Housing Market Predictions for 2026: Will Home Prices Finally Drop?

The U.S. housing market continues its slow march toward balance as 2025 winds down. Buyers are gaining a little more breathing room thanks to moderating home prices, rising inventory, and slightly friendlier mortgage rates. Still, many remain cautious—waiting to see what 2026 will bring.

According to experts featured in the full report from Forbes Advisor, the big picture is clear: expect gradual price growth, relatively stable rates, and the most buyer-friendly conditions in markets with rising supply and strong local economies.

Fed Cuts Rates Again: Will Mortgage Rates Ease?

The Federal Reserve delivered its third rate cut of the year, dropping the benchmark rate to its lowest point since 2022. Mortgage rates, while not directly tied to the federal funds rate, tend to follow its overall trend.

Fed Chair Jerome Powell noted that inflation data remains limited but steady, keeping expectations for stable economic conditions heading into 2026.

The 2026 Housing Market Forecast

National home price growth slowed to just 1.3% annually in October 2025—one of the softest readings in years.

Regional highlights:

Miami, Tampa, and Phoenix: experiencing price declines

Chicago, Cleveland, NYC: showing modest gains

Most analysts expect 1% to 2% national growth in 2026—not a crash, but not a return to pandemic-era surges either.

Will the Housing Market Crash?

Short answer: Highly unlikely.

Inventory is still below pre-pandemic levels, and homeowners continue to hold strong equity positions. Even with cooling prices in some markets, there is no clear trigger for a widespread collapse.

“The record low supply of houses on the market protects against a market crash.” — Tom Hutchens, Angel Oak Mortgage Solutions

When Will the Market Fully Recover?

A meaningful recovery depends on two major shifts:

More homes hitting the market

Mortgage rates falling into the upper‑5% range

Both could happen in 2026—but the pace will vary regionally.

How Today’s Payments Compare to Last Year

The Forbes Advisor mortgage calculator shows a clear benefit to 2025 buyers. With rates lower than in 2024, a typical buyer saves $106 per month and over $38,000 in lifetime interest.

Existing & Pending Home Sales: What the Numbers Show

Existing-home sales ticked up 1.2% in October 2025, reaching 4.1 million transactions. Pending sales also climbed 1.9%, particularly in the Midwest and South where affordability remains stronger.

NAR’s Lawrence Yun notes that seasonal slowdowns may offer buyers more negotiating power during winter months.

Housing Inventory Outlook

Inventory is rising in several key markets, including Austin, San Antonio, and Tampa—areas that overheated during the pandemic. Meanwhile, markets like Buffalo, Cleveland, and Pittsburgh continue facing tight supply.

If mortgage rates drop significantly, expect inventory to tighten again as demand surges.

Should You Wait to Buy?

“The best time for buyers is when they find a home they like, can afford, and fits their family’s needs.” — Orphe Divounguy, Zillow Home Loans

Trying to perfectly time the market rarely works. Rising prices, shifting inventory, and uncertain rates make preparation more important than prediction.

Pro Tip: If you’re building a long‑term real estate career, staying informed is just as important as staying licensed.

Real estate professionals in Florida and beyond trust Cameron Academy for licensing, continuing education, and professional development.

Pro Tips for Buyers

Know your true budget—monthly payments matter more than listing prices.

Be flexible with size, features, and location.

Study local inventory trends and days on market.

Stay patient and avoid stretching beyond your means.

Pro Tips for Sellers

Research comparable properties and price competitively.

Ensure the home looks its best—online curb appeal matters.

Work with a knowledgeable local agent.

Fix known issues before listing to avoid buyer objections.

FAQs

Will lower mortgage rates push prices up?

Yes. Lower rates increase demand, which pressures prices upward—especially in tight markets.

What happens if the market crashes?

Home values fall, foreclosures rise, and inventory balloons. However, experts agree a 2026 crash is highly unlikely.

Is it smart to buy real estate before a recession?

For long-term homeowners: usually yes. For short-term investors: more risky.

Final Thoughts

The 2026 housing market won’t look like the frenzy of 2021 nor the tight freeze of 2023–2024. Instead, buyers and sellers should expect a slow return toward balance—with opportunities strongest in markets gaining inventory.

And if you’re working toward becoming a real estate professional—or expanding your credentials—now is an excellent time to strengthen your expertise. Visit Cameron Academy for real estate, mortgage, insurance, and professional licensing across the nation.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

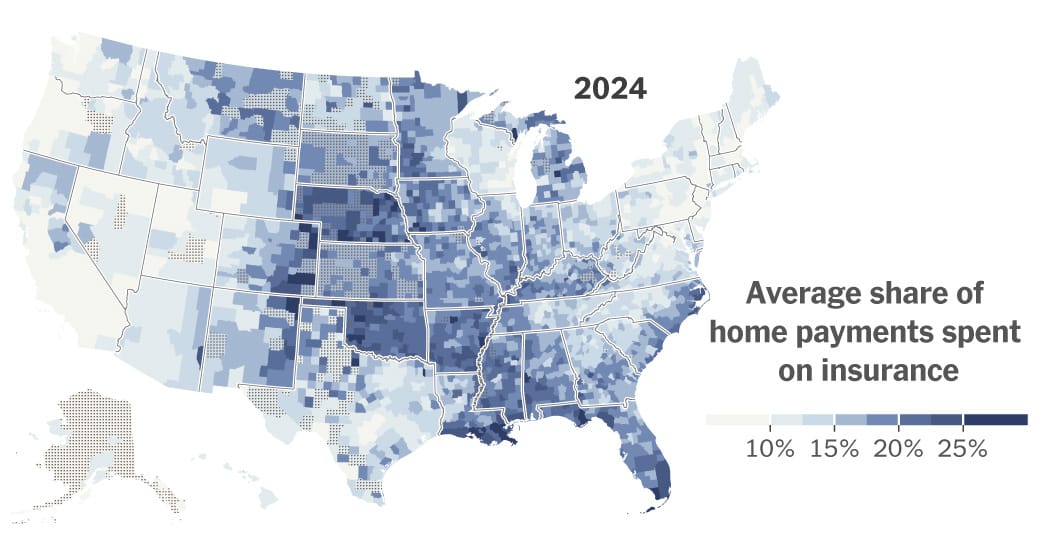

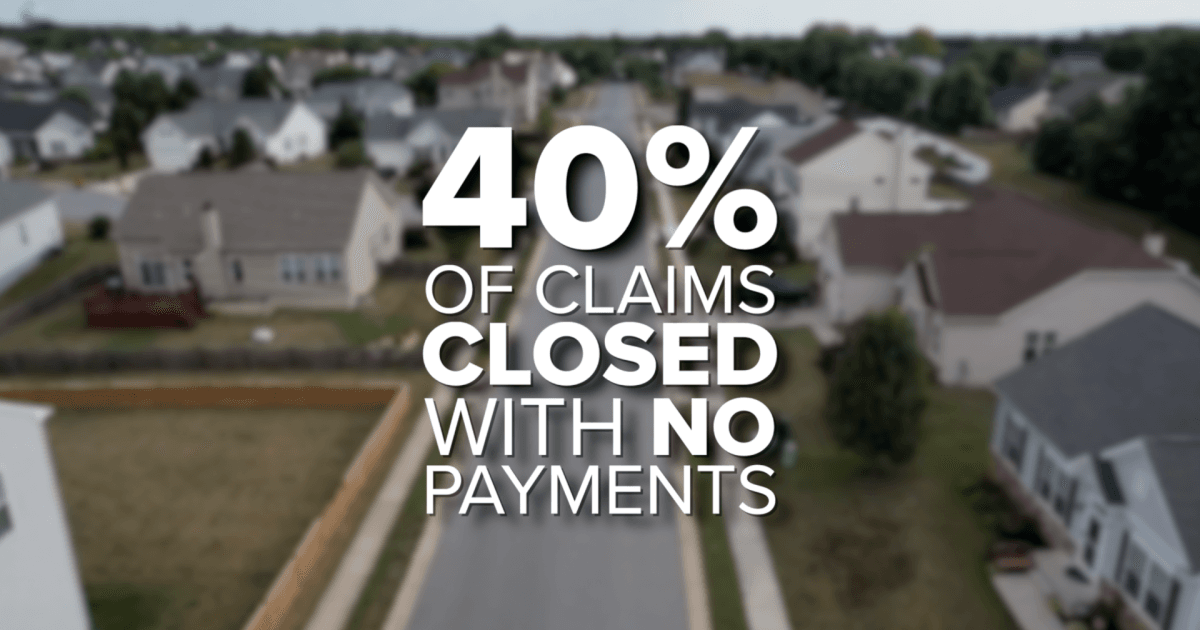

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}