transparency Matters Right Now

State Rep. Yvette Benarroch of Naples, who filed the bill, captured the urgency behind HB 767:

“Right now, affordability is an issue for the whole state and insurance is part of the problem, so we want to make sure that little by little we can get to where they trust us again, because right now I can tell you constituents do not trust insurance companies, and they do not trust government.”

Her comments echo the frustration felt by homeowners, real estate agents, mortgage professionals, and insurance licensees across Florida. With premiums deeply influencing home affordability and market activity, clarity is becoming a must-have tool rather than a luxury.

Why This Matters for Florida Professionals

Whether you’re navigating the real estate market, advising mortgage clients, or working within the insurance sector, understanding bills like HB 767 is essential. These legislative shifts influence consumer confidence, market behavior, and the conversations professionals have every day.

That’s why organizations such as Cameron Academy emphasize staying informed. For those pursuing or renewing licenses in real estate, insurance, mortgage, or other regulated fields, keeping up with evolving laws ensures your credibility — and your effectiveness — remain strong.

What Happens Next?

The bill now moves to the Florida Senate. If approved and signed by the governor, insurers may soon be required to provide a level of transparency many Floridians have been waiting for.

To follow the original reporting and ongoing updates, visit WPTV News, where journalist Matt Sczesny continues digging into Florida’s insurance landscape.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

The title insurance industry is entering 2026 with a renewed focus on technology, operational efficiency, and stronger agent support after years of volatility. Leaders from major underwriters report rising transaction activity, improved affordability, and a surge in automation and fraud‑prevention tools—signs that smarter systems and better training will define the next wave of growth.

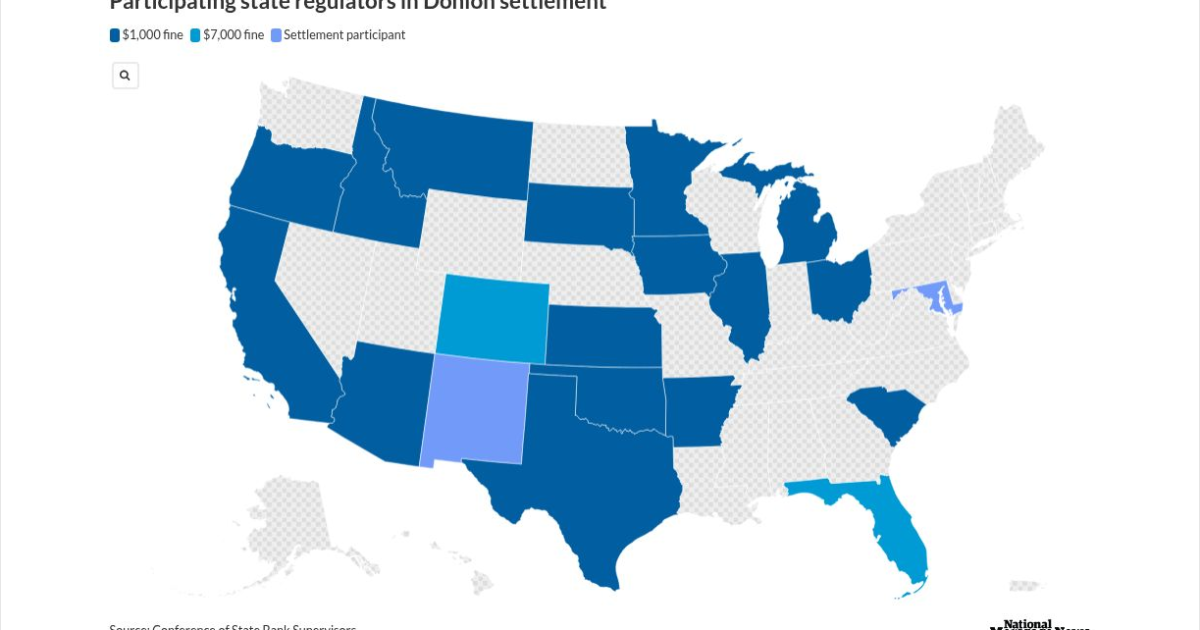

A multistate crackdown has sent shockwaves through the mortgage industry as Patrick Terrance Donlon, CEO of Trusted American Mortgage, accepted a sweeping settlement that bans him from working as a mortgage loan originator in 21 states—19 of them permanently. Regulators say Donlon had another individual complete his mandatory licensing and continuing‑education courses, a violation that triggered a coordinated investigation and a $31,000 penalty. The case underscores regulators’ growing intolerance for education fraud and serves as a sharp reminder to industry professionals: cutting corners on licensing can end careers.

Florida’s once‑booming housing market is cooling fast as rising insurance premiums, increasing foreclosures, and expanding flood zones push buyers to back out of deals and force sellers to cut prices. With insurance now adding thousands to annual housing costs, professionals across real estate, mortgage, and insurance are navigating a dramatically shifting landscape that’s redefining affordability in the Sunshine State.

Florida begins 2026 with a wave of more than 250 new laws now in effect, impacting healthcare, insurance, real estate, and consumer protections statewide. From free breast cancer screenings for state employees to tighter pet insurance regulations, mandatory healthcare refund rules, enhanced animal‑cruelty penalties, and new condo‑management requirements, these updates carry major implications for professionals navigating Florida’s evolving regulatory landscape.

Florida’s barrier islands may offer postcard-perfect beaches and soaring real estate demand, but they’re also some of the most fragile and costly places to build in the United States. With 765,000 residents living on land that shifts, sinks, and takes the brunt of every major hurricane, the financial and insurance risks are accelerating fast. From billion‑dollar beach rebuilds to towers settling into the sand, today’s coastal development challenges are reshaping conversations around property values, disclosure, and long‑term resilience. For real estate professionals, understanding these risks isn’t just smart — it’s becoming essential.

A Cedar City development is turning heads with its fresh approach to affordability. The team behind Temple View Commons is delivering luxury‑inspired twin homes at prices below the local median by using a small, hands‑on staff and cutting traditional costs like realtor commissions. In a tight Utah housing market where inventory is scarce and prices remain high, their strategy offers a realistic path to homeownership without sacrificing high‑end finishes.

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

Title Insurance Leaders Double Down on Tech and Efficiency to Drive 2026 Market Momentum Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}